TDS and TCS Due Date Chart for FY 2025-26 | AY 2026-27:

Read date chart for TDS and TCS Due Date Chart and TDS Rate Chart for FY 2025-26 or AY 2026-27.

TDS and TCS Due Date

Table of Contents

TDS and TCS Due Date Chart for FY 2025-26 | AY 2026-27

Tax Deducted at source (TDS) and Tax Collected at source (TCS) plays an important source of Tax collection for the Income Tax Department. Thus delay in collection or deduction of tax, delay in payment of TDS/TCS and filing TDS and TCS Return, leads to good quantum of Interest and Late fees.

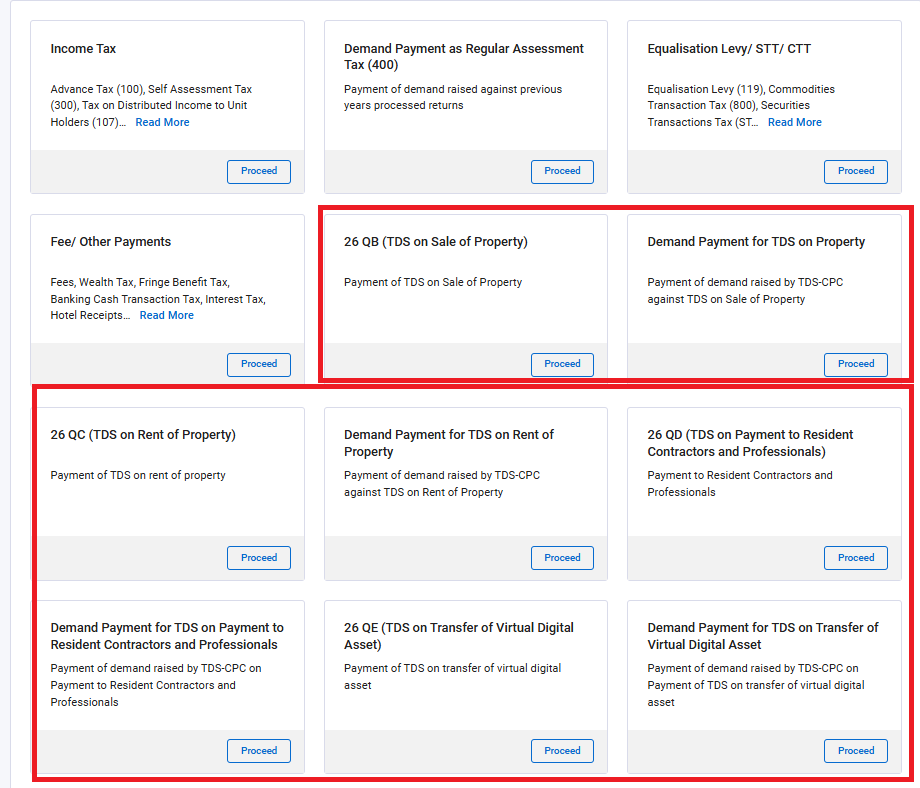

Income Tax Forms for Tax Payment/ Return Filing and Certificate

TAN is required for the filing of these returns.

However, there are certain transactions where TDS is applicable, but TAN is not required for Filing the TDS return. The Return Filing can be done with the PAN of the deductee.

These Transactions are:

TAN is required for the filing of these returns.

However, there are certain transactions where TDS is applicable, but TAN is not required for Filing the TDS return. The Return Filing can be done with the PAN of the deductee.

These Transactions are:

The Whole information is summarised in this image:

The Whole information is summarised in this image:

Interest applicable on Non-Deduction/ Collection or Late Deduction/ Collection of TDS and TCS

Non-Deduction/Collection of TDS/TCS

The interest of 1% is applicable on Non-Deduction/ Collection of TDS/TCS for the month or part of the month.

Non-payment to government after Deduction/Collection of TDS/TCS

The interest of 1.5% is applicable on Non-payment to government after Deduction/Collection of TDS/TCS for the month or part of the month.

Meaning of the month or part of the month:

Let's understand this with the help of an example. M/S ABC Limited made a payment of Rs. 45000 as professional Fees to Mr X. Payment was made on 6th April without deduction of TDS. Later on TDS of Rs was deducted on 3rd May and paid to the government on 10th August.

Interest for Non-Deduction between 6th April to 3rd May will be calculated as 4500 X 1% X 2 Months.

Interest for Non-payment between 3rd May to 10th August will be calculated as 4500 X 1.5% X 4 Months.

Late Filing fees of TDS and TCS returns

According to section 234E, if an individual does not submit the TDS/TCS statement by the deadline specified by the Income Tax Act of 1961, they will be responsible for paying INR 200 for each day that the failure persists.

Maximum of Late Filing fees which can be charged

The total amount of TDS/TCS deducted or collected cannot be greater than the amount of late filing costs.

So basically we need to take care of Late deduction, Late Payment and Late Filing Fees:

Interest applicable on Non-Deduction/ Collection or Late Deduction/ Collection of TDS and TCS

Non-Deduction/Collection of TDS/TCS

The interest of 1% is applicable on Non-Deduction/ Collection of TDS/TCS for the month or part of the month.

Non-payment to government after Deduction/Collection of TDS/TCS

The interest of 1.5% is applicable on Non-payment to government after Deduction/Collection of TDS/TCS for the month or part of the month.

Meaning of the month or part of the month:

Let's understand this with the help of an example. M/S ABC Limited made a payment of Rs. 45000 as professional Fees to Mr X. Payment was made on 6th April without deduction of TDS. Later on TDS of Rs was deducted on 3rd May and paid to the government on 10th August.

Interest for Non-Deduction between 6th April to 3rd May will be calculated as 4500 X 1% X 2 Months.

Interest for Non-payment between 3rd May to 10th August will be calculated as 4500 X 1.5% X 4 Months.

Late Filing fees of TDS and TCS returns

According to section 234E, if an individual does not submit the TDS/TCS statement by the deadline specified by the Income Tax Act of 1961, they will be responsible for paying INR 200 for each day that the failure persists.

Maximum of Late Filing fees which can be charged

The total amount of TDS/TCS deducted or collected cannot be greater than the amount of late filing costs.

So basically we need to take care of Late deduction, Late Payment and Late Filing Fees:

Download TDS Rate Chart for FY 2025-26 in PDF. Form

Download TDS Rate Chart for FY 2025-26 in PDF. Form

Download TCS Rate Chart for FY 2025-26 in PDF. Form

Hope you find this material helpful.

Download TCS Rate Chart for FY 2025-26 in PDF. Form

Hope you find this material helpful.

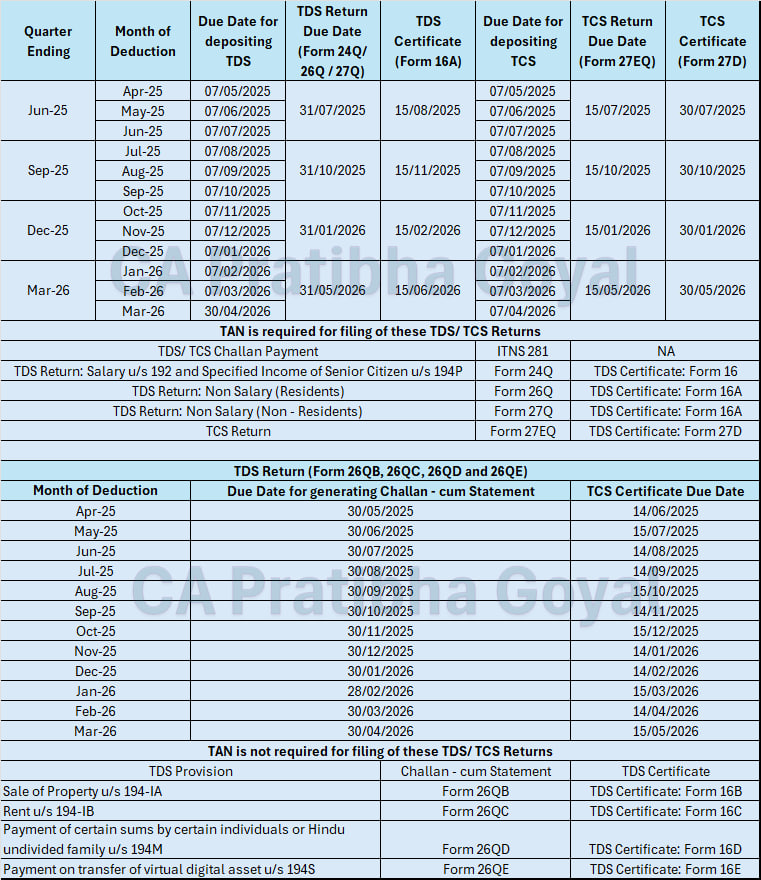

What are the due dates?

TDS The due date for depositing TDS is the 7th of next month. Only for the month of March, the TDS can be deposited up to 30th April. The Due date to file TDS Return for Quarter 1 (April to June), Quarter 2 (July to September), Quarter 3 (October to December) and Quarter 4 (January to March) is 31st July, 31st October, 31st December and 31st May, respectively. TDS Certificate is required to be issued within 15 Days of Return Filing. However Salary TDS Certificate has to be generated within 15 days of the TDS Return filing of Last Quarter. TCS The due date for depositing TCS is the 7th of next month. The Due date to file TCS Return for Quarter 1 (April to June), Quarter 2 (July to September), Quarter 3 (October to December) and Quarter 4 (January to March) is 15th July, 15th October, 15th December and 15th May, respectively. TCS Certificate is required to be issued within 15 Days of Return Filing. Here is a due date chart for TDS and TCS Due Date Chart for FY 2025-26 | AY 2026-27| Quarter Ending | Month of Deduction | Due Date for depositing TDS | TDS Return Due Date (Form 24Q/ 26Q / 27Q) | TDS Certificate (Form 16A) | Due Date for depositing TCS | TCS Return Due Date (Form 27EQ) | TCS Certificate (Form 27D) |

| Jun-25 | Apr-25 | 07/05/2025 | 31/07/2025 | 15/08/2025 | 07/05/2025 | 15/07/2025 | 30/07/2025 |

| May-25 | 07/06/2025 | 07/06/2025 | |||||

| Jun-25 | 07/07/2025 | 07/07/2025 | |||||

| Sep-25 | Jul-25 | 07/08/2025 | 31/10/2025 | 15/11/2025 | 07/08/2025 | 15/10/2025 | 30/10/2025 |

| Aug-25 | 07/09/2025 | 07/09/2025 | |||||

| Sep-25 | 07/10/2025 | 07/10/2025 | |||||

| Dec-25 | Oct-25 | 07/11/2025 | 31/01/2026 | 15/02/2026 | 07/11/2025 | 15/01/2026 | 30/01/2026 |

| Nov-25 | 07/12/2025 | 07/12/2025 | |||||

| Dec-25 | 07/01/2026 | 07/01/2026 | |||||

| Mar-26 | Jan-26 | 07/02/2026 | 31/05/2026 | 15/06/2026 | 07/02/2026 | 15/05/2026 | 30/05/2026 |

| Feb-26 | 07/03/2026 | 07/03/2026 | |||||

| Mar-26 | 30/04/2026 | 07/04/2026 |

| TDS/ TCS Challan Payment | ITNS 281 | NA | |||||

| TDS Return: Salary u/s 192 and Specified Income of Senior Citizen u/s 194P | Form 24Q | TDS Certificate: Form 16 | |||||

| TDS Return: Non Salary (Residents) | Form 26Q | TDS Certificate: Form 16A | |||||

| TDS Return: Non Salary (Non - Residents) | Form 27Q | TDS Certificate: Form 16A | |||||

| TCS Return | Form 27EQ | TDS Certificate: Form 27D | |||||

TAN is required for the filing of these returns.

However, there are certain transactions where TDS is applicable, but TAN is not required for Filing the TDS return. The Return Filing can be done with the PAN of the deductee.

These Transactions are:

- TDS on Sale of Property u/s 194-IA: Challan - cum Statement is Form 26QB and TDS Certificate is in Form 16B

- TDS on Rent u/s 194-IB: Challan - cum Statement is Form 26QC and TDS Certificate is in Form 16C

- TDS on Payment of Certain Sums by Certain Individuals or Hindu Undivided Family u/s 194M: Challan - cum Statement is Form 26QD and TDS Certificate is in Form 16D

- TDS on Payment on transfer of virtual digital asset u/s 194S: Challan - cum Statement is Form 26QE and TDS Certificate is in Form 16E

| TDS Return (Form 26QB, 26QC, 26QD and 26QE) | |||||||

| Month of Deduction | Due Date for generating Challan - cum Statement | TCS Certificate Due Date | |||||

| Apr-25 | 30/05/2025 | 14/06/2025 | |||||

| May-25 | 30/06/2025 | 15/07/2025 | |||||

| Jun-25 | 30/07/2025 | 14/08/2025 | |||||

| Jul-25 | 30/08/2025 | 14/09/2025 | |||||

| Aug-25 | 30/09/2025 | 15/10/2025 | |||||

| Sep-25 | 30/10/2025 | 14/11/2025 | |||||

| Oct-25 | 30/11/2025 | 15/12/2025 | |||||

| Nov-25 | 30/12/2025 | 14/01/2026 | |||||

| Dec-25 | 30/01/2026 | 14/02/2026 | |||||

| Jan-26 | 28/02/2026 | 15/03/2026 | |||||

| Feb-26 | 30/03/2026 | 14/04/2026 | |||||

| Mar-26 | 30/04/2026 | 15/05/2026 | |||||

The Whole information is summarised in this image:

Interest applicable on Non-Deduction/ Collection or Late Deduction/ Collection of TDS and TCS

Non-Deduction/Collection of TDS/TCS

The interest of 1% is applicable on Non-Deduction/ Collection of TDS/TCS for the month or part of the month.

Non-payment to government after Deduction/Collection of TDS/TCS

The interest of 1.5% is applicable on Non-payment to government after Deduction/Collection of TDS/TCS for the month or part of the month.

Meaning of the month or part of the month:

Let's understand this with the help of an example. M/S ABC Limited made a payment of Rs. 45000 as professional Fees to Mr X. Payment was made on 6th April without deduction of TDS. Later on TDS of Rs was deducted on 3rd May and paid to the government on 10th August.

Interest for Non-Deduction between 6th April to 3rd May will be calculated as 4500 X 1% X 2 Months.

Interest for Non-payment between 3rd May to 10th August will be calculated as 4500 X 1.5% X 4 Months.

Late Filing fees of TDS and TCS returns

According to section 234E, if an individual does not submit the TDS/TCS statement by the deadline specified by the Income Tax Act of 1961, they will be responsible for paying INR 200 for each day that the failure persists.

Maximum of Late Filing fees which can be charged

The total amount of TDS/TCS deducted or collected cannot be greater than the amount of late filing costs.

So basically we need to take care of Late deduction, Late Payment and Late Filing Fees:

| Type of Deduction | Description | Formula for Late Fees/Interest |

| Late Deduction | TDS Not Deducted | Interest = (TDS/ TCS on Amount Paid/ Credited X Period of Delay X 1.5%) |

| Late Fees | Failure to file TDS/ TCS Return on/ Before Due date | Late Filing Fee = INR 200 per Day (Fees cannot Exceed TDS/ TCS Amount) |

| Late Payment | TDS Deducted but not deposited | Interest = (TDS/ TCS Not Deposited X Period of Delay X 1.5%) |

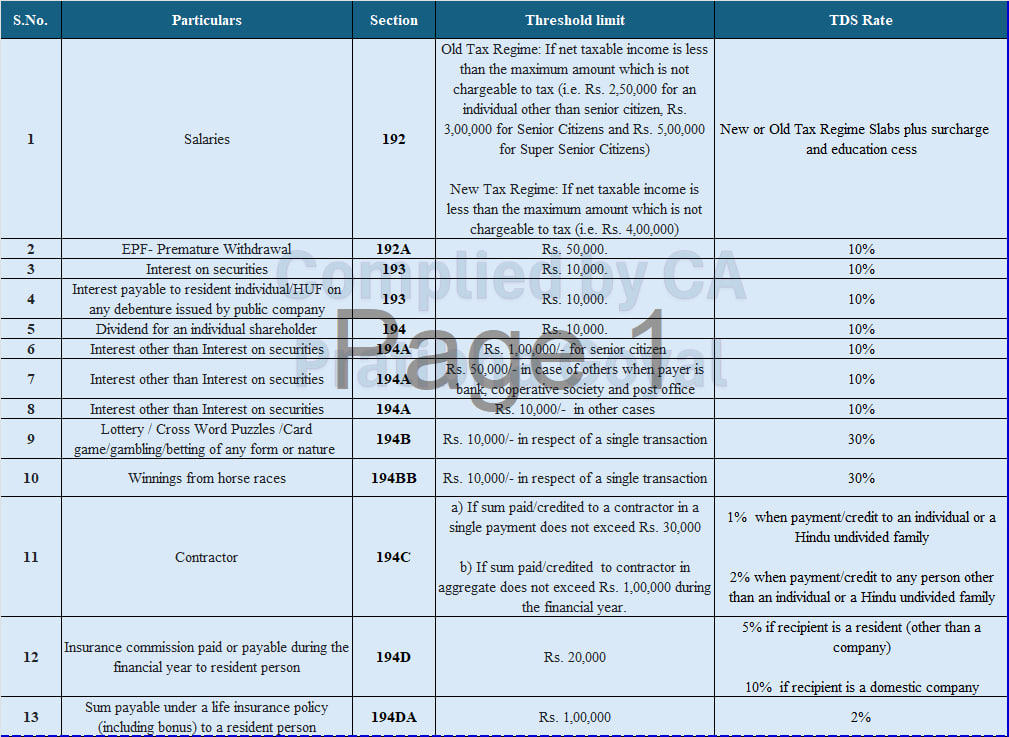

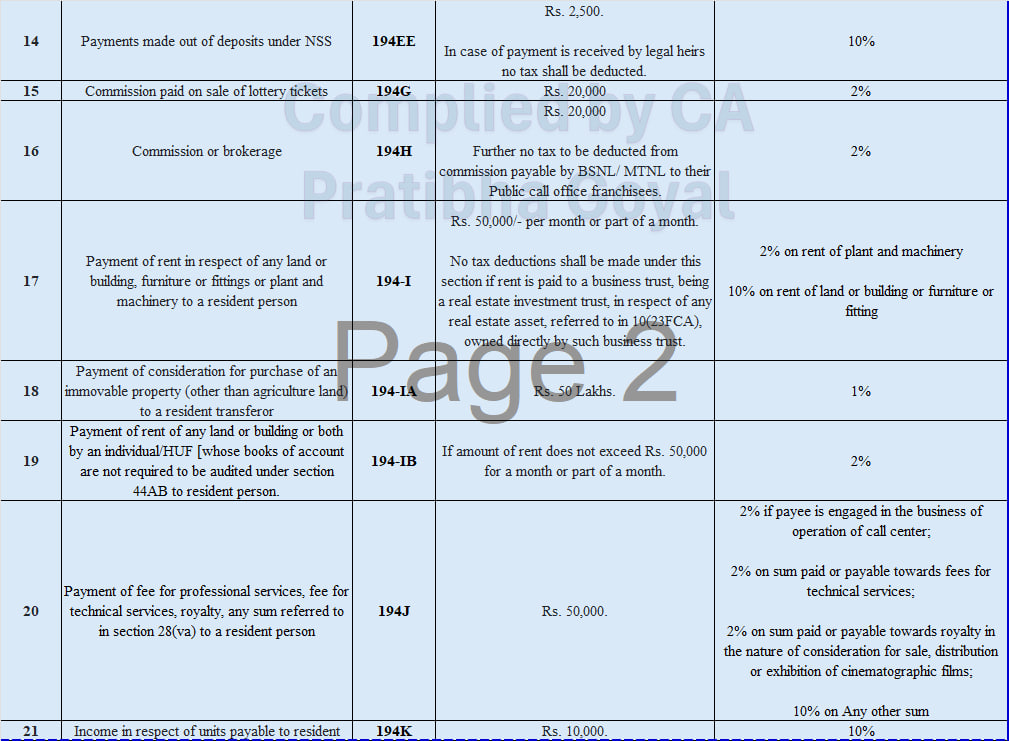

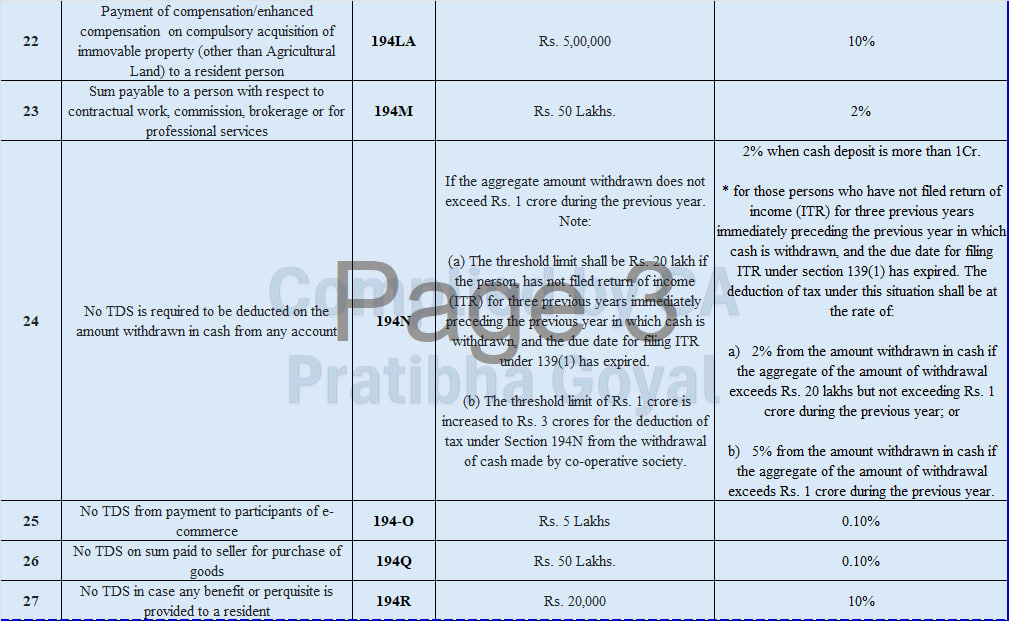

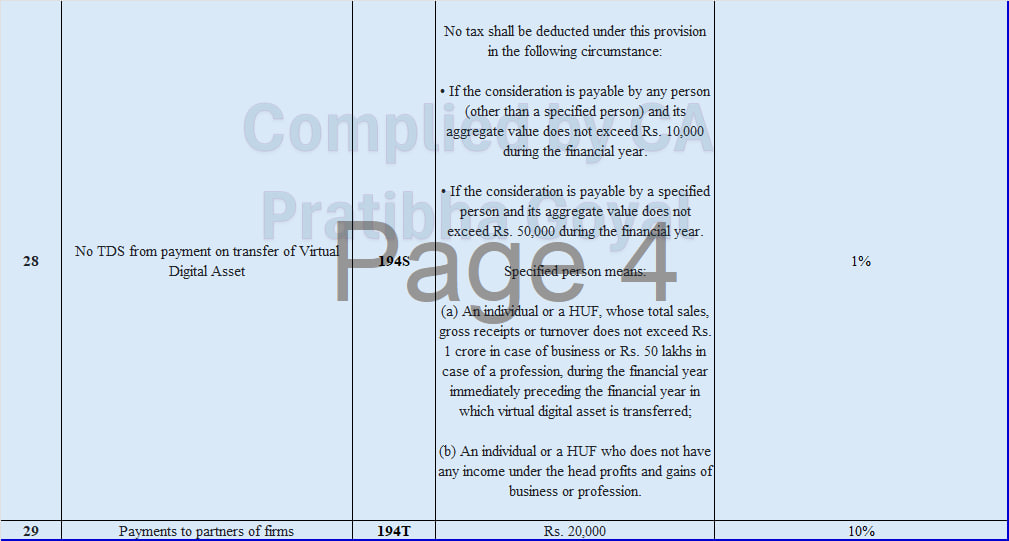

TDS Rate Chart for FY 2025-26 | AY 2026-27

TDS Rate Chart - Page 2

TDS Rate Chart - Page 3

TDS Rate Chart - Page 4

Download TDS Rate Chart for FY 2025-26 in PDF. Form

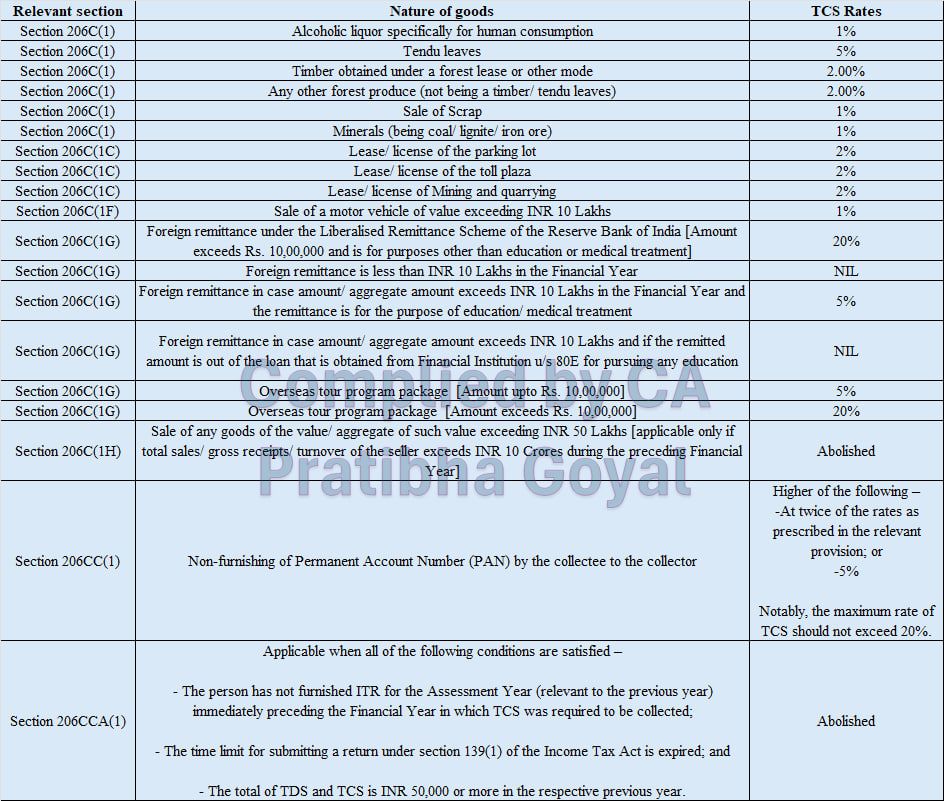

TCS Rate Chart for FY 2025-26 | AY 2026-27

Download TCS Rate Chart for FY 2025-26 in PDF. Form

Hope you find this material helpful.About Author

CA Pratibha Goyal

Co Founder

CA Pratibha Goyal is Chartered Accountant qualified in 2016, is a Member of The Institute of Chartered Accountants of India having wide experience in the field of Auditing, Taxation, ROC, GST and Secretarial matters etc.

She has written over a thousand articles & has made several videos on topics related to Auditing & Taxation. As a Speaker she has delivered various sessions on various branches of NIRC of ICAI.

CA Pratibha Goyal is Chartered Accountant qualified in 2016, is a Member of The Institute of Chartered Accountants of India having wide experience in the field of Auditing, Taxation, ROC, GST and Secretarial matters etc.

She has written over a thousand articles & has made several videos on topics related to Auditing & Taxation. As a Speaker she has delivered various sessions on various branches of NIRC of ICAI.

Studycafe

Studycafe New Delhi, Delhi, India

New Delhi, Delhi, India 1486

1486My Recent Articles

- Biggest Labour Reform in Indian History: 4 Labour Codes Effective from today

- Tax Audit and ITR Due date not extended in this case: Know More

- Government notifies Agreement and Protocol between India and Qatar [Read Notification]

- CA Breaking: Results of ICAI Examination to be announced soon, Know probable Date

- Breaking: GSTR-3B Due Date for September 2025 extended by CBIC amid Diwali Festivities

Up Next

Loading suggestions…

Recent Posts

All Posts

Tags

No tags yet.

Recent Posts

All Posts

Tags

No tags yet.