Analysis of Recent orders passed by NAA (National Anti-Profiteering Authority)

Section 171(1) of the CGST Act, 2017 stipulates that any reduction in the rate of tax on any supply of goods or services or the benefit of input tax credit shall be passed on to the recipient by way of commensurate reduction in prices.

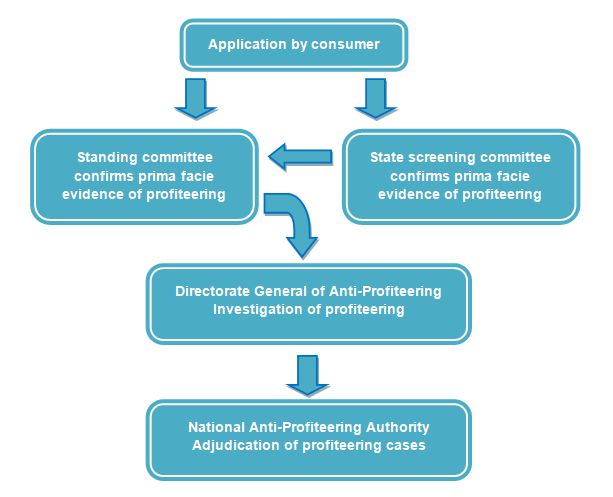

Section 171(2) of the CGST Act, 2017 stipulates that the Central Government may, on recommendations of the Council, by notification, constitute an Authority, or empower an existing Authority constituted under any law for the time being in force, to examine whether input tax credits availed by any registered person or the reduction in the tax rate have actually resulted in a commensurate reduction in the price of the goods or services or both supplied by him.

Section 171(3) of the CGST Act, 2017 stipulates that the

Authority referred to in sub-section (2) shall

exercise such

powers and

discharge such

functions as may be

prescribed.

Important procedural details have been specified vide

rule 122 to

rule 137 of the CGST Rules, 2017, inter alia includes, constitution of the Authority, constitution of the Standing Committee and Screening Committees, power to determine the methodology and procedure, examination of application by the Standing Committee and the Screening Committee, initiation and conduct of proceedings, confidentiality of information, cooperation with other agencies or statutory authorities, power to summon persons to give evidence and procedure documents, order of the Authority, compliance by the registered person, monitoring of the order etc.

The following flow chart will help us to understand the organisational structure:

At the time of penning down this article, so far nine orders have been published as passed by the Authority in their website (www.naa.gov.in). All the orders have been reviewed and are summarised below with key take away points from each order:

Analysis of Recent orders passed by NAA

| Sl. No |

Name of the parties |

Citation |

Date of the Judgement |

| 1 |

Sh. Dinesh Mohan Bhardwaj Proprietor, M/S U.P. Sales (Applicant) Vs Services Versus M/S Vrandavaneshwree (Respondent) |

2018 (4) Tmi 1377 - The National Anti-Profiteering Authority |

27-03-2018 |

| Sl. No |

Name of the parties |

Citation |

Date of the Judgement |

| 2 |

Kumar Gandharv (Applicant) Vs KRBL Ltd (Respondent). |

2018 (5) Tmi 760 - National Anti-Profiteering Authority |

04.05.2018 |

Summary of Case No. 3/2018:

a. Facts

i. KRBL Ltd., being the manufacturer of India Gate Basmati Rice, sold 10 kg packet of India Gate Basmati Rice (Mini Mogra), herein after stated as product, at a MRP of Rs. 540/- and Rs. 585/- in the month of August, 2017 and October, 2017, respectively.

ii. The product wasnt subjected to tax in pre-GST regime, was brought under the net of tax in GST regime w.e.f 22.09.2017 when tax (GST) @5% was levied.

iii. Respondent was thus became eligible to avail of input tax credit (ITC) w.e.f the same date.

iv. Applicant vide his application dated 27.11.2017, sent through e-mail to the Standing Committee alleged that the benefit of reduction in the rate of tax on the product has not been passed on to the consumers as its Maximum Retail Price (MRP) had been increased.

v. Standing Committee examined the application and forwarded to the Director General Safeguards (DGSG) for detailed investigation on 18.12.2017.

b. Issue

i. Whether on becoming eligible to avail of the benefit of input tax credit (ITC) on India Gate Basmati Rice, benefit of input tax credit (ITC) has been passed on to the customers in view of increase in MRP of 10 kg packet of India Gate Basmati Rice

c. Decision

i. No net benefit of ITC is available to the respondent which could be passed on to the customers. Accordingly the Authority didnt find any substance in the application filed by the Applicant as there is no violation of the provisions of section 171 of the CGST Act, 2017 and hence the same is dismissed.

d. Ratio

i. India Gate Basmati Rice, on becoming taxable product, benefit of input tax credit was made available to the Respondent w.e.f 22.09.2017.

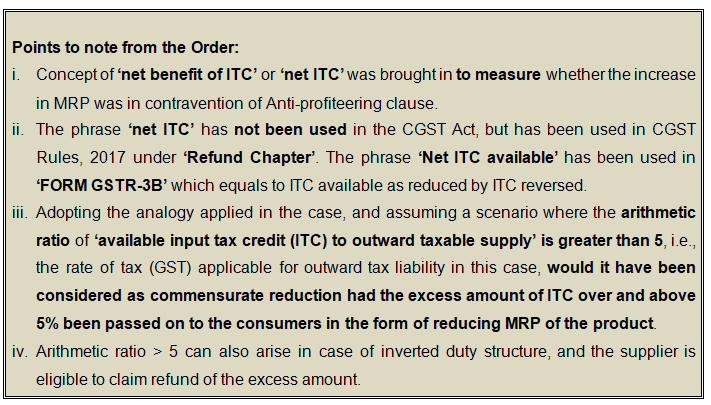

ii. It was further revealed from the data submitted for three months, i.e, September, October and November, 2017 that input tax credit (ITC) available as a percentage of total value of taxable supplies during these three months varied between 2.69% to 3%, whereas the GST rate on outward taxable supply was 5%.

iii. Thus ITC available was insufficient to discharge GST liability, and the balance amount had been paid in cash.

iv. Cost of price of paddy, which amounts to 75% cost of production, has increased by more than 30% in the FY 2017 as compared to the FY 2016.

v. The Respondent submitted that because of the stiff competition in the market, they couldnt pass on the increased cost entirely to the consumer, instead increased Maximum Retail Price MRP by 8% only from Rs. 540/- to Rs. 585/-.

vi. Therefore, the Authority didnt find any reason to treat the price fixed by the respondent as a violation of section 171 of the CGST Act 2017, i.e, Anti-profiteering clause.

| Sl. No |

Name of the parties |

Citation |

Date of the Judgement |

| 3 |

M/S Abel Space Solutions LLP (Applicant) Vs M/s Schindler India Private Limited (Respondent) |

2018 (6) Tmi 687 - The National Anti Profiteering Authority |

31.05.2018 |

Summary of Case No. 4/2018:

a. Facts

i. An application, dated 20.09.2017, was filed before the Standing Committee on 20.09.2017.

ii. Applicant had placed orders for supply of two lifts in December, 2016. First lift was delivered, against which full payment was also made during pre-GST regime.

iii. The issue is related to the second lift. The material was despatched to the Applicant on 29.03.2017. An advance was paid to the Respondent against invoice dated 28.06.2017, on which Service Tax was charged. Installation was done on 27.07.2017, i.e, in GST regime, when two more invoices were raised by the Respondent with tax (GST).

b. Issue

i. It has been alleged by the Applicant that the tax (GST) has been charged without excluding the pre-GST regime Excise Duty amount on the material and hence the Respondent had charged tax twice.

c. Decision

i. Based on the given facts, no substance was found in the claim filed by the Applicant and thus hereby orders dropping of the present proceedings as no violation of the provisions of section 171 of the CGST Act, 2017 has been established.

d. Ratio

i. The Applicant had paid advance for purchase of the second lift and the Respondent had charged Service Tax which was leviable in pre-GST regime.

ii. Supply and installation of lift amounted to Works Contract and as per Rule 2A of the Service Tax (Determination of Value) Rules, 2006, value of the service portion of the works contract was to be taken as equivalent to the gross amount charged for the works contract minus the value of property in goods transferred in the execution of the said contract and on the goods transferred Value Added Tax (VAT) was to be charged and on the service portion, Service Tax was leviable.

iii. Explanation to Rule 3 of Point of Taxation Rules, 201, wherever any advance was received by the service provider against the taxable service, the point of taxation was to be construed as the date of receipt of such advance.

iv. Installation of elevator was completed in the GST regime, and hence the point for levy of tax for supply of material fell under the GST regime and accordingly, two more invoices were issued on 27.07.2017 wherein the applicable GST was correctly charged.

v. Respondent could have passed on the benefit of Excise Duty if the material was despatched on or after 01.07.2017 and since all the materials were delivered before 30.06.2017 and hence, he was not in a position to pass such benefit to the Applicant.

| Sl. No |

Name of the parties |

Citation |

Date of the Judgement |

| 4 |

Sh. Rishi Gupta (Applicant) Vs M/s. Flipkart Internet Pvt. Ltd (Respondent) |

2018 (7) Tmi 1490 - National Anti-Profiteering Authority |

18.07.2018 |

Summary of Case No. 5/2018:

a. Facts

i. An application dated 11.01.2018 was filed by the Applicant before the Standing Committee.

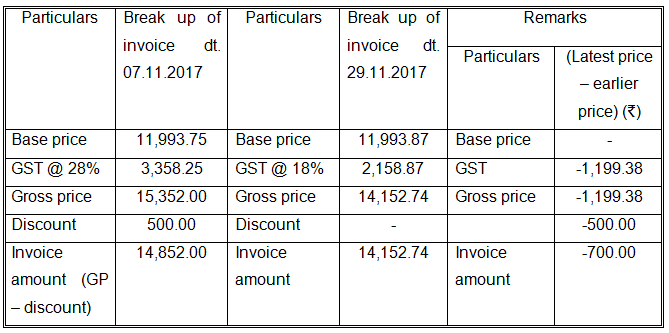

ii. Applicant ordered a Godrej Interio Slimline Metal Almirah through the Respondent vide his order no. 110666745976477000 on 04.11.2017 and a tax invoice dated 07.11.2017 was issued to him for an amount of Rs. 14,852/- by M/s. Godrej & Boyce Mfg. Co. Ltd., Mumbai (herein after referred as Supplier).

iii. Rate of tax (GST) has been reduced by the Government of India on 14.11.2017 from 28% to 18%.

iv. Another invoice dated 29.11.2017, at the time of delivery, was issued by the Supplier for an amount of Rs. 14,152/-.

v. Respondent vide his letter dated 27.04.2018, intimated that excess amount of Rs. 700/- was refunded to the Applicant on 18.01.2018.

b. Issues

i. Excess amount charged earlier should have been refunded to the Applicant, and

ii. Respondent by not refunding the excess amount collected, has resorted to profiteering.

c. Decision

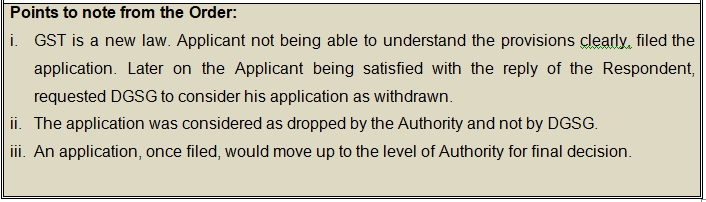

i. Respondent was not the Supplier / Manufacturer of the Almirah, was only an agent who had offered his platform, i.e, a market place to the Supplier to sell the Almirah by charging commission, and was also not responsible for collection or refund of tax (GST). Hence, he cannot be held accountable for contravention of section 171 of the CGST Act, 2017.

ii. Allegation of profiteering made by the Applicant against the Respondent as well as Supplier is not established and hence the present application is not maintainable and the same is dismissed.

iii. As there may be several cases, where e-platforms have collected excess tax (GST) at the time of booking which are required to be refunded. Therefore, the Authority has already directed the Director General of Audit, Central Board of Indirect Taxes and Customs vide letter No. NAA/2018/DO/08/2011 dated 24.05.2018 to audit the major e-platforms and submit its findings to the Authority.

d. Ratio

i. The Respondent, being an agent, offered a market place which enabled the sellers to offer their products for direct sale to the customers for which it was charging commission.

ii. Sellers were entirely responsible

iii. Base price i.e, Rs. 11,993.75/-, was not changed by the Supplier either before or after the rate of change of tax.

iv. Rs. 700/- was refunded to the Applicant by the Supplier on 18.01.2018.

v. Withdrawal of discount of Rs. 500/- by the Supplier vide his invoice dated 29.11.2017 did not amount to profiteering as discount was given by the Manufacturer supplier out of profit margin.

| Sl. No |

Name of the parties |

Citation |

Date of the Judgement |

| 5 |

Shri Pawan Sharma C/O Kalptaru Departmental & General Stores (Applicant no 1), Director General Anti-Profiteering, Indirect Taxes & Customs (Applicant no 2) Vs M/S Sharma Trading Company (Respondent) |

2018 (9) Tmi 625 - The National Anti-Profiteering Authority |

07.09.2018 |

Summary of Case No. 6/2018:

a. Facts

i. Applicant No. 1 was a distributor and stockist of M/s. Hindustan Unilever Limited (Manufacturer supplier).

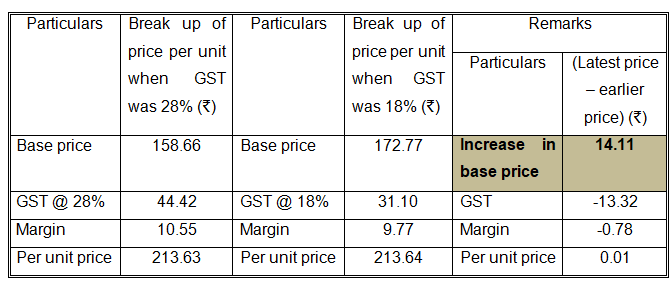

ii. Applicant No. 1 had bought Vaseline VTM 400ml on 26.09.2017 at Rs. 213.63/- per unit vide tax invoice No. GSA25066 when tax (GST) rate was 28%, and 20 units of Vaseline VTM 400ml on 15.11.2017 at Rs. 213.63/- per unit vide tax invoice No. GSA37782 when the tax (GST) rate was reduced to 18% on this product vide Notification No. 41/2017 Central Tax (Rate) dated 14.11.2017.

iii. An application dated 22.11.2017 was filed by the Applicant No. 1 before the Standing Committee of Anti-Profiteering that the Respondent had indulged in profiteering in contravention of section 171 of the CGST Act, 2017 as the price of Vaseline VTM 400 ml was not reduced.

iv. The application was referred by the Standing Committee of Anti-Profiteering to Director General of Anti-Profiteering (DGAP) for detailed investigation.

v. DGAP asked the Respondent to suo moto determine the quantum of benefit which he had not passed on after the reduction in the rate of tax.

vi. 20 units of Vaseline VTM 400ml were returned by the Applicant No. 1 to the Supplier vide Goods Return invoice No. 534 dated 15.12.2017 against which CN No. AA021330 was issued by the Supplier on 23.12.2017.

vii. Manufacturer supplier runs various Consumer Promotion Schemes (CPS) during the lean period by offering additional quantity or along with some additional products.

viii. Additional quantity was offered in September, 2017 which was also in offering in November, 2017, when MRP was retained at Rs. 235/- for 400 ml i.e, additional 100 ml was offered along with 300 ml of Vaseline VTM.

ix. MRP was reduced from Rs. 235/- to Rs. 233/- w.e.f 13.12.2017.

x. Respondent claims to be an intermediary in the supply chain.

b. Issues

i. Section 171 of the CGST Act, 2017 did not provide for any methodology for determining the commensurate reduction in the prices.

ii. It was alleged that the Respondent had not passed on the benefit of reduction in the rate of tax by lowering the price of Vaseline VTM 400 ml, and indulged in profiteering in contravention of the provisions of Section 171 of the CGST Act, 2017.

c. Decision

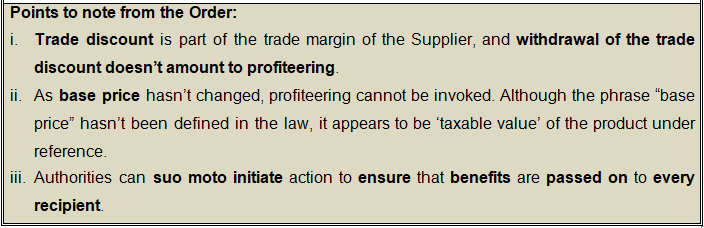

i. The argument advanced by the Respondent appears to be frivolous as it involves only mathematical calculation of the amount by which the tax had been reduced i.e by 10% and after subtracting the same from the existing Maximum Retail Price (MRP), the MRP was to be re-fixed as per the provisions of the Legal Metrology (Packaged Commodities) Rules, 2011. It was also mandatory for the Respondent to declare the reduced MRP by affixing additional sticker or stamping or online printing as per letter No. WM-10(31)/2017 dated 16.11.2017 issued by the Ministry of Consumer Affairs, Food and Public Distribution.

ii. Base price of Vaseline VTM 400 ml was increased by the Respondent exactly by the same amount by which the tax had been reduced. He was legally bound not to charge the enhanced base price and cannot escape his accountability of passing on the benefit of the reduction in the rate of tax to his customers. Allegation of profiteering has been duly established against him. Accordingly, the Respondent was directed to reduce the sale price of the product immediately commensurate to the reduction in the rate of tax as was notified on 14.11.2017 and pass on the benefit of reduction in the rate of the tax to his customers. Penalty is imposable.

d. Ratio

i. Increase in base price of the product is as follows:

| Sl. No |

Name of the parties |

Citation |

Date of the Judgement |

| 6 |

Shri Sukhbir Rohilla along with 108 other Applicants (collectively as 1st Applicants). & Director General Anti-Profiteering, Indirect Taxes & Customs (2nd Applicant) Vs M/s Pyramid Infratech Pvt. Ltd (Respondent)., |

|

18.09.2018 |

Summary of Case No. 7/2018:

a. Facts

i. Two projects viz. (1) Urban Homes, Sector 70A, Gurugram, and Urban Homes, Sector-86, Gurugram are being executed by the Respondent.

ii. Several applications were filed with the Haryana Screening Committee for appropriate redressal of their grievance. Applications were examined by the Screening Committee who decided to forward these applications to Standing Committee of Anti-Profiteering for further necessary action.

iii. Standing Committee confirmed that there was prima facie evidence of non compliance and forwarded these applications to now redesignated as Director General of Anti-Profiteering (DGAP) for detailed investigation.

iv. DGAP issued a notice to the Respondent to submit his reply in response to the allegations and to suo moto declare the amount of profiteering.

v. Applicants booked flats under the Haryana Affordable Housing Policy, 2013.

vi. Payment was not linked to completion of construction mile stone based, instead was time based payment schedule.

vii. In pre-GST regime Service Tax was exempted and only VAT @5.25% was leviable for the project.

viii. In GST regime, rate of tax (GST) was 12% w.e.f 01.07.2017 and was reduced to 8% w.e.f 25.01.2018.

ix. Applicants alleged that benefit of input tax credit (ITC) which was available is much more than the output tax liability of the respondent.

b. Issues

i. Whether there was any violation of the provisions of Section 171 of the CGST Act, 2017 in this case

ii. If yes then what was the quantum of profiteering.

c. Decision

i. Excess ITC was available to the Respondent the benefit of which he was required to pass on to the Applicants. The Respondent cannot appropriate this benefit as this is a concession given by the Government from its own tax revenue to reduce the prices being charged by the builders from the vulnerable section of society which cannot afford high value apartments. The Respondent is not being asked to extend this benefit out of his own account and he is only liable to pass on the benefit of ITC to which he has become entitled by virtue of the grant of ITC on the Construction Service by the Government.

ii. It is held that the Respondent has profiteered an amount of Rs. 8,22,80,998/-

iii. Profiteered amount is to be refunded to the Applicants along with interest @18% who have applied and also to those Applicants who have not applied as they are identifiable.

d. Ratio

i. ITC ratio to Taxable Value in terms of % during pre-GST regime was 1.1%, whereas the same in GST regime is 7.2%. Thus additional ITC availed in terms of % of taxable supplies was 6.1%.

| Sl. No |

Name of the parties |

Citation |

Date of the Judgement |

| 7 |

Miss Neeru Varshney (Applicant No. 1) and Director General Anti-Profiteering (Applicant No. 2) Vs M/s Lifestyle International Pvt. Ltd. (Respondent) |

2018 (9) Tmi 1640 - National Anti-Profiteering Authority |

25.09.2018 |

Summary of Case No. 8/2018:

a. Facts

i. An application dated 23.11.2017 was filed by the Applicant No. 1 before the Standing Committee.

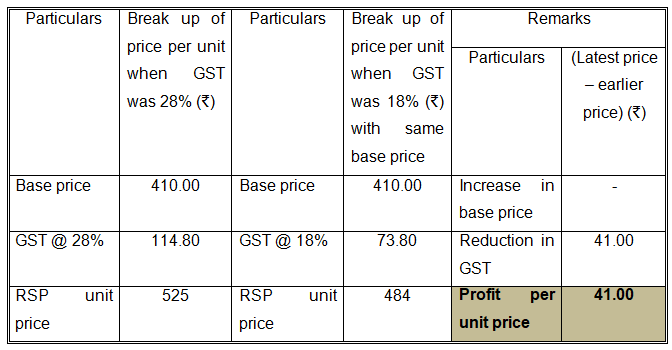

ii. Applicant No. 1 had bought Maybelline FIT Me foundation (here-in-after referred to as the product) from the Respondent @ Rs. 525/- per unit vide tax invoice no. 1230010554 on 22.11.2017 which included GST @ 18%.

iii. Standing Committee examined the above application, and referred to DGAP for detailed investigation.

iv. DGAP had called upon the Respondent to submit his reply on allegation levelled by the Applicant No. 1 and also to suo moto determine the quantum of benefit which had not been passed on to its buyers during the period between 15.11.2017 to 31.01.2018.

v. Respondent was registered in different States and / or UTs, and thus maintained 24 GSTINs. Respondent further claimed that during the period between November, 2017 to January, 2018, he had given discount of 11.66% on the MRP which was more than what he was required to pass on consequent to the reduction in the rate of tax w.e.f 15.11.2017.

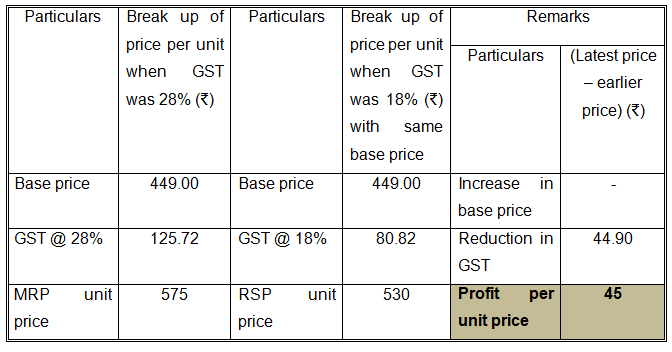

vi. DGAP has further stated that the Respondent had sold 485 units of another shade of the product between 01.11.2017 to 14.11.2017, in which basic price per unit was increased from Rs. 449/- to Rs. 487/- on which GST at a rate of 18% was charged resulting no change in MRP at Rs. 575/- per unit.

b. Issue

i. The Respondent had not passed on the benefit of reduction in the rate of tax by lowering the price of Maybelline FIT Me foundation.

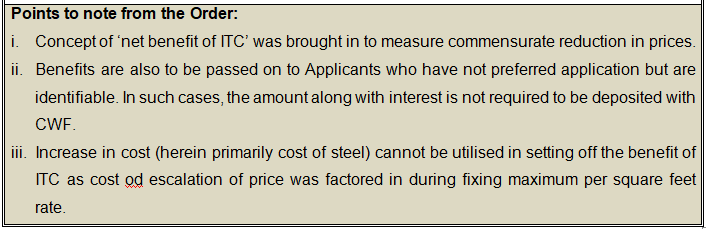

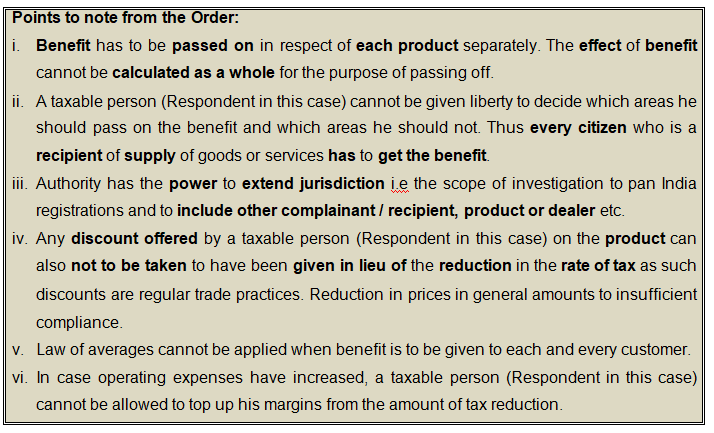

c. Decision

i. Every citizen who is a recipient of supply of goods or services has to get the benefit and hence this benefit has to be calculated on each and every product. The Respondent has no discretion to provide benefit on certain class of products and deny the same in respect of the other products. Denial of the benefit as per the convenience of the Respondent is not permissible as it is hit by the provisions of section 171 of the CGST Act, 2017.

ii. Respondent has failed to reduce base price due to reduction in tax (GST) and had issued incorrect invoices which is established.

iii. Respondent is directed that to reduce the price of both the shades of the product to Rs. 410/- and Rs. 449/- respectively excluding GST. He is directed to refund Rs. 41/- along with interest @ 18% to the Applicant No. 1 from the date when this amount was realised by him from her till the date of refund. Since rest of the recipients are not identifiable the DGAP is directed to get the balance amount of profiteering of Rs. 15,820/- deposited in the Consumer Welfare Fund of the Central and the Concerned State Govt. as per provisions of law along with interest @ 18% till the amount is paid.

iv. To issue notice to the Respondent to show cause as to why penalty as per provisions of Section 122 of the CGST Act, 2017 read with Rule 133 (3) (d) of the CGST Rules, should not be imposed upon him.

v. The DGAP is directed to investigate the claim made by the Respondent in para no 27 that an amount of Rs. 1,98,46,438/- might not have been passed on to the individual buyers by him and submit Report to the Authority under Rule 129(6) of the above Rules..

d. Ratio

i. Increase in per unit base price when MRP was Rs. 550/-:

ii. Increase in per unit base price whose MRP was Rs. 575/-:

Thus it is evident that the per unit profiteering amount is exactly equals to the amount by which tax (GST) has been reduced.

| Sl. No |

Name of the parties |

Citation |

Date of the Judgement |

| 8 |

Sh. Jijrushu N Bhattacharya (Applicant No.1) & Director General Anti-Profiteering (Applicant No. 2) Vs M/s. NP Foods (Franchisee M/s Subway India), (Respondent) |

2018 (9) Tmi 1763 - National Anti-Profiteering Authority |

29.09.2018 |

Summary of Case No.9/2018:

a. Facts

i. Respondent is a franchisee of M/s Subway India, and is free to buy raw material, fix sell price. Franchisor is entitled to royalty on the net turnover.

ii. The Applicant purchased 6 Hara Bhara Kabab Sub on 14.11.2017 from the Respondent.

iii. GST rate in restaurant service was reduced from 18% to 5% without input tax credit (ITC) from 15.11.2017.

iv. Effect of denial of ITC was 11.80%, and Respondent increased base prices ranging from 6% to 17% of the different items, i.e, increase in average base prises by 12.14% to neutralize the effect of denial of ITC.

b. Issues

i. Whether there was reduction in the rate of tax on the restaurant service after 14.11.2017 and whether the benefit as emanating from such reduced tax rate has not been passed to the Applicant No. 1 in terms of the commensurate reduction in the price of the product purchased by him

ii. Whether profiteering of Rs. 452/- was made by the Respondent y selling 32 numbers of items on 14.11.2017 in Karelibaug outlet at increased base price

c. Decision

The allegation of not passing on the benefit on rate reduction is not established against the Respondent. There is no merit in the application filed by the Applicant No. 1 and the same is accordingly dismissed.

d. Ratio

i. Respondent had increased the base price of his products to make good loss which had occurred due to of ITC post GST rate reduction.

ii. There was no reduction of rate of tax (GST) on 14.11.2017.

| Sl. No |

Name of the parties |

Citation |

Date of the Judgement |

| 9 |

Shri Ankur Jain (Applicant No. 1) & Director General Anti-Profiteering, Central Board of Indirect Taxes & Customs (Applicant No. 2) Vs M/s Kunj Lub Marketing Pvt. Ltd (Respondent) |

2018 (9) Tmi 1763 - National Anti-Profiteering Authority |

08-10-2018 |

Summary of Case No. 10/2018:

a. Facts

i. Applicant No. 1 was a retailer, doing business in the name and style of M/s. Anil Kumar Jain & Sons and to whom the Respondent had been selling Nestles products.

ii. An application through email dated 29.11.2017 was filed before the Standing Committee on Anti-Profiteering by Applicant No. 1.

iii. The application was examined by the Standing Committee on Anti-Profiteering in its meeting held on 20.12.2017, where it was decided to refer the matter to the Director General of Safeguards (DGSG), now re-designated as Director General of Anti-Profiteering (DGAP), for further investigation.

iv. Respondent was asked to suo-moto determine the quantum of benefit not passed on.

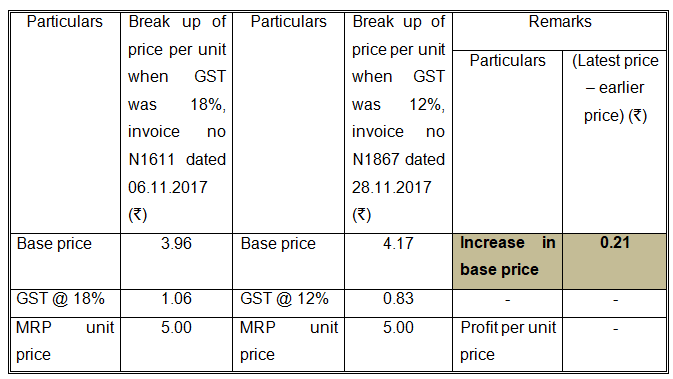

v. Applicant No.1 stated to have purchased Maggi Noodle packs, each weighing 35 Gms., having Maximum Retail Price (MRP) of Rs.5/- from the Respondent on 06.11.2017 vide invoice No. N1611 and on 28.11.2017 vide invoice No. N1867.

vi. Respondent was alleged to have charged base price of Rs. 3.96 per packet with tax (GST) @ 18% on it and increased base price to Rs. 4.17 per packet when tax (GST) was reduced to 12% so that cum-tax price remains unchanged at Rs. 4.67/- per packet.

vii. Respondent had claimed to have passed on the benefit of GST rate reduction in respect of the product bearing MRP of Rs. 5/- through other packs of Maggi Noodles having different grammage (Maggi Noodles pack of 70 Gms. Bearing MRP of Rs. 12/- per pack).

viii. Respondent further claims that benefit passed on was more than what it would have required to be passed on and the benefit of GST rate reduction had been passed on in respect of Maggie Noodles as a whole.

b. Issues

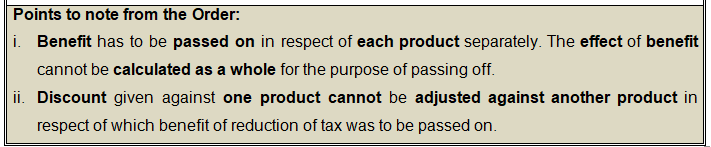

i. Whether the benefit accrued due to reduction in the rate of tax of one product can be passed on via another product or not

ii. Whether there was any violation on the provisions of Section 171 of the CGST Act, 2017 in this case

iii. If yes then what was the quantum of profiteering

c. Decision

i. The Respondent has contended that he had passed on the benefit in respect of the product by way of reducing the MRP of the 70 Gms. products. The Respondent has no such liberty to arbitrarily decide in respect of which products he would pass on the benefit and in respect of which products he would not pass such benefit. As per the provisions of Section 171 of the Act, the benefit has to be passed on to each recipient and the same cannot be selectively granted or denied as Maggi Noodle pack of 35 Gms is distinct from from a 70 Gms pack and both the packs may be bought by the different recipients /customers. Hence the benefit accruing to one customer cannot be given or denied to another nor can the benefit given to one set of customers arbitrarily enhanced and set off against the another. No such adjustments are permissible under the Act.

ii. The Respondent has resorted to profiteering of Re. 0.24/- per pack. It is beyond doubt that the benefit of reduction in the GST rate was not passed on to the recipients by way of commensurate reduction in the price charged by the Respondent which amounts to of the provisions of Section 171 of the CGST Act, 2017.

iii. Quantum of profiteering is determined as Rs. 90,778/- including the profiteering of Rs. 2,253/- made by the Respondent from Applicant No. . Accordingly he is directed to refund an amount of Rs. 2,253/- to the Applicant No.1 along with interest @18% p.a and is hereby directed to deposit the balance amount of Rs. 88,525/- along with interest at 18% p.a till the date of deposit in the respective Central or State Consumer Welfare Fund.

iv. The Respondent has realised more price from the consumers than the price he is entitled to and compelled them to pay more GST than they are required to pay by issuing incorrect invoices and hence committed offence under section 122 (1) (i) of the CGST Act, 2017 and therefore he is liable to for imposition of penalty. Accordingly, a Show Cause Notice be issued to the Respondent directing him to explain as to why the penalty prescribed under Section 122 of the above Act read with rule 133 (3) (d) of the CGST Rules, 2017 should not be imposed on him.

d. Ratio

i. Calculation of increase in base price in respect of Maggi Noodle packs, each weighing 35 Gms.

Conclusion:

i. It seems that there exists confusion regarding identifying commensurate reduction to prices which eventually culminates into profiteering in GST regime.

ii. The word commensurate has been defined in Cambridge dictionary to mean as in a correct and suitable amount compared to something else.

iii. As the word commensurate has been used and not equivalent, thereby intention of the law is not to take the overall facts and circumstances into consideration to decide whether profiteering has been done or not.

iv. Essentially there is no objection to profit in business but objection to profiteering out of the two reasons stated in the GST law.

v. In many a cases DGSG / DGAP has asked the Respondents to suo moto determine the benefits of reduction of tax.

vi. The author of the article is personally of the view that if cost records were maintained by all the Respondents, increase in costs and other factors, as discussed supra, could easily be identified there from. Authority may also consider to prescribe a format for reporting figures which would be unique to all or at least a format for suppliers of goods and a format for suppliers of services to maintain uniformity. Thus section 148 of the Companies Act, 2013 may suitably be amended.

vii. This will ease the task of the taxable persons to calculate how much benefits have been accrued to them.

viii. Elongated supply chain spanning across manufactures, distributors, retailers, etc make it difficult for manufacturer to ensure that the benefits of rate reductions are passed on at every stage so as to reach the end consumers, more particularly with respect to pipeline stock as on the date of reduction of tax.

ix. M/s. Pyramid Infratech Pvt. Ltd is reported to have filed a writ petition against the order in Delhi High Court alleging that the Anti-Profiteering mechanism lacks clarity.

x. Plenty of issues have been addressed through the Orders, discussed supra, many of them have been pointed out in this article under the heading points to note from the order, which appears to have been raised by the Respondents as those were not specifically mentioned in the law.

xi. Thus Government of India may consider to publish clarification to diffuse confusion in the form of either Notifications or Circulars clarifying the points mentioned against each order, as discussed supra, along with any other clarifications as deems fit.

Disclaimer: This publication contains information solely for education purpose only. It is neither a guidance note nor is a professional advice nor is intended to address any specific circumstance of any individual or entity. The undersigned does not accept any responsibility for loss incurred by any person for acting or refraining to act as a result of any matter in this publication.

About theAuthor :CMA. Susanta Kumar Saha

A seasoned professional with around 24 years experience in Corporate Finance, Direct & Indirect taxation, Financial & Management Accounting, Fund Management, Budgeting, ERP Implementation in different sectors of industry.

Corporate trainer in Goods and Services Tax, implementation and compliance consultant, advisory and litigation management.

13

13