Clarification On Restriction in availment of ITC w.r.t CGST Rule 36(4) issued by CBIC

Clarification On Restriction in availment of ITC w.r.t CGST Rule 36(4) issued by CBIC Circular No. 123/42/2019- GST F. No. CBEC- 20/06/14/20

Clarification On Restriction in availment of ITC w.r.t CGST Rule 36(4) issued by CBIC

2. It is requested that suitable trade notices may be issued to publicize the contents of this Circular.

2. It is requested that suitable trade notices may be issued to publicize the contents of this Circular.

Click Here to Buy CA Final Pendrive Classes at Discounted Rate

For Regular Updates Join : https://t.me/Studycafe

Tags : GST, Rule 36(4), 20% ITC Restriction

Click Here to Buy CA Final Pendrive Classes at Discounted Rate

For Regular Updates Join : https://t.me/Studycafe

Tags : GST, Rule 36(4), 20% ITC Restriction

Circular No. 123/42/2019- GST

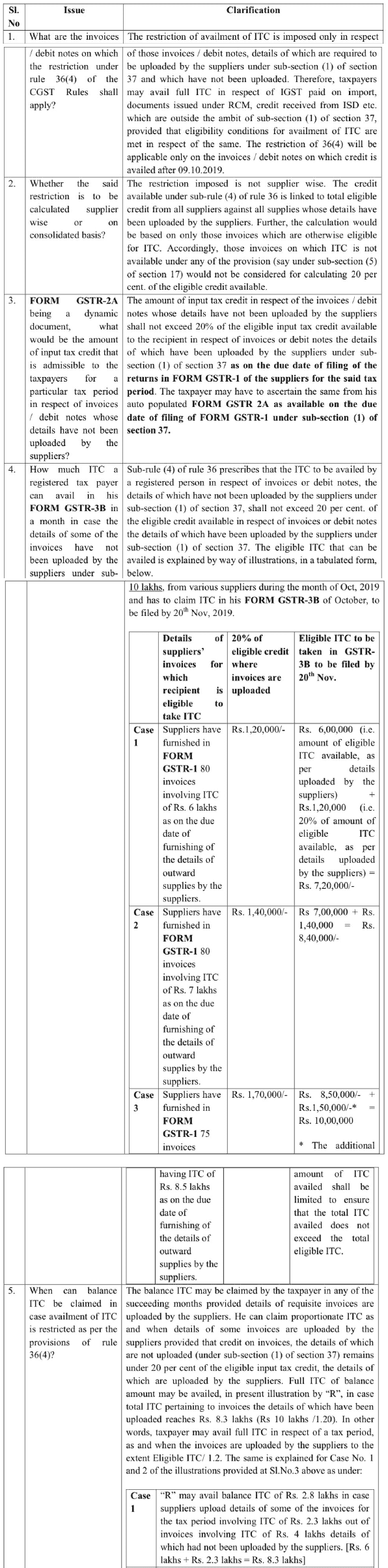

F. No. CBEC- 20/06/14/2019 - GST Government of India Ministry of Finance Department of Revenue Central Board of Indirect Taxes and Customs GST Policy Wing ****** New Delhi, the 11th November, 2019 To The Pr. Chief Commissioners / Chief Commissioners / Principal Commissioners / Commissioners of Central Tax (All), The Principal Director Generals / Director Generals (All) Madam / Sir, Subject: Restriction in availment of input tax credit in terms of sub-rule (4) of rule 36 of CGST Rules, 2017 - reg. Sub-rule (4) to rule 36 of the Central Goods and Services Tax Rules, 2017 (hereinafter referred to as the CGST Rules) has been inserted vide notification No. 49/2019- Central Tax, dated 09.10.2019. The said sub-rule provides restriction in availment of input tax credit (ITC) in respect of invoices or debit notes, the details of which have not been uploaded by the suppliers under sub-section (1) of section 37of the Central Goods and Services Tax Act, 2017 (hereinafter referred to as the CGST Act). 2. To ensure uniformity in the implementation of the provisions of the law across the field formations, the Board, in exercise of its powers conferred under section 168(1) of the CGST Act hereby clarifies various issues in succeeding paragraphs. 3. The conditions and eligibility for the ITC that may be availed by the recipient shall con tinue to be governed as per the provisions of Chapter V of the CGST Act and the rules made thereunder. This being a new provision, the restriction is not imposed through the common portal and it is the responsibility of the taxpayer that credit is availed in terms of the said rule and therefore, the availment of restricted credit in tenn s of sub-rule (4) of rule 36 of CGST Rules shall be done on self-assessment basis by the tax payers. Various issues relating to implementatio n of the said sub-rule have been examined and the clarification on each of these points is as under: -

2. It is requested that suitable trade notices may be issued to publicize the contents of this Circular.

Yogendra Garg

Principal Commissioner (GST)

About Author

Pratibha Goyal

Admin

This Account belongs to Admistrator of Studycafe.

Studycafe

Studycafe Delhi, Delhi, India

Delhi, Delhi, India 1080

1080My Recent Articles

- Chartered Accountants Association Embraces Income Tax Faceless Proceedings

- CBDT condones delay in filing form 10IC for AY 20-21: Know upto when to file the form to take concessional tax benefit

- ICAI Announced date of Live Coaching Classes for CA Intermediate Nov 2022 Exam

- ICAI Announced Registration Date for Online Home-Based Practical Training Assessment

- ICAI Released Mock Test Papers Series for May 2022 CA Exam

Up Next

Loading suggestions…

Recent Posts

All Posts

Recent Posts

All Posts