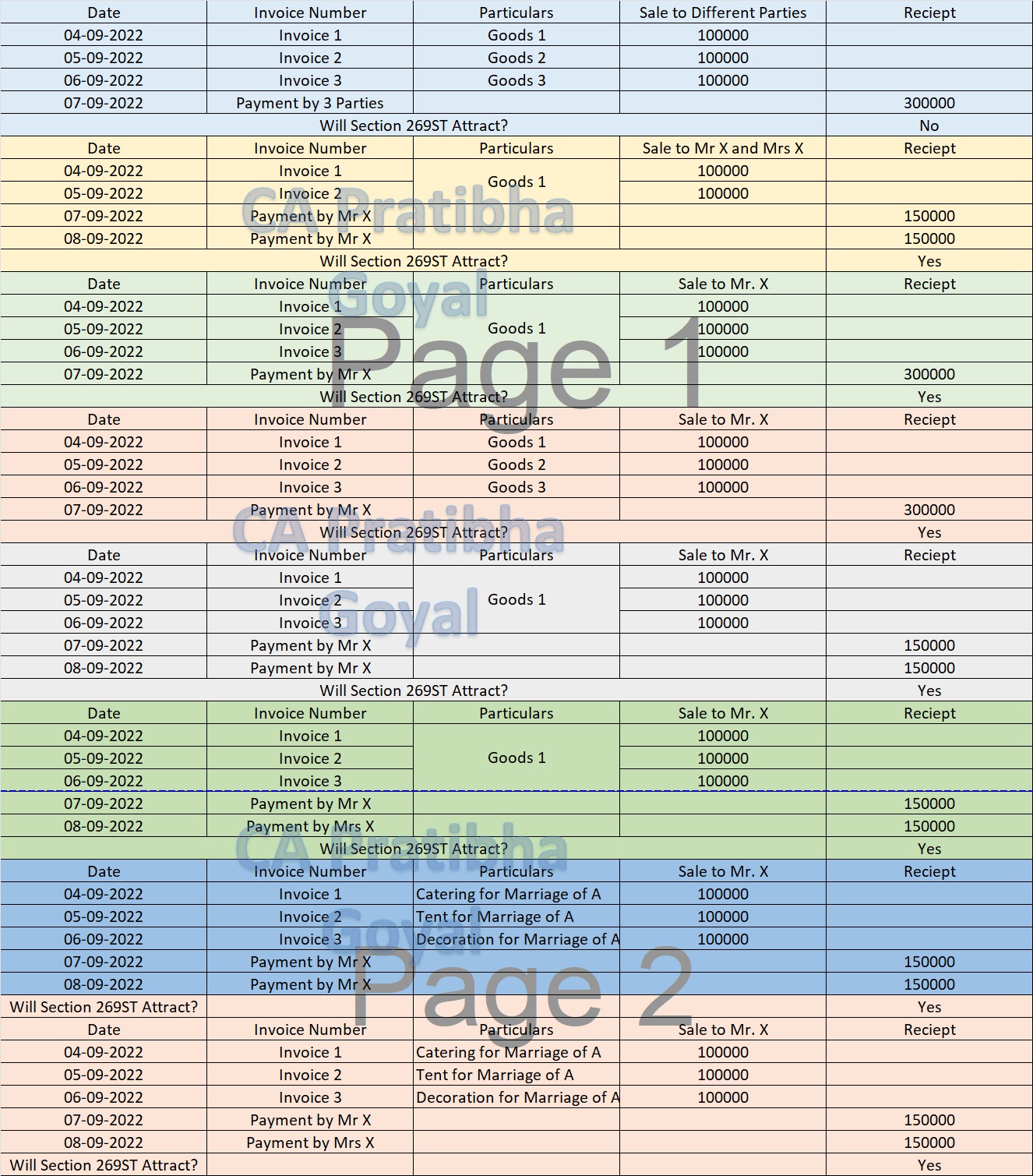

Case Studies on Section 269ST of Income Tax:

Section 269ST was introduced in Income Tax Act in 2017. Under this sec, no person can receive a payment above Rs.2 Lakhs in a single day.

Section 269ST of Income Tax

Table of Contents

Case Studies on Section 269ST of Income Tax

As per Section 269ST, no person shall receive an amount of two lakh rupees or more

(a) in aggregate from a person in a day; or

(b) in respect of a single transaction; or

(c) in respect of transactions relating to one event or occasion from a person,

otherwise than by an account payee cheque or an account payee bank draft or use of an electronic clearing system through a bank account or through such other electronic mode as may be prescribed.

The following entities are exempt u/s 269ST of Income Tax:

(a) Government;

(b) any banking company, post office savings bank or cooperative bank;

Further as per NOTIFICATION NO. SO 2065(E) [NO.57/2017 (F.NO.370142/10/2017-TPL)], DATED 3-7-2017 the provision of section 269ST shall not apply to the following, namely:

(a) receipt by a business correspondent on behalf of a banking company or co-operative bank, in accordance with the guidelines issued by the Reserve Bank of India;

(b) receipt by a white label automated teller machine operator from retail outlet sources on behalf of a banking company or co-operative bank, in accordance with the authorisation issued by the Reserve Bank of India under the Payment and Settlement Systems Act, 2007 (51 of 2007);

(c) receipt from an agent by an issuer of pre-paid payment instruments, in accordance with the authorisation issued by the Reserve Bank of India under the Payment and Settlement Systems Act, 2007 (51 of 2007);

(d) receipt by a company or institution issuing credit cards against bills raised in respect of one or more credit cards;

(e) receipt which is not includible in the total income under clause (17A) of section 10 of the Income-tax Act, 1961.

Case Studies on Section 269ST of Income Tax

About Author

CA Pratibha Goyal

Co Founder

CA Pratibha Goyal is Chartered Accountant qualified in 2016, is a Member of The Institute of Chartered Accountants of India having wide experience in the field of Auditing, Taxation, ROC, GST and Secretarial matters etc.

She has written over a thousand articles & has made several videos on topics related to Auditing & Taxation. As a Speaker she has delivered various sessions on various branches of NIRC of ICAI.

CA Pratibha Goyal is Chartered Accountant qualified in 2016, is a Member of The Institute of Chartered Accountants of India having wide experience in the field of Auditing, Taxation, ROC, GST and Secretarial matters etc.

She has written over a thousand articles & has made several videos on topics related to Auditing & Taxation. As a Speaker she has delivered various sessions on various branches of NIRC of ICAI.

Studycafe

Studycafe New Delhi, Delhi, India

New Delhi, Delhi, India 1486

1486My Recent Articles

- Biggest Labour Reform in Indian History: 4 Labour Codes Effective from today

- Tax Audit and ITR Due date not extended in this case: Know More

- Government notifies Agreement and Protocol between India and Qatar [Read Notification]

- CA Breaking: Results of ICAI Examination to be announced soon, Know probable Date

- Breaking: GSTR-3B Due Date for September 2025 extended by CBIC amid Diwali Festivities

Up Next

Loading suggestions…

Recent Posts

All Posts

Recent Posts

All Posts