Due Date for Availing ITC As Per Section 16(4) Applicable on IGST Paid on Bill of Entry: AAR:

IGST credit paid on imported machinery via Bill of Entry was not claimed in time, and AAR ruled it cannot be availed after the Section 16(4) deadline.

AAR Rules IGST Credit on Imports Time-Barred If Not Claimed by Due Date

Table of Contents

Due Date for Availing ITC As Per Section 16(4) Applicable on IGST Paid on Bill of Entry: AAR

M/s. Adi Enterprises is the legal name of the applicant here. The registered address of the business is 01, Desaiwadi, Usgaon, Bhatane, Virar, Palghar, Maharashtra, 401303. Applicant is a manufacturer of "Ear buds", which have HSN as 96190090. They have imported machinery, the details of which are as under:

- Commercial Invoice Date: 18/08/2022

- Invoice Value: USD 49000

- Seller name: China Forbona Group Limited

- Invoice Number: P220621518YD

- Port Code: INBOM4

- BE No: 2134376

- BE Date: 24/08/2022

- IGST Paid: Rs. 9,00,939

What is Case?

The applicant imported goods and paid IGST (tax) via a Bill of Entry. This tax was accurately displayed in their GSTR 2A (in August 2022) and GSTR 2B (in March 2023), which are forms indicating what Input Tax Credit (ITC) is available. Even though the tax was displayed as available, the applicant forgot to claim this ITC in its GSTR 3B return for the financial year 2022–23. Moreover, the applicant missed the final due date (30th November 2023) to claim ITC as per the GST law. The GST department then sent an email to the applicant on March 21, 2024, saying that this IGST credit is displayed in GSTR 2B but has not been claimed yet in GSTR 3B. The department recommended the applicant claim it now and also reverse it in the same return (a process for unmatched ITC). The applicant has now remembered its missed ITC and is now asking the Authority for Advance Ruling, and raising questions whether it’s still legally allowed to claim this old IGST credit in the upcoming GSTR 3B return, even though the deadline has ended under Section 16(4) of the CGST Act.Questions Raised by Applicant

The applicant has raised the following questions by seeking the advisory ruling: "1) Whether the time limit of availing ITC as mentioned in Section 16(4) of the CGST Act, 2017 is applicable on ITC eligible as per the Bill of Entry? 2) In this case, can the applicant avail of this IGST paid as per the bill of entry in the next GSTR3B?"What Did Ruling Say?

In accordance with the Maharashtra Authority for Advance Ruling (MAAR), the above questions are being answered as follows under Section 98 of the Central Goods and Services Tax Act, 2017 and the Maharashtra Goods and Services Tax Act, 2017: Ans. 1: Yes, the time limit of availing ITC (Income Tax Credit) as stated in Section 16(4) of the CGST Act, 2017 is applicable on ITC eligible as per the Bill of Entry. Ans. 2: No, in this case, the applicant cannot avail of this ICST paid as a bill of entry in the next CGSTR3B. Refer to the advance ruling for complete information.About Author

Saloni Kumari

Content Writer

Saloni is a Content Writer with 2+ years of experience at studycafe.in. She writes legal, taxation, and finance related content including GST, Income Tax etc. Skilled in translating complex judicial pronouncements and regulatory developments into clear, and reader-friendly articles. Experienced in covering judgements of ITAT, High Court, GSTAT, and news related to Income Tax, GST, and corporate law. She can be reached at [email protected].

Saloni is a Content Writer with 2+ years of experience at studycafe.in. She writes legal, taxation, and finance related content including GST, Income Tax etc. Skilled in translating complex judicial pronouncements and regulatory developments into clear, and reader-friendly articles. Experienced in covering judgements of ITAT, High Court, GSTAT, and news related to Income Tax, GST, and corporate law. She can be reached at [email protected].

StudyCafe

StudyCafe Delhi, Delhi, India

Delhi, Delhi, India 2427

2427My Recent Articles

- Reliance Infrastructure Receives ED Provisional Attachment Order Over Rs 762.75 Crore Reliance Power Shareholding

- CBIC Allows Extension Beyond Two-Year Re-Export Limit for Duty-Free Event Imports

- Enforcement Directorate Attaches Reliance Power Assets Worth Rs 1,021 Crore Under PMLA

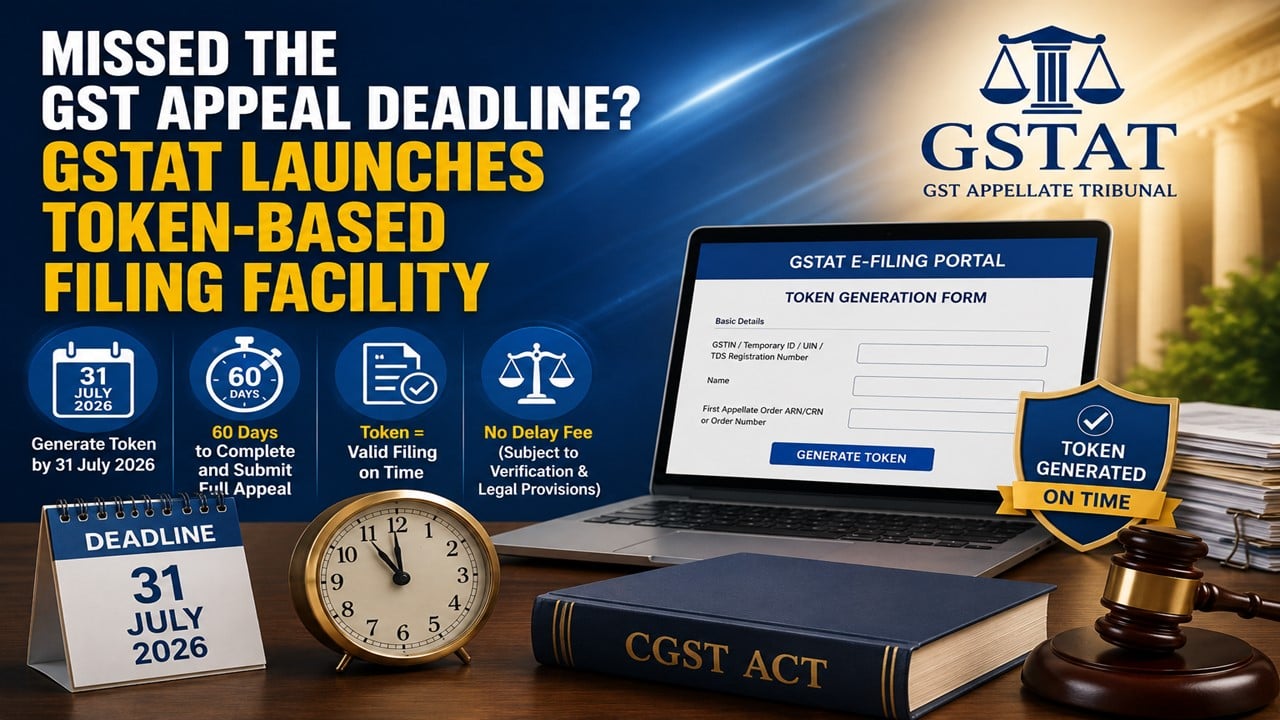

- GSTAT Introduces Token-Based Mechanism to Secure Timely GST Appeal Filing Before July 31, 2026Premium

- Assam GST Department Prescribes Indicative ITC Utilisation Benchmarks for Government Works ContractorsPremium

Up Next

Loading suggestions…

Recent Posts

All Posts

Recent Posts

All Posts