CBDT Revises Tax Audit Form 3CD and amends Rule 6G

CBDT Revises Tax Audit Form 3CD and amends Rule 6G Central Board of Direct Taxes [CBDT] has made an amendment in Tax Audit Form [Form 3CD] and amends…

CBDT Revises Tax Audit Form 3CD and amends Rule 6G

Central Board of Direct Taxes [CBDT] has made an amendment in Tax Audit Form [Form 3CD] and amends Rule 6G. As per the notification, now the assessee can revise form 3CD which is necessitated by recalculation of disallowance under section 40 or section 43B.

(iii) in clause 18, for sub-clauses (ca) and (cb), the following sub-clauses, shall be substituted namely:-

“(ca) Adjustment made to the written down value under section 115BAC/115BAD (for assessment year 2021-2022 only)……

(cb) Adjustment made to written down value of Intangible asset due to excluding value of goodwill of a business or profession…..

(cc) Adjusted written down value……….”;

(iv) in clause 32, for sub-clause (a), the following sub-clause shall be substituted, namely:-

(a) Details of brought forward loss or depreciation allowance, in the following manner, to the extent available:

(iii) in clause 18, for sub-clauses (ca) and (cb), the following sub-clauses, shall be substituted namely:-

“(ca) Adjustment made to the written down value under section 115BAC/115BAD (for assessment year 2021-2022 only)……

(cb) Adjustment made to written down value of Intangible asset due to excluding value of goodwill of a business or profession…..

(cc) Adjusted written down value……….”;

(iv) in clause 32, for sub-clause (a), the following sub-clause shall be substituted, namely:-

(a) Details of brought forward loss or depreciation allowance, in the following manner, to the extent available:

*If the assessed depreciation is less and no appeal pending then take assessed.

^To be filled in for assessment year 2021-2022 only.’’:

(v) clause 36 shall be omitted.

*If the assessed depreciation is less and no appeal pending then take assessed.

^To be filled in for assessment year 2021-2022 only.’’:

(v) clause 36 shall be omitted.

MINISTRY OF FINANCE (Department of Revenue) (CENTRAL BOARD OF DIRECT TAXES) NOTIFICATION New Delhi, the 1st April, 2021 (INCOME-TAX)

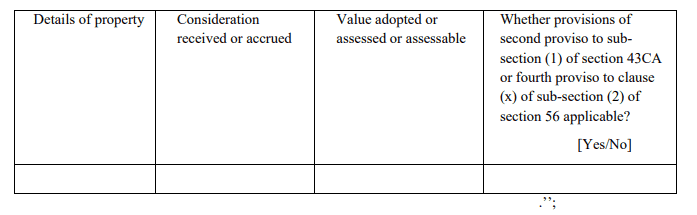

G.S.R. 246(E).––In exercise of the powers conferred by section 44AB read with section 295 of the Incometax Act (43 of 1961), the Central Board of Direct Taxes, hereby, makes the following rules further to amend the Income-tax Rules, 1962, namely:- 1. Short title and commencement.– (1) These rules may be called the Income-tax (eighth Amendment) Rules, 2021. (2) They shall come into force on the date of their publication in the Official Gazette. 2. In the Income-tax Rules, 1962,- (a) in rule 6G, after sub-rule (2), the following sub-rule shall be inserted, namely:- "(3) The report of audit furnished under this rule may be revised by the person by getting a revised report of audit from an accountant, duly signed and verified by such accountant, and furnish it before the end of the relevant assessment year for which the report pertains, if there is payment by such person after furnishing of the report under subrule (1) and (2) which necessitates a recalculation of disallowance under section 40 or section 43B." ; (b) in Appendix II, in Form 3CD,- (i) in PART –A for clause 8A, the following clause shall be substituted, namely: - "8A Whether the assessee has opted for taxation under section 115BA/115BAA/115BAB/ 115BAC/115BAD?."; (ii) in PART-B, for clause 17,the following clause shall be substituted, namely:- "17. Where any land or building or both is transferred during the previous year for a consideration less than value adopted or assessed or assessable by any authority of a State Government referred to in section 43CAor 50C,please

(iii) in clause 18, for sub-clauses (ca) and (cb), the following sub-clauses, shall be substituted namely:-

“(ca) Adjustment made to the written down value under section 115BAC/115BAD (for assessment year 2021-2022 only)……

(cb) Adjustment made to written down value of Intangible asset due to excluding value of goodwill of a business or profession…..

(cc) Adjusted written down value……….”;

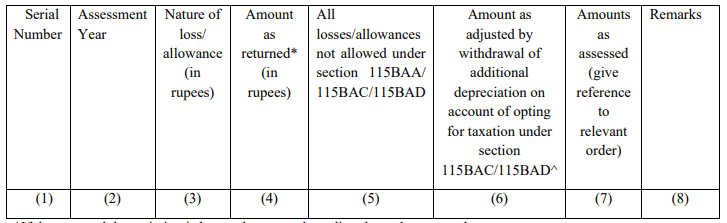

(iv) in clause 32, for sub-clause (a), the following sub-clause shall be substituted, namely:-

(a) Details of brought forward loss or depreciation allowance, in the following manner, to the extent available:

*If the assessed depreciation is less and no appeal pending then take assessed.

^To be filled in for assessment year 2021-2022 only.’’:

(v) clause 36 shall be omitted.

[Notification No. 28 /2021/F. No 370142/9/2018-TPL] ANKIT JAIN, Under Secy. (Tax Policy Legislation)

Note: The principal rules were published in the Gazette of India, Extraordinary, Part-II, Section 3, Sub-section (ii) vide notification number S.O. 969 (E), dated the 26th March, 1962 and was last amended vide notification number G.S.R. 242 (E) dated 31.03.2021About Author

Pratibha Goyal

Admin

This Account belongs to Admistrator of Studycafe.

This Account belongs to Admistrator of Studycafe.

Studycafe

Studycafe Delhi, Delhi, India

Delhi, Delhi, India 1080

1080My Recent Articles

- Chartered Accountants Association Embraces Income Tax Faceless Proceedings

- CBDT condones delay in filing form 10IC for AY 20-21: Know upto when to file the form to take concessional tax benefit

- ICAI Announced date of Live Coaching Classes for CA Intermediate Nov 2022 Exam

- ICAI Announced Registration Date for Online Home-Based Practical Training Assessment

- ICAI Released Mock Test Papers Series for May 2022 CA Exam

Up Next

Loading suggestions…

Recent Posts

All Posts

Recent Posts

All Posts