GST Council on Recovery of Tax, ITC and Interest in case of mismatch in GSTR-3B, GSTR-2B and GSTR-1:

GST Council in its 50th meeting has provided for a recovery process for interest and tax in case of Difference in Form GSTR-1 and GSTR-3B.

ITC and Interest in case of mismatch in GSTR-3B, GSTR-2B and GSTR-1

Table of Contents

GST Council on Recovery of Tax, ITC and Interest in case of mismatch in GSTR-3B, GSTR-2B and GSTR-1

The GST Council in its 50th meeting has provided for a recovery process for interest and tax in case of Difference in Form GSTR-1 and GSTR-3B. The Council has also provided for a process to deal with Difference in ITC availed in GSTR-3B and Autopopulated in GSTR-2B.

Recovery Process in case of Difference in Form GSTR-1 and GSTR-3B

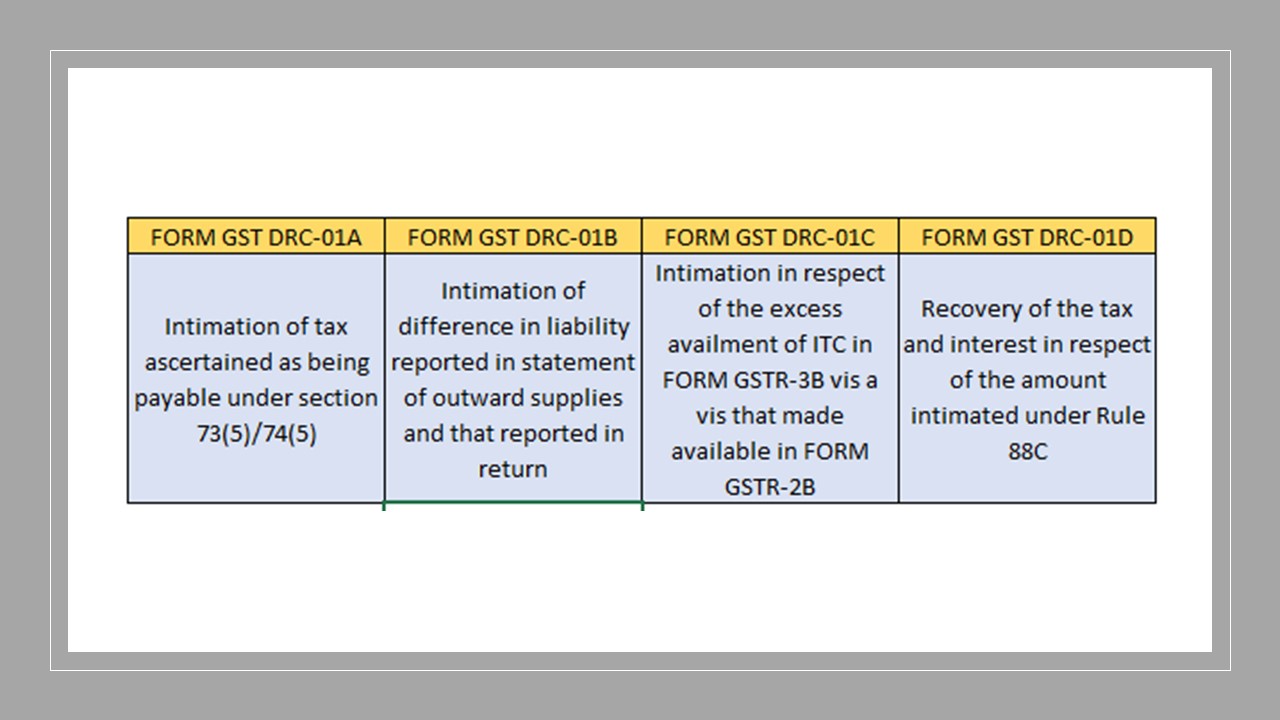

Rule 88C was inserted in the CGST Rules, 2017 with effect from 26.12.2022 for system based intimation to the registered person in cases where the output tax liability in terms of FORM GSTR-1 of a registered person for any particular month exceeds the output tax liability disclosed by the said person in the return in FORM GSTR-3B for the said month by a specified threshold. This was done on the recommendations of the GST Council in its 48th meeting held on 17.12.2022. As per Rule 88C, the person who recives intimation under rule 88C shall pay the amount of the differential tax liability, as specified in Part A of FORM GST DRC-01B, fully or partially, along with interest under section 50, through FORM GST DRC-03 and furnish the details thereof in Part B of FORM GST DRC-01B electronically on the common portal; or furnish a reply electronically on the common portal, incorporating reasons in respect of that part of the differential tax liability that has remained unpaid, if any, in Part B of FORM GST DRC-01B. The Council has now recommended the insertion of Rule 142B in the CGST Rules, 2017, and the insertion of a FORM GST DRC-01D to provide for the manner of recovery of the tax and interest in respect of the amount intimated under Rule 88C which has not been paid and for which no satisfactory explanation has been furnished by the registered person.Differences in ITC availed in Form GSTR-3B and GSTR-2B

The Council has recommended a mechanism for system-based intimation to the taxpayers in respect of the excess availment of ITC in FORM GSTR-3B vis a vis that made available in FORM GSTR-2B. This means System driven notices will be sent in case of Differences in ITC availed in Form GSTR-3B and GSTR-2B. The threshold, along with the procedure of auto-compliance on the part of the taxpayers, to explain the reasons for the said difference or take remedial action in respect of such difference will be notified soon. For this purpose, rule 88D and FORM DRC-01C to be inserted in CGST Rules, 2017, along with an amendment in rule 59(6) of CGST Rules, 2017.About Author

CA Pratibha Goyal

Co Founder

CA Pratibha Goyal is Chartered Accountant qualified in 2016, is a Member of The Institute of Chartered Accountants of India having wide experience in the field of Auditing, Taxation, ROC, GST and Secretarial matters etc.

She has written over a thousand articles & has made several videos on topics related to Auditing & Taxation. As a Speaker she has delivered various sessions on various branches of NIRC of ICAI.

CA Pratibha Goyal is Chartered Accountant qualified in 2016, is a Member of The Institute of Chartered Accountants of India having wide experience in the field of Auditing, Taxation, ROC, GST and Secretarial matters etc.

She has written over a thousand articles & has made several videos on topics related to Auditing & Taxation. As a Speaker she has delivered various sessions on various branches of NIRC of ICAI.

Studycafe

Studycafe New Delhi, Delhi, India

New Delhi, Delhi, India 1486

1486My Recent Articles

- Biggest Labour Reform in Indian History: 4 Labour Codes Effective from today

- Tax Audit and ITR Due date not extended in this case: Know More

- Government notifies Agreement and Protocol between India and Qatar [Read Notification]

- CA Breaking: Results of ICAI Examination to be announced soon, Know probable Date

- Breaking: GSTR-3B Due Date for September 2025 extended by CBIC amid Diwali Festivities

Up Next

Loading suggestions…

Recent Posts

All Posts

Recent Posts

All Posts