TDS on Rent to be Deducted If Monthly Rent Payment Exceeds Rs. 50,000 (From FY 25-26 Onwards):

Any individual or HUF or others (company/partnership firm) paying a monthly rent above Rs. 50,000 is required to deduct TDS on the rent paid.

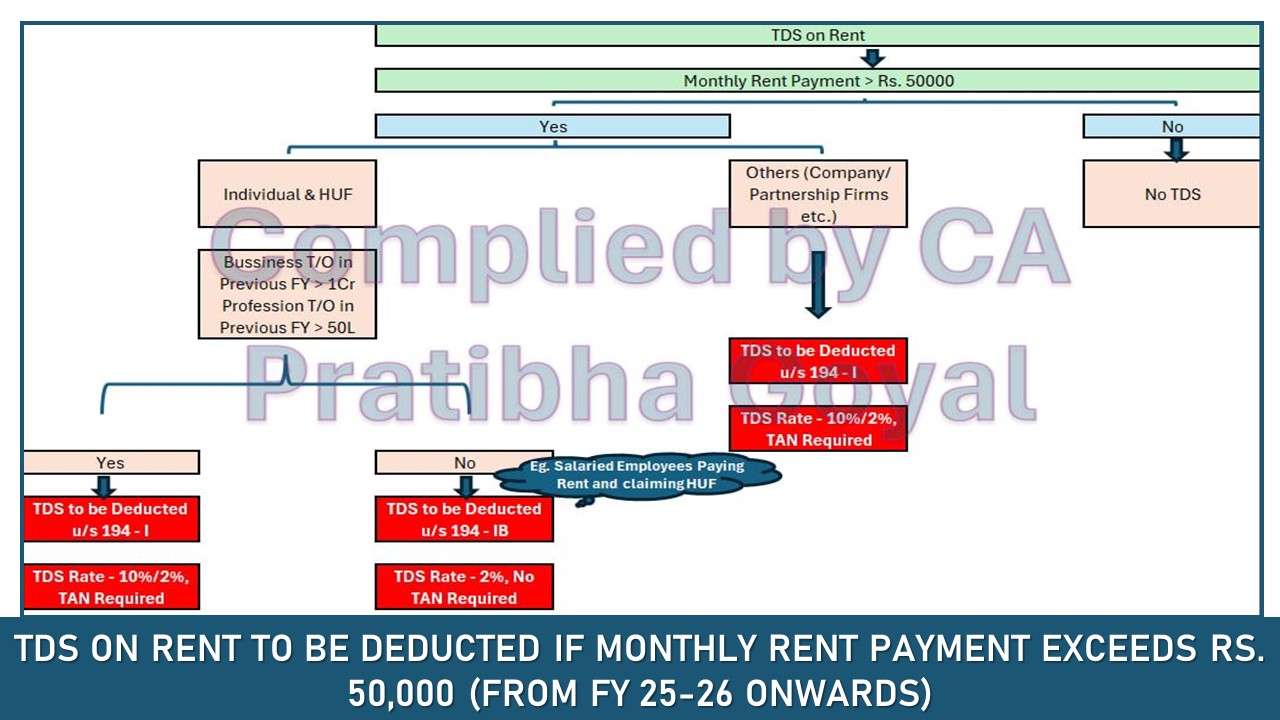

TDS on Rent

Table of Contents

TDS on Rent to be Deducted If Monthly Rent Payment Exceeds Rs. 50,000 (From FY 25-26 Onwards)

Any individual or HUF or others (company/partnership firm) paying a monthly rent above Rs. 50,000 is required to deduct TDS on the rent paid to the landlord. The deducted TDS must be remitted to the Income Tax Department.

If the monthly rent paid is less than Rs. 50,000, then no TDS is required, regardless of who the tenant is. However, if the rent exceeds Rs. 50,000 per month, then TDS is applicable.

TDS on rent for individual or HUF

In case the rent is paid by an individual or HUF whose turnover/gross receipts exceed 1 crore or 50 lakhs, respectively, in the last financial year have to deduct TDS on rent in the current year. The TDS is deducted as follows:- 2% of rent on plant and machinery

- 10% of rent on land, building or furniture

TDS on rent for Others

On the other hand, if the rent is paid by a company, partnership firm, or any entity apart from individuals and HUFs, then TDS must be deducted under Section 194-I as follows:- The TDS rate will be 10% for land or buildings.

- 2% for plant or machinery, and the payer is required to have a TAN.

About Author

Nidhi

Content Writer

Nidhi is a skilled content writer specializing in personal finance. She creates clear, engaging articles on mutual funds, investments, insurance, and wealth-building strategies. With a passion for simplifying complex financial topics, Nidhi helps readers make informed money decisions with confidence. She can be reached at [email protected]

Nidhi is a skilled content writer specializing in personal finance. She creates clear, engaging articles on mutual funds, investments, insurance, and wealth-building strategies. With a passion for simplifying complex financial topics, Nidhi helps readers make informed money decisions with confidence. She can be reached at [email protected]

Studycafe

Studycafe New Delhi, Delhi, India

New Delhi, Delhi, India 1832

1832My Recent Articles

- Karnataka High Court Gives Another Chance in GST Matter Due to Lack of Hearing

- Delay Should Be Condoned if Explanation is Unrefuted: ITAT

- Non-Service of Income Tax Notice, Ill health of taxpayer, ITAT condones Appeal filing delay

- Books of Accounts Cannot be Rejected Without Any Specific Defect: ITAT Kolkata

- Karnataka High Court Sends ITC Matter Back to GST Authorities for Reconsideration

Up Next

Loading suggestions…

Recent Posts

All Posts

Tags

No tags yet.

Recent Posts

All Posts

Tags

No tags yet.