Benefits of tonnage tax scheme extended to inland vessels [Budget 2025]:

![Benefits of tonnage tax scheme extended to inland vessels [Budget 2025]](https://assets.studycafe.in/uploads/2025/02/Income-Tax-Tonnage-tax-scheme.jpg)

Benefits of the Income Tax tonnage tax scheme has been proposed to be extended to inland vessels by Budget 2025

Income Tax Tonnage tax scheme

Benefits of tonnage tax scheme extended to inland vessels [Budget 2025]

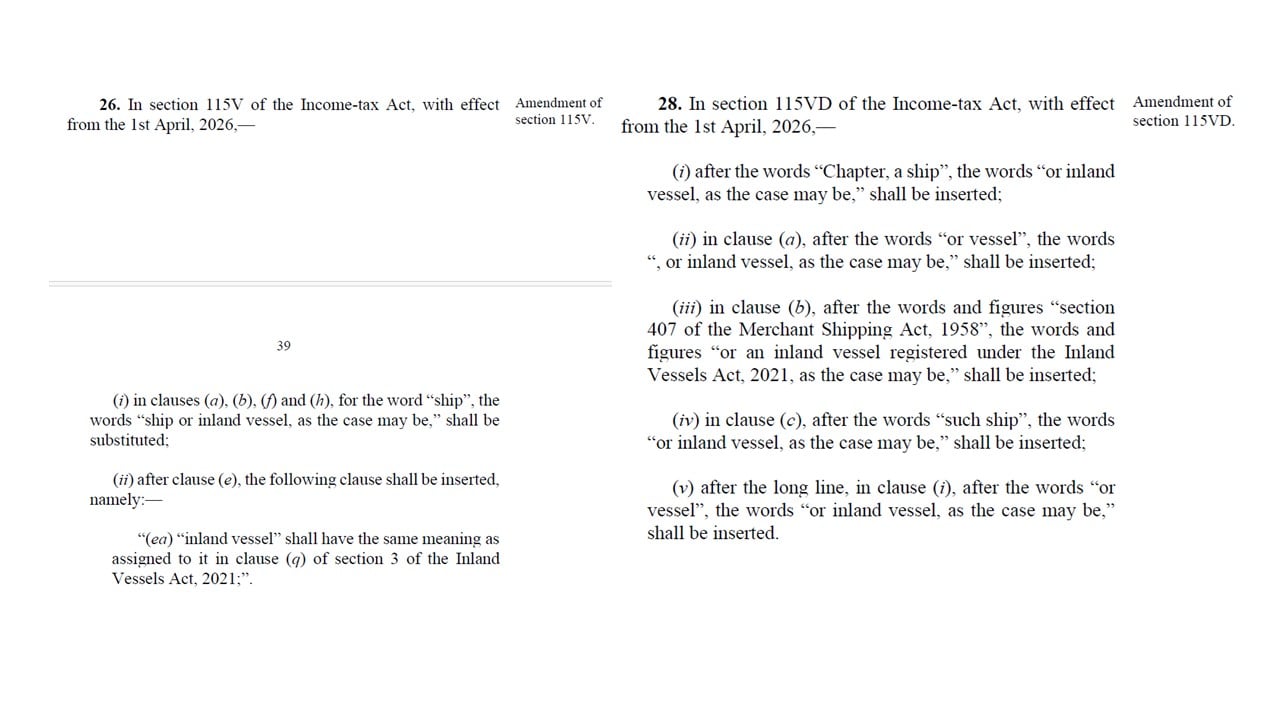

The Tonnage Tax scheme in Chapter XII-G of the Act was brought vide Finance Act, 2004 in order to promote Indian shipping industry wherein the qualifying shipping companies were given the choice to opt for the tonnage tax regime or continue to remain within the normal corporate tax regime.

Representations were received to extend tonnage tax scheme to inland vessels to promote inland water transportation industry. It is stated that at present, India is short of inland water transport vessels fleet and require higher investments in the sector which is capital intensive. Therefore, to provide a boost to inland water transportation, it was represented to include inland vessels under the ambit of tonnage tax scheme.

Therefore, to promote inland water transportation in the country and to attract investments in the sector, it is proposed to extend the benefits of tonnage tax scheme to Inland Vessels registered under Inland Vessels Act, 2021. Accordingly inland vessels have been included in the section 115VD for being eligible to be a qualified ship. Further, inland vessels have been defined in section 115V of the Act in the same manner as provided in the Inland Vessels Act, 2021. Other corresponding amendments have been made to extend the tonnage tax scheme to inland vessels.

These amendment will take effect from the 1st day of April, 2026 and shall, accordingly, apply in relation to the assessment year 2026-27 and subsequent assessment years.

These amendment will take effect from the 1st day of April, 2026 and shall, accordingly, apply in relation to the assessment year 2026-27 and subsequent assessment years.

These amendment will take effect from the 1st day of April, 2026 and shall, accordingly, apply in relation to the assessment year 2026-27 and subsequent assessment years.About Author

CA Pratibha Goyal

Co Founder

CA Pratibha Goyal is Chartered Accountant qualified in 2016, is a Member of The Institute of Chartered Accountants of India having wide experience in the field of Auditing, Taxation, ROC, GST and Secretarial matters etc.

She has written over a thousand articles & has made several videos on topics related to Auditing & Taxation. As a Speaker she has delivered various sessions on various branches of NIRC of ICAI.

CA Pratibha Goyal is Chartered Accountant qualified in 2016, is a Member of The Institute of Chartered Accountants of India having wide experience in the field of Auditing, Taxation, ROC, GST and Secretarial matters etc.

She has written over a thousand articles & has made several videos on topics related to Auditing & Taxation. As a Speaker she has delivered various sessions on various branches of NIRC of ICAI.

Studycafe

Studycafe New Delhi, Delhi, India

New Delhi, Delhi, India 1486

1486My Recent Articles

- Biggest Labour Reform in Indian History: 4 Labour Codes Effective from today

- Tax Audit and ITR Due date not extended in this case: Know More

- Government notifies Agreement and Protocol between India and Qatar [Read Notification]

- CA Breaking: Results of ICAI Examination to be announced soon, Know probable Date

- Breaking: GSTR-3B Due Date for September 2025 extended by CBIC amid Diwali Festivities

Up Next

Loading suggestions…

Recent Posts

All Posts

Tags

No tags yet.

Recent Posts

All Posts

Tags

No tags yet.