Custom NotificationNo. 57/2018-Customs (ADD) dated13th December 2018

Custom Notification No. 57/2018-Customs (ADD) dated 13th December 2018 MINISTRY OF FINANCE (Department of Revenue) NOTIFICATION New Delhi, t

Custom Notification No. 57/2018-Customs (ADD) dated 13th December 2018

MINISTRY OF FINANCE

(Department of Revenue)

NOTIFICATION

New Delhi, the 13th December, 2018

No. 57/2018-Customs (ADD)

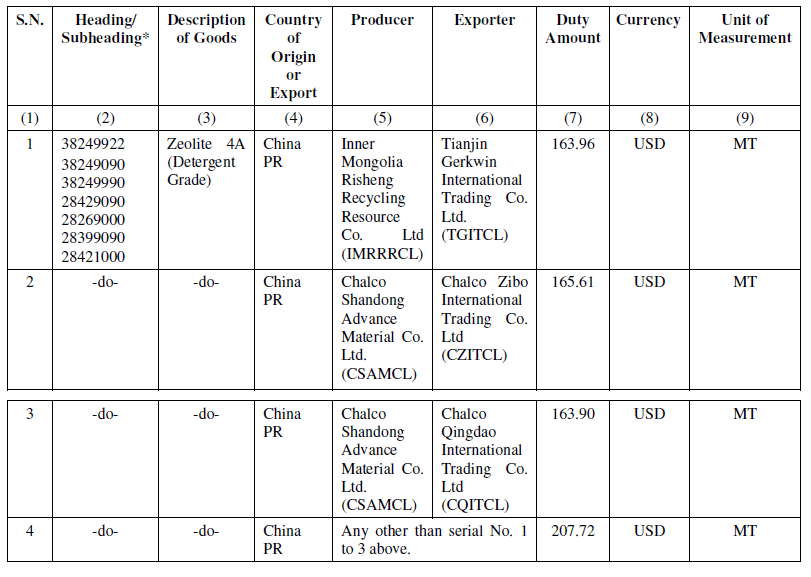

G.S.R. 1203(E).Whereas, in the matter of import of Zeolite 4A [Detergent grade] (hereinafter referred to as the subject goods) falling under the tariff items 38249922, 38249090, 38249990, 28429090, 28269000, 28399090, and 28421000 of the First Schedule to the Customs Tariff Act, 1975 (51 of 1975) (hereinafter referred to as the Customs Tariff Act), originating in, or exported from China PR (hereinafter referred to as the subject country), and imported into India, the designated authority in its final findings vide notification No. 6/14/2017-DGAD, dated the 29th October 2018, published in the Gazette of India, Extraordinary, Part I, Section 1, dated the 29th October 2018, has come to the conclusion that-

(a) there was a positive dumping margins as well as material injury to the domestic industry caused by such dumped imports;

(b) such dumping is required to offset dumping and injury; and

(c) it is necessary to impose anti-dumping duty on imports of subject goods from subject countries,

and has recommended the imposition of definitive anti-dumping duty on the imports of subject goods, originating in or exported from the subject country and imported into India, in order to remove injury to the domestic industry.

Now, therefore, in exercise of the powers conferred by sub-sections (1) and (5) of section 9A of the Customs Tariff Act, read with rules 18 and 20 of the Customs Tariff (Identification, Assessment and Collection of Anti-dumping Duty on Dumped Articles and for Determination of Injury) Rules, 1995, the Central Government, after considering the aforesaid final findings of the designated authority, hereby imposes on the subject goods, the description of which is specified in column (3) of the Table below, falling under tariff item of the First Schedule to the Customs Tariff Act as specified in the corresponding entry in column (2), originating in and exported from the countries as specified in the corresponding entry in column (4), produced by the producers as specified in the corresponding entry in column (5), exported by the exporters as specified in the corresponding entry in column (6), and imported into India, an anti-dumping duty at the rate equal to the amount as specified in the corresponding entry in column (7), in the currency specified in the corresponding entry in column (8) and per unit of measurement as specified in the corresponding entry in column (9) of the said Table:

2. The anti-dumping duty imposed shall be effective for a period of five years (unless revoked, superseded or amended earlier) from the date of publication of this notification in the Official Gazette and shall be payable in Indian currency.

Explanation.- For the purposes of this notification, rate of exchange applicable for the purposes of calculation of such anti-dumping duty shall be the rate which is specified in the notification of the Government of India, in the Ministry of Finance (Department of Revenue), issued from time to time, in exercise of the powers conferred by section 14 of the Customs Act, 1962 (52 of 1962), and the relevant date for the determination of the rate of exchange shall be the date of presentation of the bill of entry under section 46 of the said Act.

2. The anti-dumping duty imposed shall be effective for a period of five years (unless revoked, superseded or amended earlier) from the date of publication of this notification in the Official Gazette and shall be payable in Indian currency.

Explanation.- For the purposes of this notification, rate of exchange applicable for the purposes of calculation of such anti-dumping duty shall be the rate which is specified in the notification of the Government of India, in the Ministry of Finance (Department of Revenue), issued from time to time, in exercise of the powers conferred by section 14 of the Customs Act, 1962 (52 of 1962), and the relevant date for the determination of the rate of exchange shall be the date of presentation of the bill of entry under section 46 of the said Act.

2. The anti-dumping duty imposed shall be effective for a period of five years (unless revoked, superseded or amended earlier) from the date of publication of this notification in the Official Gazette and shall be payable in Indian currency.

Explanation.- For the purposes of this notification, rate of exchange applicable for the purposes of calculation of such anti-dumping duty shall be the rate which is specified in the notification of the Government of India, in the Ministry of Finance (Department of Revenue), issued from time to time, in exercise of the powers conferred by section 14 of the Customs Act, 1962 (52 of 1962), and the relevant date for the determination of the rate of exchange shall be the date of presentation of the bill of entry under section 46 of the said Act.

[F. No. 354/409/2018 -TRU]

GUNJAN KUMAR VERMA, Under Secy.

Click Here to Buy CA Final Pendrive Classes at Discounted RateAbout Author

CA Deepak Gupta

Co Founder

CA Deepak Gupta,is Co-founder of Studycafe. He is Microsoft Office Specialist and Corporate Trainer of AI Tools, Microsoft Excel.

He is Finance Influencer having more than 250K followers on Social Media. CA Deepak Gupta, is Having more than 14 plus years of experience, and he has Worked with best brands Like, Hero, Wipro, Ericsson before Starting Studycafe. He has Trained more than 20000 Persons in Microsoft Excel, PowerPoint, Power BI, Google Sheet, Google Forms and Other Tools.

CA Deepak Gupta,is Co-founder of Studycafe. He is Microsoft Office Specialist and Corporate Trainer of AI Tools, Microsoft Excel.

He is Finance Influencer having more than 250K followers on Social Media. CA Deepak Gupta, is Having more than 14 plus years of experience, and he has Worked with best brands Like, Hero, Wipro, Ericsson before Starting Studycafe. He has Trained more than 20000 Persons in Microsoft Excel, PowerPoint, Power BI, Google Sheet, Google Forms and Other Tools.

StudyCafe

StudyCafe Delhi, Delhi, India

Delhi, Delhi, India 3423

3423My Recent Articles

- UltraTech Cement slapped with Rs. 808.78 Cr Income Tax Demand

- GST: High Court upheld constitutional validity of Section 16(2)(c), asks government to address ITC issues of genuine purchasers

- Old vs New Tax Regime for Tax Year 2026-27

- High court criticizes Income Tax Department for not releasing ITR Utilities despite 11 years of directions

- Fino Payments Bank CEO Rishi Gupta Gets Bail in GST Case, Bank Clarifies No Direct Link

Up Next

Loading suggestions…

Recent Posts

All Posts

Tags

No tags yet.

Recent Posts

All Posts

Tags

No tags yet.