Best Judgement Assessment on non-furnishing of GST Returns

Best Judgement Assessment on non-furnishing of GST Returns CBIC has come with circular No. 129/48/2019-GST Standard Operating Procedure to b

Best Judgement Assessment on non-furnishing of GST Returns

CBIC has come with circular No. 129/48/2019-GST Standard Operating Procedure to be followed in case of non-filers of returns.

Before understanding Best Judgement Assessment, let us know Crux of Circular no.129/48/2019-GST dated 24th Dec 2019

1) Every Registered persons will get a reminder 3 days before due date to file their GST returns

2) once the due date is over, the registered person will get a auto msg stating that he has not filed the said return

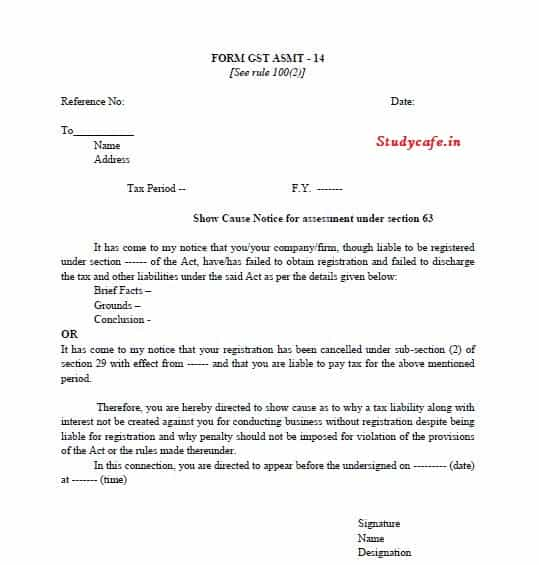

3) 5 days after the due date is over, the registered person will get a notice in form GSTR3A requiring him to furnish the said return within 15 days

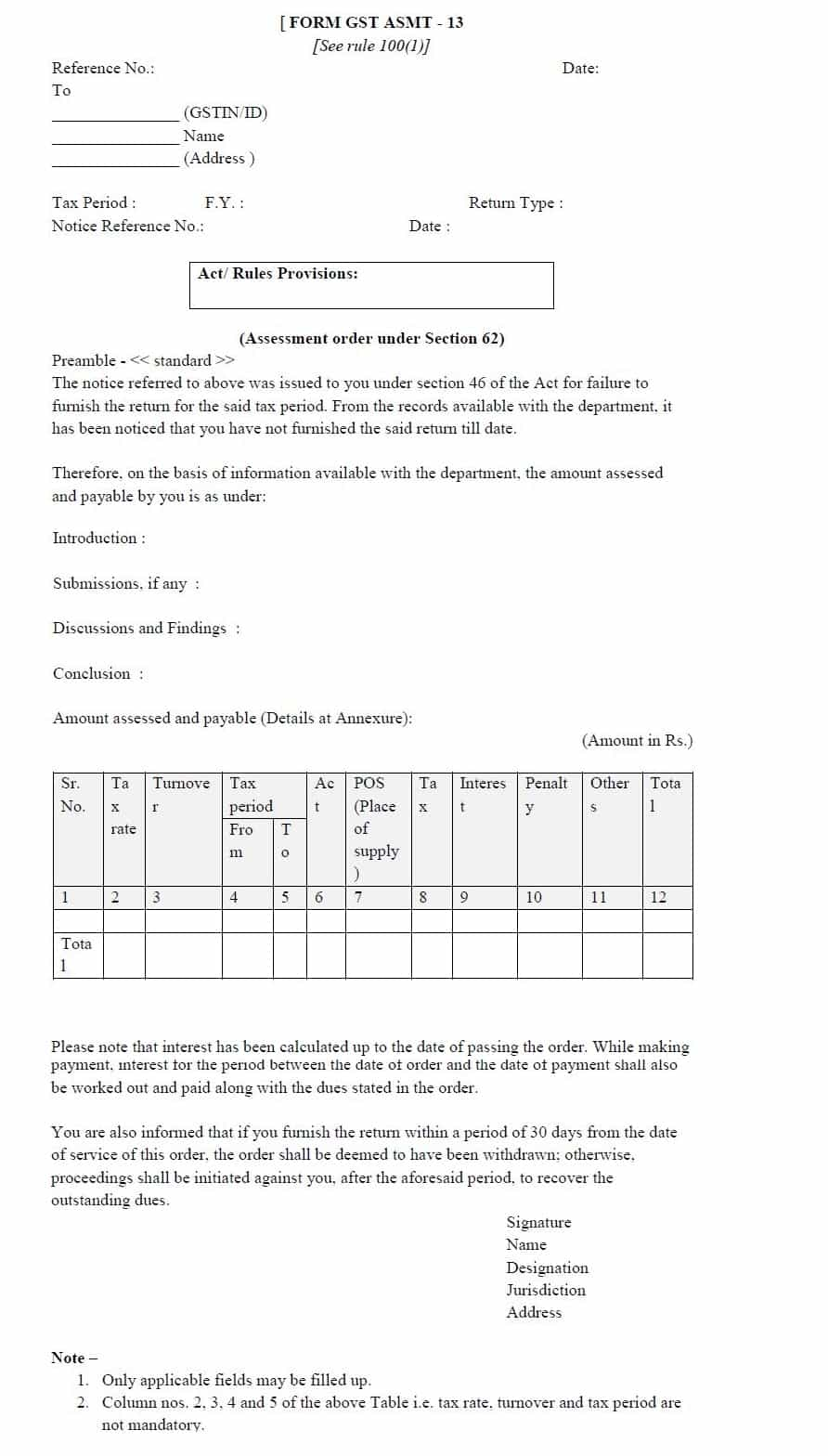

4) if the person doesn't file the return within 15 days, the officer will pass a best judgement assessment order in form GST ASMT 13 on thr basis of information like E-way bill, 2A or any other relevant information.

5) Now, the registered person gets a final opportunity to submit his return within 30 days from passing the above order, if he files then the order will stand withdrawn. If he doesn't, then the officer will start recovery proceedings u/s 79 and 80 for recovery of GST.

What is best Judgement Assessment in GST

Legal Text

Assessment of Non-Fillers of GST Return:

As per Section 62 of the CGST Act, 2017 provides :-

(1) Notwithstanding anything to the contrary contained in sec. 73 or sec. 74, where a registered person fails to furnished the return under sec. 39 or sec. 45, ever after the service of a notice under sec. 46, the proper officer may proceed to assess the tax liability of the said person to the best of his judgment taking into account all the relevant material which is available or which he has gathered and issue an assessment order within a period of five years from the date specified under sec. 44 or furnishing of the annual return for the financial year to which the tax not paid relates.

(2) Where the registered person furnishes a valid return within thirty days of the service of the assessment order under sub-section(1), the said assessment order shall be deemed to have been withdrawn but the liability for payment of interest under section 50 or for the payment of late fee under sec. 47 shall continue.

Assessment of Unregistered Person in GST:

As per section 63 of the CGST Act,2017, provides:-

Notwithstanding anything to the contrary contained in section 73 or sec.74, where a taxable person fails to obtain registration even though liable to do so or whose registration has been cancelled under sun-section (2) of section 29 but who was liable to pay tax, the proper officer may proceed to assess the tax liability of such taxable person to the best of his judgment for the relevant tax periods and issue an assessment order within a period of five years from the date specified under section 44 for furnishing of the annual return for the financial year to which the tax not paid relates:

Provided that no such assessment order shall passed without giving the person an opportunity of being heard.

Relevant Extract of Rule 100 of CGST Rules 2017

Assessment in certain cases.

100. (1) The order of assessment made under sub-section (1) of section 62 shall be issued in FORM GST ASMT-13 and a summary thereof shall be uploaded electronically in FORM GST DRC-07.

[caption id="attachment_85726" align="aligncenter" width="892"] Best Judgement Assessment on non-furnishing of GST Returns[/caption]

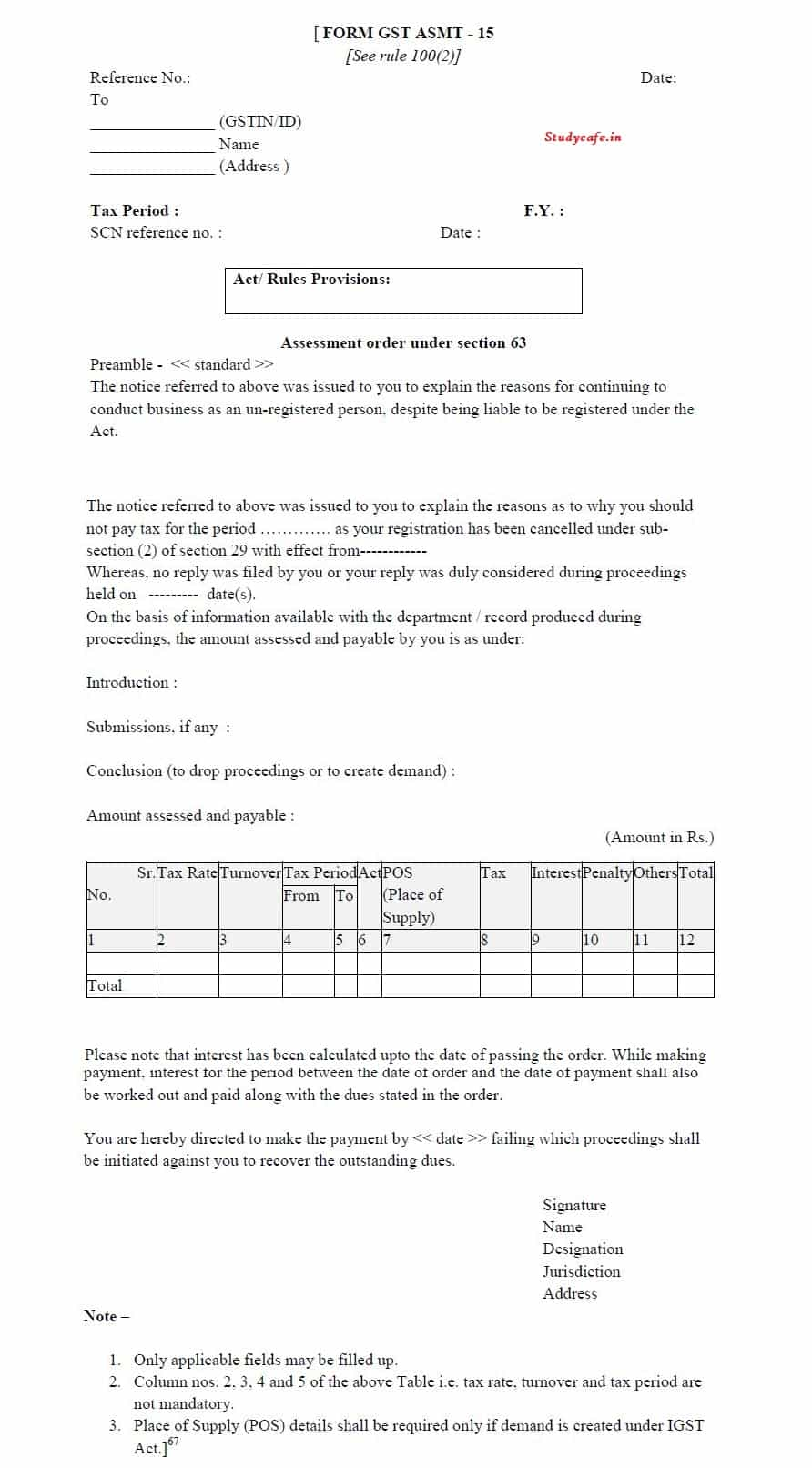

(2) The proper officer shall issue a notice to a taxable person in accordance with the provisions of section 63 in FORM GST ASMT-14 containing the grounds on which the assessment is proposed to be made on best judgment basis and shall also serve a summary thereof electronically in FORM GST DRC-01, and after allowing a time of fifteen days to such person to furnish his reply, if any, pass an order in FORM GST ASMT-15 and summary thereof shall be uploaded electronically in FORM GST DRC-07.

Best Judgement Assessment on non-furnishing of GST Returns[/caption]

(2) The proper officer shall issue a notice to a taxable person in accordance with the provisions of section 63 in FORM GST ASMT-14 containing the grounds on which the assessment is proposed to be made on best judgment basis and shall also serve a summary thereof electronically in FORM GST DRC-01, and after allowing a time of fifteen days to such person to furnish his reply, if any, pass an order in FORM GST ASMT-15 and summary thereof shall be uploaded electronically in FORM GST DRC-07.

[caption id="attachment_85728" align="aligncenter" width="892"] Best Judgement Assessment on non-furnishing of GST Returns[/caption]

Best Judgement Assessment is made by the AO, based on his reasoning and using the available information.

In GST situation of best judgement arises when:

[caption id="attachment_85728" align="aligncenter" width="892"] Best Judgement Assessment on non-furnishing of GST Returns[/caption]

Best Judgement Assessment is made by the AO, based on his reasoning and using the available information.

In GST situation of best judgement arises when:

Best Judgement Assessment on non-furnishing of GST Returns[/caption]

(2) The proper officer shall issue a notice to a taxable person in accordance with the provisions of section 63 in FORM GST ASMT-14 containing the grounds on which the assessment is proposed to be made on best judgment basis and shall also serve a summary thereof electronically in FORM GST DRC-01, and after allowing a time of fifteen days to such person to furnish his reply, if any, pass an order in FORM GST ASMT-15 and summary thereof shall be uploaded electronically in FORM GST DRC-07.

[caption id="attachment_85728" align="aligncenter" width="892"] Best Judgement Assessment on non-furnishing of GST Returns[/caption]

Best Judgement Assessment is made by the AO, based on his reasoning and using the available information.

In GST situation of best judgement arises when:

- the registered person has not filed his return

- the person is not registered for GST even though he is liable to

About Author

Pratibha Goyal

Admin

This Account belongs to Admistrator of Studycafe.

This Account belongs to Admistrator of Studycafe.

Studycafe

Studycafe Delhi, Delhi, India

Delhi, Delhi, India 1080

1080My Recent Articles

- Chartered Accountants Association Embraces Income Tax Faceless Proceedings

- CBDT condones delay in filing form 10IC for AY 20-21: Know upto when to file the form to take concessional tax benefit

- ICAI Announced date of Live Coaching Classes for CA Intermediate Nov 2022 Exam

- ICAI Announced Registration Date for Online Home-Based Practical Training Assessment

- ICAI Released Mock Test Papers Series for May 2022 CA Exam

Up Next

Loading suggestions…

Recent Posts

All Posts

Recent Posts

All Posts