Difference between form 3CA & 3CB - Income Tax Audit Form

Difference between form 3CA & 3CB - Income Tax Audit Form Relevant Rule : Rule 6G of Income Tax Act : Report of audit of accounts to be furnished…

Table of Contents

Difference between form 3CA & 3CB - Income Tax Audit Form

Relevant Rule : Rule 6G of Income Tax Act:

Report of audit of accounts to be furnished under section 44AB.

6G. (1) The report of audit of the accounts of a person required to be furnished under section 44AB shall,

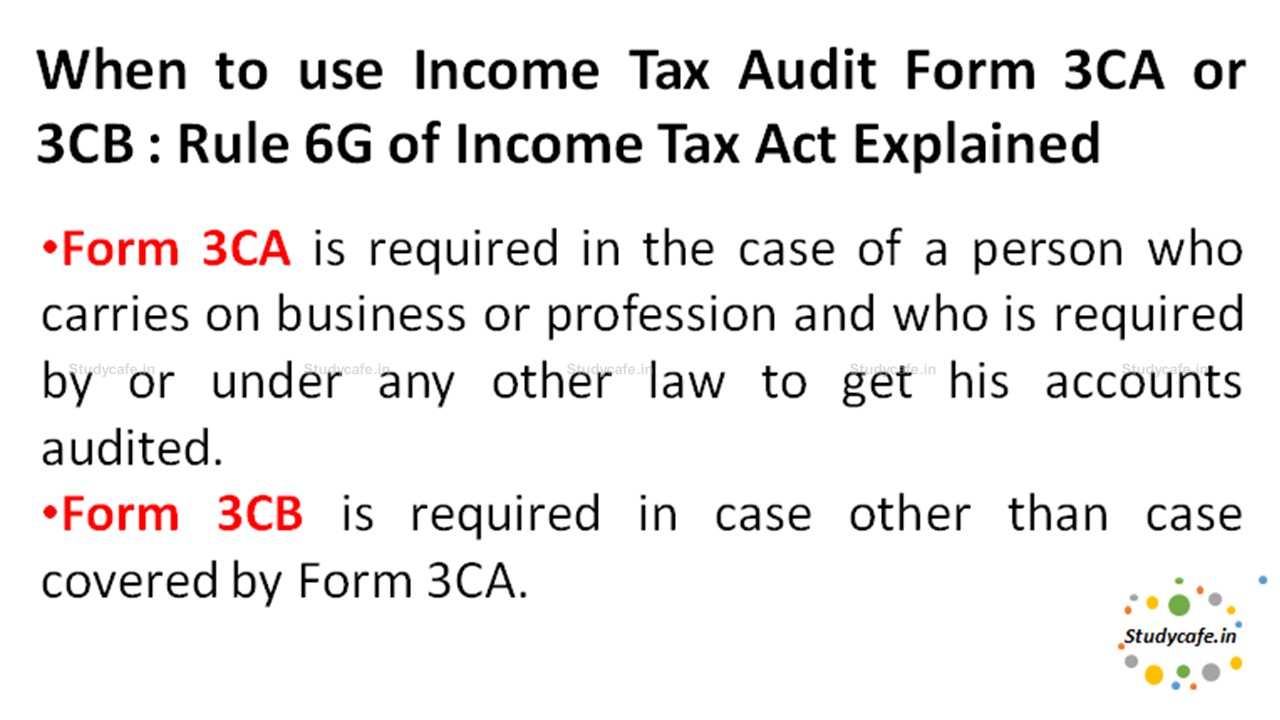

(a) in the case of a person who carries on business or profession and who is required by or under any other law to get his accounts audited, be in Form No. 3CA;

(b) in the case of a person who carries on business or profession, but not being a person referred to in clause (a), be in Form No. 3CB.

(2) The particulars which are required to be furnished under section 44AB shall be in Form No. 3CD.

Now when to use Income Tax Audit Form 3CA or 3CB : Rule 6G of Income Tax Act Explained

Form 3CA is required in the case of a person who carries on business or profession and who is required by or under any other law to get his accounts audited. CASE A : For Example a company is required to get it's account audited under Company Act 2013 and therefore in case we have to do Tax Audit for the company, we shall file Income Tax Audit Form 3CA. Form 3CB is required in case other than case covered by Form 3CA. CASE B : For Example Turnover of an individual is INR 5 Crs. Now he is not required to get his accounts Audited under any other act, but we have to do his audit as per Income Tax Act, therefore in this case Income Tax Audit Form 3CB shall be filed. These two forms as the case may be are required to be filed along with Form 3CD which is again a detailed form having 44 clauses analyzing and auditing the accounts of taxpayer as per Income Tax Act. Therefore now we know that in CASE A one shall file Tax Audit Report in Form 3CA-3CD and in CASE B one shall file Tax Audit Report in Form 3CB-3CDDue Date of Filing Tax Audit for FY 20-21

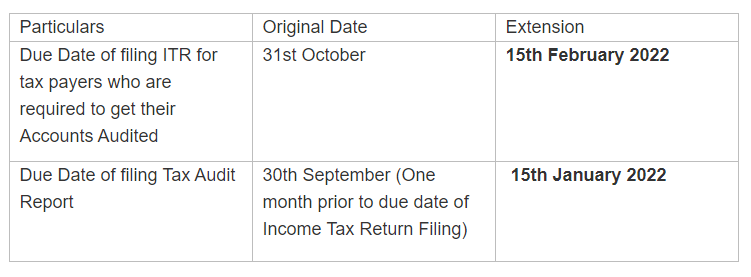

Change in Due Date of Tax Audit and Income Tax Return Filing:

Penalty for Non Filing Tax Audit Report

A minimum penalty can be 0.5% of the total sales, turnover or gross receipts, which can go up to Rs. 1,50,000 is applicable in case Tax Audit Report is not filed. However, if the taxpayer gives reasonable cause for non-compliance, no penalty will be imposed.About Author

Reetu

Content Manager

Reetu is a Content Writer with 4+ years of experience in GST, Income Tax, Finance, Company Law, Education and Career Related Content. She is a B.COM (Honrs.) Graduate.

Reetu is a Content Writer with 4+ years of experience in GST, Income Tax, Finance, Company Law, Education and Career Related Content. She is a B.COM (Honrs.) Graduate.

Studycafe

Studycafe Delhi, Delhi, India

Delhi, Delhi, India 8072

8072My Recent Articles

- Income Tax Guide for Indian Defence Personnel for Tax Filing, Taxable Allowances and Other Benefits

- Income Tax Return Breaking: ITR Forms released for AY 25-26

- Ex-DRT Officials Sentenced to 5 Years Rigorous Imprisonment by Madras High Court along with Rs.27 Lakh Fine

- GSTN issued Advisory on Case Sensitivity in IRN Generation

- RBI to issue Notes of Rs.10 and Rs.500 bearing Signature of Guv Malhotra

Up Next

Loading suggestions…

Recent Posts

All Posts

Tags

Recent Posts

All Posts