Cancellation and Revocation of Cancellation of GST Registration

Cancellation and Revocation of Cancellation of GST Registration Cancellation of Registration under GST means that the registered person will no more …

Table of Contents

Cancellation and Revocation of Cancellation of GST Registration

Cancellation of Registration under GST means that the registered person will no more be registered under GST. The provisions regarding cancellation of registration is stated under section 29 of CGST Act, 2017.

The proper officer may, either on his own motion, or on an application filed by the registered person, or by his legal heirs (in case of death of such person), cancel the registration, in such manner and within such period as may be prescribed, cancel the registration, in such manner and within such period as may be prescribed.

Procedure to be followed by the registered person seeking cancellation of registration

As per Rule 20 of CGST Rules, 2017, a registered person other than:-- A person to whom a registration has been granted under Rule 12 i.e. tax deductor or tax collector, or

- A person to whom a Unique Identity Number has been granted under Rule 17,

- The details of inputs held in stock or inputs contained in semi-finished or finished goods held in stock, and of capital goods held in stock on the date from which the cancellation of registration is sought,

- Liability thereon,

- The details of the payment, if any, made against such liability, and

Procedure to be followed by the Proper officer for cancellation of registration

Rule 22 of the CGST Act, 2017 lays down the procedure to be followed by the proper officer for cancellation of registration. According, the procedure has been described as follows:- 1. Show cause notice (SCN) for cancellation of registration: Where the proper officer has reasons to believe that the registration of a person is liable to be canceled, he shall issue a notice to such person in Form GST REG-17, requiring him to show cause, within a period of 7 working days from the date of service of such notice, as to why his registration shall not be canceled. 2. Reply to SCN: The reply to the show-cause notice shall be furnished in Form GST REG-18 within 7 working days from the date of service of notice. 3. Order for cancellation of Registration: Where registration of a person is liable to be canceled, the proper officer shall issue the order of cancellation of registration within 30 days from the date of reply to SCN, in Form GST REG-19. 4. Effective date of cancellation: The cancellation of registration shall be effective from a date to be determined by the proper officer and mentioned in the cancellation order. He will direct the taxable person to pay arrears of any tax, interest, or penalty including the amount liable to be paid under section 29(5). 5. Dropping of proceedings for cancellation of Registration: If the reply to SCN is satisfactory, the proper officer shall drop the proceedings and pass an order in Form GST REG-20. However, where the person instead of replying to the SCN served for failure to furnish returns for a continuous period of 6 months (3 months in case of composition scheme supplier)furnishes all the pending returns and makes full payment of the tax dues along with applicable interest and late fee, the proper officer shall drop the proceedings and pass an order.Concept of final return

A taxable person whose GST registration is canceled or surrendered has to file a final return in the form of GSTR-10, within three months from the date of cancellation or date of cancellation order whichever is later, for the purpose of providing details of ITC involved in closing stock (including inputs and capital goods) to be reversed/ paid by the taxpayer.Other points to be noted

- A person to whom a UIN has been granted under rule 17 cannot apply for cancellation of registration [Rule 20].

- The cancellation of registration will not affect the liability of the registered person to pay tax and other dues under the Act for any period prior to the date of cancellation.

- The cancellation of registration under either SGST Act/UTGST Act shall be deemed to be a cancellation of registration under CGST Act [Section 29(4)].

- Once registration is canceled by the tax authority, the taxpayer will be intimated about the same via message and email. Order for cancellation of registration will be issued and intimated to the primary authorized signatory by email and message.

- The taxpayer would not be allowed to file a return for the period after the date of cancellation mentioned in the cancellation order. However, he can submit returns of the earlier period (i.e. for the period before the date of cancellation mentioned in the cancellation order for which registration was active).

Amount payable on cancellation of registration [Section 29(5) & (6)]

A registered person whose registration is canceled will have to debit the electronic credit or cash ledger by an amount equivalent to:-- input tax credit (ITC) in respect of:- (i) stock of inputs and inputs contained in semi-finished/finished goods’ stock or (ii) capital goods or plant and machinery on the day immediately preceding the date of cancellation, or

- the output tax payable on such goods

Revocation of cancellation of registration [Section 30 read with rule 23]

Revocation of cancellation of registration under GST simply means the restoration of GST registration. The following procedures has been laid down in this regard:-(A) Procedure for revocation of cancellation

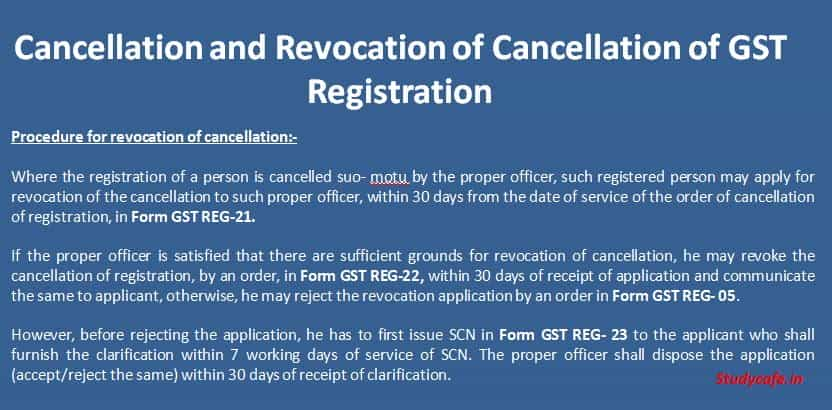

- Where the registration of a person is cancelled suo-motu by the proper officer, such registered person may apply for revocation of the cancellation to such proper officer, within 30 days from the date of service of the order of cancellation of registration, in Form GST REG-21.

- Provided that the period of 30 days may be increased by:

- the Additional Commissioner or the Joint Commissioner, as the case may be, for a period not exceeding 30 days

- and the Commissioner, for a further period not exceeding 30 days

- If the proper officer is satisfied that there are sufficient grounds for revocation of cancellation, he may revoke the cancellation of registration, by an order, in Form GST REG-22, within 30 days of receipt of application and communicate the same to applicant, otherwise, he may reject the revocation application by an order in Form GST REG- 05.

- However, before rejecting the application, he has to first issue SCN in Form GST REG- 23 to the applicant who shall furnish the clarification within 7 working days of service of SCN. The proper officer shall dispose the application (accept/reject the same) within 30 days of receipt of clarification.

(B) Where registration was cancelled for failure of registered person to furnish returns

Where registration was cancelled for failure of registered person to furnish returns, before applying for revocation, the person has to make good the defaults, i.e. the person needs to file such returns. However, the registration may have been cancelled by the proper officer either from the date of order of cancellation of registration or from a retrospective date.(1) Where the registration has been canceled with effect from the date of order of cancellation of registration

The common portal does not allow furnishing of returns after the effective date of cancellation, but returns for the earlier period (i.e. for the period before date of cancellation mentioned in the cancellation order) can be furnished after cancellation. Where the registration is cancelled with effect from the date of order of cancellation of registration, person applying for revocation of cancellation has to furnish all returns due till the date of such cancellation before the application for revocation can be filed and has to pay any amount due as tax, in terms of such returns along with any amount payable towards interest, penalties or late fee payable in respect of the said returns. However, since the portal does not allow to furnish returns after the date of cancellation of registration, all returns due for the period from the date of order of cancellation till the date of order of revocation of cancellation of registration have to be furnished within a period of 30 days from the date of the order of revocation.(2) Where the registration has been cancelled with retrospective Effect

Where the registration has been canceled with retrospective effect, it is not possible to furnish the returns before filing the application for revocation of cancellation of registration. In that case, the application for revocation of cancellation of registration is allowed to be filed, subject to the condition that all returns relating to the period from the effective date of cancellation of registration till the date of order of revocation of cancellation of registration shall be filed within a period of 30 days from the date of order of such revocation of cancellation of registration.About Author

Tista

Student

Delhi, Delhi, India

Delhi, Delhi, India 39

39Up Next

Loading suggestions…

Recent Posts

All Posts

Tags

Recent Posts

All Posts