CBDT issued Circular to remove difficulty in implementation of changes relating to TCS on LRS and and Overseas Tour Packages:

The Central Board of Direct Taxes has issued Circular to remove difficulty in implementation of changes relating to TCS on LRS and and Overseas Tour Packages.

Removal of difficulty relating to TCS on LRS and and Overseas Tour Packages

Table of Contents

CBDT issued Circular to remove difficulty in implementation of changes relating to TCS on LRS and and Overseas Tour Packages

The Central Board of Direct Taxes(CBDT) has issued Circular to remove difficulty in implementation of changes relating to Tax Collection at Source (TCS) on Liberalised Remittance Scheme (LRS) and on purchase of overseas tour program package.

Finance Act,2023 has amended sub-section (1G) of section 206C of the Income-tax Act, 1961 (hereinafter referred to as 'the Act') to, interalia,

(i) increase the rate of Tax Collection at Source (TCS) from 5% to 20% for remittance under LRS as well as for purchase of overseas tour program package; and

(ii) remove the threshold of Rs 7 lakh for triggering TCS on LRS.

These two amendments did not apply when the remittance was for educational or medical purposes.

Following that, the government notified the Foreign Exchange Management (Current Account Transactions) (Amendment) Rules, 2023 via an e-gazette notification dated May 16, 2023 to remove the differential treatment for credit cards vs other forms of drawing foreign Exchange under LRS. For the time being, this adjustment has been postponed.

There have been comments regarding the practical challenges that may occur as a result of the lifting of the bar for LRS payments other than for education and medical treatment. During the meet with the RBI, banks, and card networks, certain financial institutions requested additional time to adjust their present IT systems to solve concerns resulting from the introduction of the provision of TCS on credit card transactions.

ln order to address these issues, a Press Release dated 28.6.2023 (copy enclosed) was issued by Ministry of Finance wherein the following decisions relating to income-tax have been taken:

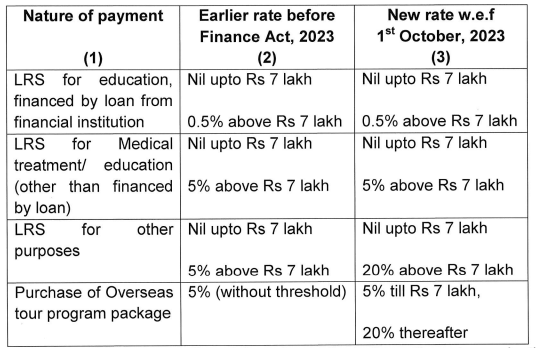

i) Threshold of Rs.7 lakh per financial year per individual in clause (i) of sub-section (1G) of section 206C shall be restored for TCS on all categories of LRS payments, through all modes of payment, regardless of the purpose: Thus, for first Rs.7 lakh remittance under LRS there shall be no TCS. Beyond this Rs.7 lakh threshold, TCS shall be at the rate of -

a) 0.5% (if remittance for education is financed by loan taken from a financial institution);

b) 5% (in case of remittance for education/medical treatment);

c) 200 % for others.

The TCS shall continue to apply at the rate of 5o/o for the first Rs.7 lakh per individual per annum1 for the purchase of an overseas trip programme package under clause (ii) of sub-section (1G) of section 206C; the 20o/o rate will only apply for spending over this level.

ii) Increased TCS rates to apply from 1st October, 2023:

The increase in TCS rates, which was scheduled to take effect on July 1, 2023, will instead take effect on October 1, 2023, with the revision described in (i) above. Till 30th September,2023, earlier rates (prior to amendment by the Finance Act, 2023) shall continue to apply.

Earlier and new TCS rates are summarised as under:

*Note: (i) TCS rate mentioned in column 2 shall continue to apply till 30th September,2023.

(ii) There shall be no TCS on expenditure under LRS under clause (i) of subsection (1G) of section 206C upto Rs.7 lakh, irrespective of purpose.

Section 206C of the Act specifies that if any problem occurs in carrying out the requirements of sub-section (1G) of this section, the Board may, with the agreement of the Central Government, provide recommendations to remove the impediment. As a result, the following guidance is offered in accordance with this law.

FAQs with respect to removal of difficulty relating to TCS on LRS

*Note: (i) TCS rate mentioned in column 2 shall continue to apply till 30th September,2023.

(ii) There shall be no TCS on expenditure under LRS under clause (i) of subsection (1G) of section 206C upto Rs.7 lakh, irrespective of purpose.

Section 206C of the Act specifies that if any problem occurs in carrying out the requirements of sub-section (1G) of this section, the Board may, with the agreement of the Central Government, provide recommendations to remove the impediment. As a result, the following guidance is offered in accordance with this law.

FAQs with respect to removal of difficulty relating to TCS on LRS

*Note: (i) TCS rate mentioned in column 2 shall continue to apply till 30th September,2023.

(ii) There shall be no TCS on expenditure under LRS under clause (i) of subsection (1G) of section 206C upto Rs.7 lakh, irrespective of purpose.

Section 206C of the Act specifies that if any problem occurs in carrying out the requirements of sub-section (1G) of this section, the Board may, with the agreement of the Central Government, provide recommendations to remove the impediment. As a result, the following guidance is offered in accordance with this law.

FAQs with respect to removal of difficulty relating to TCS on LRS

Question 1: Whether payment through overseas credit card would be counted in LRS?

As indicated in a press release on June 28th, 2023, the classification of use of an international credit card while abroad as LRS has been postponed. As a result, no TCS will be applied to foreign credit card purchases made while travelling abroad until further notice.Question 2: Whether the threshold of Rs 7 lakh, for TCS to become applicable on LRS, applies separately for various purposes like education, health treatment and others? For example, if remittance of Rs 7 lakh under LRS is made in a financial year for education purpose and other remittances in the same financial year of Rs.7 lakh is made for medical treatment and Rs 7 lakh for other purposes, whether the exemption limit of Rs 7 lakh shall be given to each of the three separately?

It is emphasised that the Rs 7 lakh threshold for LRS is a combined requirement for TCS application on LRS regardless of the purpose of the remittance. This is obvious from the first proviso to sub-section (1G) of Section 206C of the Act. The proviso indicates that the TCS is not required if a buyer's total amount remitted in a financial year is less than seven lakh rupees. The revision made by the Finance Act of 2023 solely limited it to educational and medical treatment purposes. Now, following the press announcement, the former position has been reinstated, and the seven lakh rupee requirement remains to apply, regardless of the objective. Thus, in the given example, upto Rs.7 lakh remittance under LRS during a financial year shall not be liable for TCS. However, subsequent Rs 14 lakh remittance under LRS shall be liable for TCS in accordance with the TCS rates applicable for such remittance. For example, if remittances under LRS are made at different times within the current financial year, TCS rates for the remaining Rs.14 lakh remittances under LRS will be determined by the time of transfer, as TCS rates will change on October 1, 2023. TCS rates would be applicable as under:-- First Rs.7 lakh remittance under LRS during the financial year 2023-24 for education purpose (or for that matter any purpose) -> No TCS.

- Remittances beyond Rs.7 lakh under LRS during the financial year 2023-24, if on or before 30th September 2023 -> TCS at 5% (irrespective of the purpose unless it is for education purpose financed by loan from a financial institution when the rate is 0.5%).

- Remittances beyond Rs.7 lakh under LRS during the financial year 2023-24, if on or after 1st October 2023 ) TCS at O.5% (if it is for education purpose financed by loan from a financial institution), 5% (if it is for education or medical treatment) and 20% (if it is for other purposes).

Question 3: Since there are different TCS rates on LRS for the first six months and next six months of the financial year 2023-24, whether the threshold of Rs.7 lakh, for the TCS to become applicable on LRS, applies separately for each six months?

No. The threshold of Rs.7 lakh, for the TCS to become applicable on LRS, applies for the full financial year. If this threshold has already been exhausted; all subsequent remittances under LRS, whether in the first half or in the second half, would be liable for TCS at applicable rate. To Read More Download Official PDF Given Below:About Author

Reetu

Content Manager

Reetu is a Content Writer with 4+ years of experience in GST, Income Tax, Finance, Company Law, Education and Career Related Content. She is a B.COM (Honrs.) Graduate.

Reetu is a Content Writer with 4+ years of experience in GST, Income Tax, Finance, Company Law, Education and Career Related Content. She is a B.COM (Honrs.) Graduate.

Studycafe

Studycafe Delhi, Delhi, India

Delhi, Delhi, India 8072

8072My Recent Articles

- Income Tax Guide for Indian Defence Personnel for Tax Filing, Taxable Allowances and Other Benefits

- Income Tax Return Breaking: ITR Forms released for AY 25-26

- Ex-DRT Officials Sentenced to 5 Years Rigorous Imprisonment by Madras High Court along with Rs.27 Lakh Fine

- GSTN issued Advisory on Case Sensitivity in IRN Generation

- RBI to issue Notes of Rs.10 and Rs.500 bearing Signature of Guv Malhotra

Up Next

Loading suggestions…

Recent Posts

All Posts

Tags

Recent Posts

All Posts