GST Interest Calculator to be introduced in GSTR-3B

GST Interest Calculator to be introduced in GSTR-3B A new interest calculator functionality is being released in GSTR-3B as a convenience measure for…

Table of Contents

GST Interest Calculator to be introduced in GSTR-3B

A new interest calculator functionality is being released in GSTR-3B as a convenience measure for taxpayers and to assist taxpayers in performing correct self-assessment. This functionality will compute interest for the system based on the tax liability values declared by the taxpayers. The interest payable, if any, on the tax liability declared in the GSTR-3B for a specific tax period will be computed after the GSTR-3B is filed. These interest values computed by the system will be auto-populated in Table-5.1 of the GSTR-3B for the next tax period. The facility would be similar to the collection of late fees for GSTR-3Bs filed after the Due date and posted in the GSTR-3B for the following period.

This functionality has a user-friendly interface that informs taxpayers about how the system computes interest values for each tax-head. This functionality also assists taxpayers in correctly calculating interest for any past period liability declared in the GSTR-3B for the current tax period, based on the information provided by them on the portal.

The interest computed by the system has been aligned with the Section-50 of the CGST Act, 2017, as amended. Consequently, interest liability for respect of supplies made during the present tax-period and declared in the GSTR-3B for this period will be calculated only on that portion of the tax which is paid by debiting the electronic cash ledger, i.e., tax paid in cash. With respect to the liability pertaining to the previous tax-period(s), and paid in later GSTR-3B, the interest will be computed for the entire liability, whether paid by debiting the electronic cash ledger or electronic credit ledger.

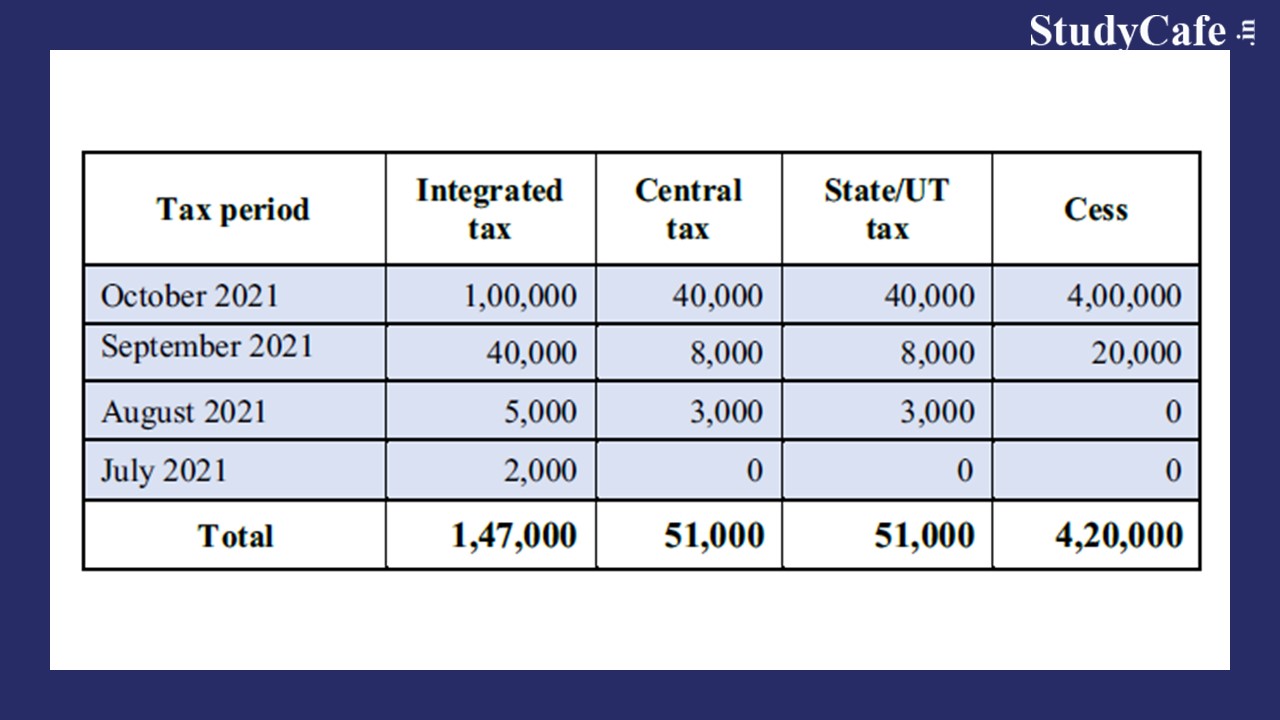

However, these consolidated tax liability values consist of not only for October 2021 but also for previous tax-periods of July, August & September 2021.

Hence, for the purposes of proper interest calculation, the taxpayer would be expected to declare the following tax-period wise break-up in GSTR-3B for October 2021, in the following manner:

However, these consolidated tax liability values consist of not only for October 2021 but also for previous tax-periods of July, August & September 2021.

Hence, for the purposes of proper interest calculation, the taxpayer would be expected to declare the following tax-period wise break-up in GSTR-3B for October 2021, in the following manner:

The interest calculation could be thereafter done as per the aforesaid values declared by the taxpayer, easily by the system. However, this gap exists in the current GSTR-3B implementation, to cover which new feature has been added.

The interest calculation could be thereafter done as per the aforesaid values declared by the taxpayer, easily by the system. However, this gap exists in the current GSTR-3B implementation, to cover which new feature has been added.

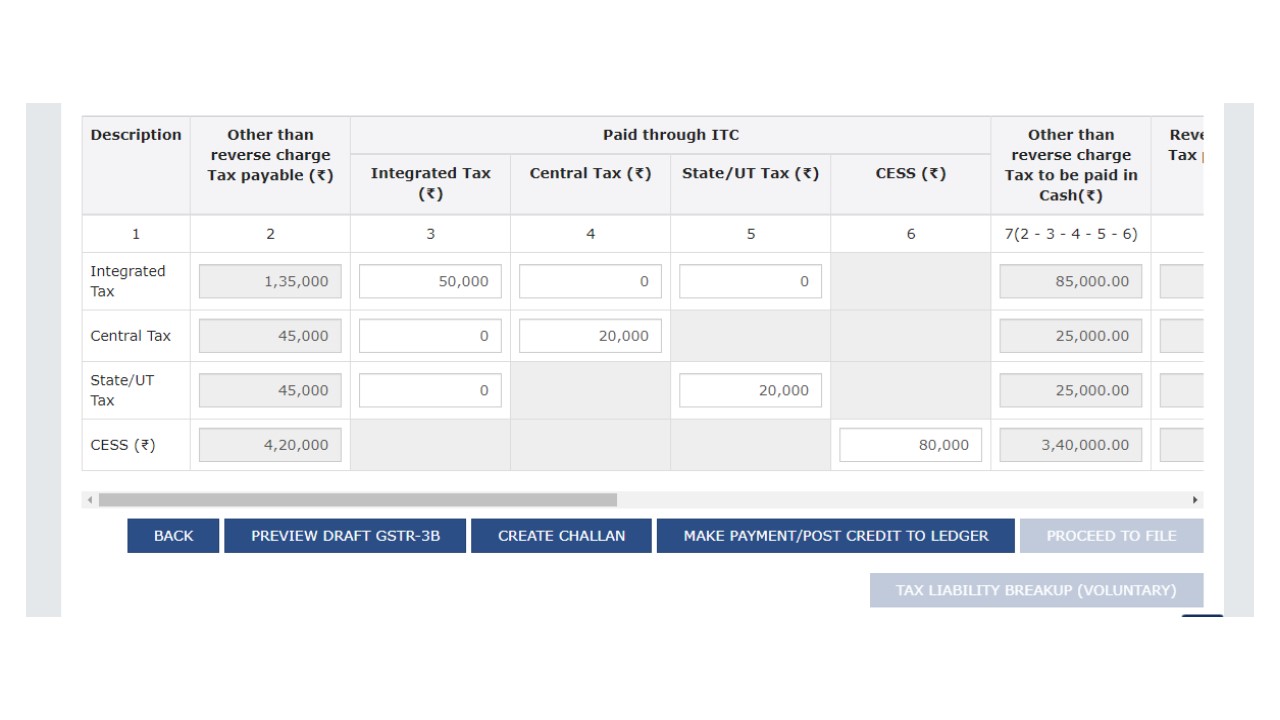

The Tax Liability Break-up (Voluntary) button will be enabled only after clicking the ‘Make payment/Post credit to ledger’ button. In other words, break-up of the taxperiod wise values can be furnished by the taxpayers after making payment of the liability for this period.

The Tax Liability Break-up (Voluntary) button will be enabled only after clicking the ‘Make payment/Post credit to ledger’ button. In other words, break-up of the taxperiod wise values can be furnished by the taxpayers after making payment of the liability for this period.

This button will also appear on the filing page of GSTR-3B.

Click on link given below to read further.

This button will also appear on the filing page of GSTR-3B.

Click on link given below to read further.

Auto-population of system computed interest

This new functionality will compute the minimum interest applicable on the basis of the values declared by the taxpayers in GSTR-3B for a particular tax-period. This system computed interest will be auto-populated in Table-5.1 of GSTR-3B for the next tax-period, the way it is done for the Late fees at present. The system computed interest values auto-populated in next GSTR-3B return will be kept editable, initially. However, the system generated PDF of filed GSTR-3B will contain both values: the System computed interest, and the user paid interest values.Scenarios where interest is applicable

Interest liability can arise in cases of either of the following, or both: i. Delayed filing of return: If the present GSTR-3B is filed after the ‘due date’, then interest will be applicable at prescribed rate of interest from the ‘due date’ of GSTR-3B for relevant period i.e. till the date of filing of the return. ii. Delayed declaration of liability: If the liability pertaining to previous tax-periods is discharged in the present GSTR-3B, then interest will be leviable from the ‘due date’ of return for the said previous period till the date of declaration of the liability in the return. Thus, as part of the interest calculator, a new feature has been provided to GSTR-3B for allowing taxpayers to voluntarily declare Tax-period wise break-up of liability. If a taxpayer is discharging liability for any past period(s) in the present GSTR- 3B, then exact tax-period wise break-up of the same can be provided by the taxpayers. The interest will be thereafter computed by the system accordingly.Furnishing tax-period wise break-up in GSTR-3B:

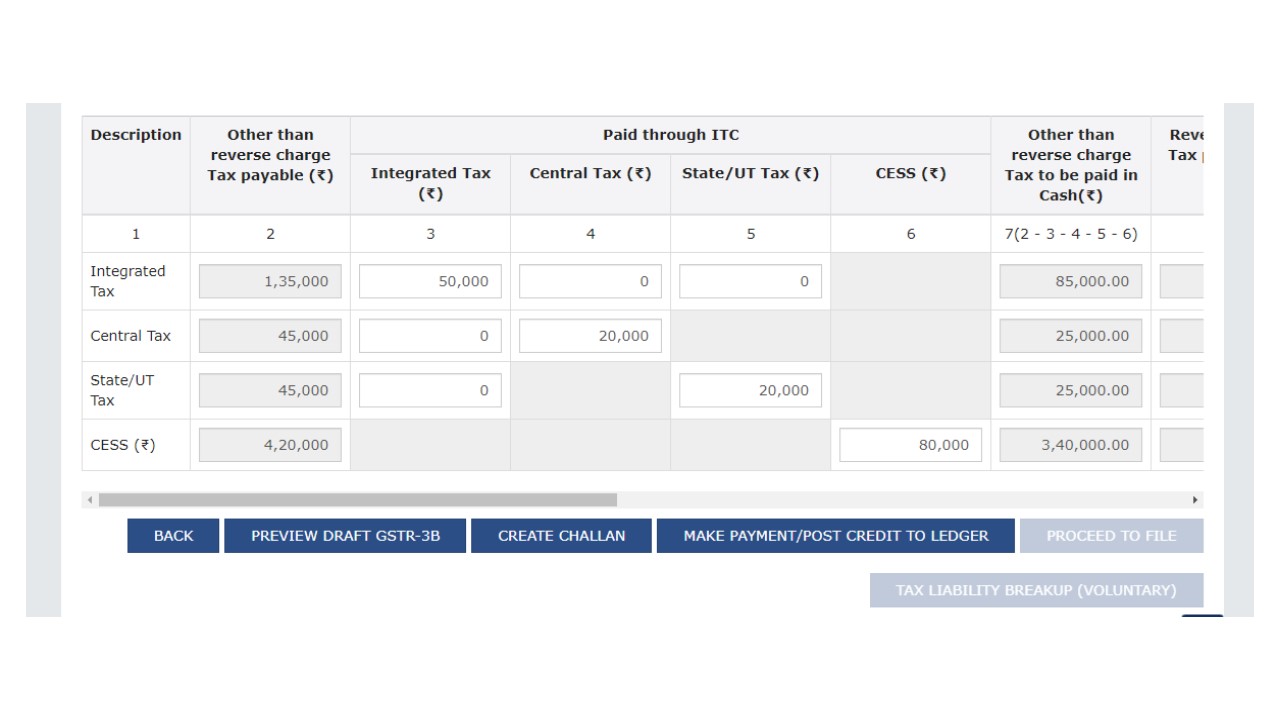

The return in FORM GSTR-3B, as it is now, allows taxpayers to discharge tax liability for previous tax-periods also, in addition to the tax liability for the present period. However, the tax-period wise break-up of the tax liability is not available in GSTR-3B. Thus, for computing the exact interest liability, the information regarding the tax-period wise break-up of the consolidated tax liability declared by the taxpayer would be required by the system. In view of above, a new button has been added in GSTR-3B, called Tax Liability Break- up (Voluntary), and data is to be entered by clicking this button only by those taxpayers who are making payment for liability pertaining to earlier tax-periods in the present GSTR- 3B. In cases where the present GSTR-3B consists of liability only for the present period, the taxpayers can ignore this button, and continue filing their return as usual.Changes in user experience

Taxpayers filing on or before Due date of GSTR-3B: After the interest calculator is enabled on the GST Portal, there will be no change in the user experience for the taxpayers who file their return on or before the ‘due date’. The taxpayer would still have the facility to provide the break-up of liability of the past period(s). For details of declaring tax-period wise tax liability, please refer to the Annexure. Taxpayer filing GSTR-3B after Due date: For taxpayers who are filing after ‘due date’, a pop-up will be shown regarding the option to declare tax-period wise tax liability, if applicable to them. If they have any tax liability pertaining to any previous tax-period to declare, they may declare the same. If the entire liability pertains to the present period, then they may ignore this pop-up message, and continue their filing as usual. If no previous period tax liability is declared, by default the interest will be computed by assuming that the entire tax liability pertains to the present period. This facilitation measure is expected to assist the taxpayers by helping them with calculation of correct interest while filing of GSTR-3B and will thus improve ease in filing return under GST. This functionality will be made available on the GST Portal shortly, and the same will be intimated to the taxpayers.Illustration

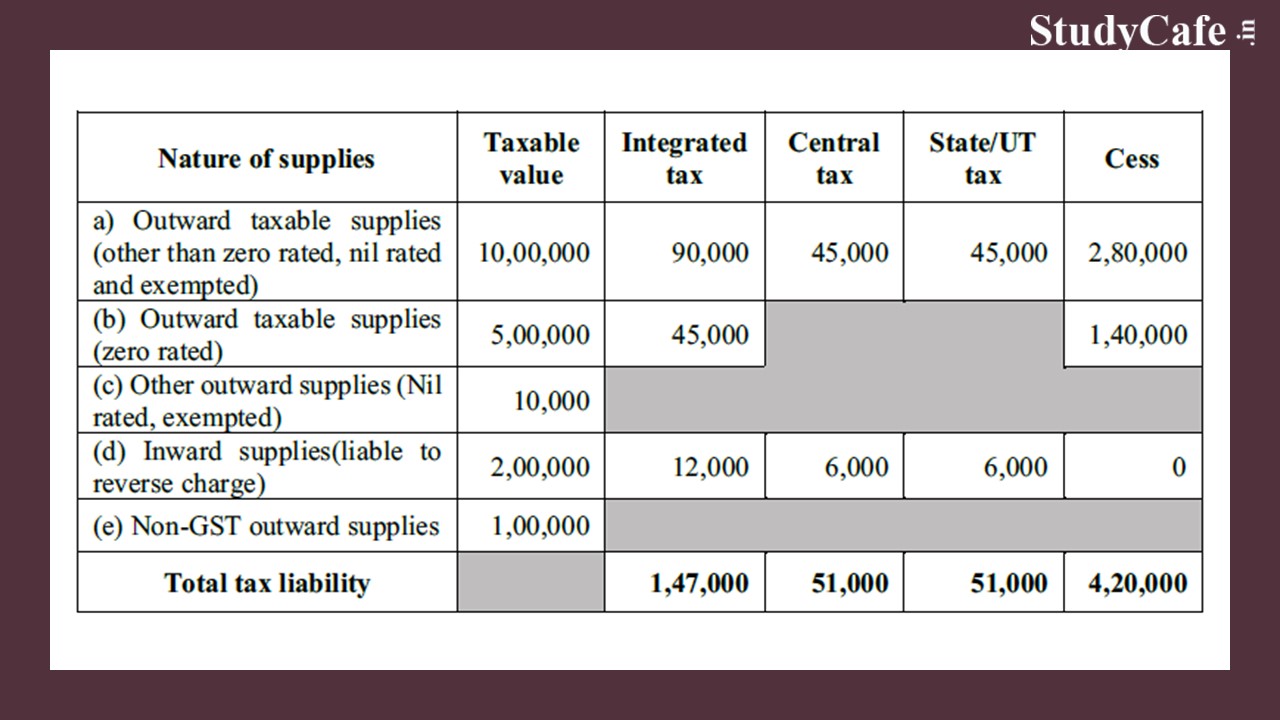

A monthly taxpayer is filing GSTR-3B for the tax period of October 2021. In the said GSTR-3B, the taxpayer has declared the following values in Table-3.1 of GSTR-3B:

However, these consolidated tax liability values consist of not only for October 2021 but also for previous tax-periods of July, August & September 2021.

Hence, for the purposes of proper interest calculation, the taxpayer would be expected to declare the following tax-period wise break-up in GSTR-3B for October 2021, in the following manner:

The interest calculation could be thereafter done as per the aforesaid values declared by the taxpayer, easily by the system. However, this gap exists in the current GSTR-3B implementation, to cover which new feature has been added.

New feature in GSTR-3B

Tax Liability Break-up (Voluntary) button in GSTR-3B: A new button called Tax Liability Break-up (Voluntary) will be provided in GSTR-3B for furnishing the tax-period wise break-up of tax liability. This button will appear in GSTR-3B on the payment page, below the Table 6.1 – Payment of tax.

The Tax Liability Break-up (Voluntary) button will be enabled only after clicking the ‘Make payment/Post credit to ledger’ button. In other words, break-up of the taxperiod wise values can be furnished by the taxpayers after making payment of the liability for this period.

This button will also appear on the filing page of GSTR-3B.

Click on link given below to read further.About Author

CA Deepak Gupta

Co Founder

CA Deepak Gupta,is Co-founder of Studycafe. He is Microsoft Office Specialist and Corporate Trainer of AI Tools, Microsoft Excel.

He is Finance Influencer having more than 250K followers on Social Media. CA Deepak Gupta, is Having more than 14 plus years of experience, and he has Worked with best brands Like, Hero, Wipro, Ericsson before Starting Studycafe. He has Trained more than 20000 Persons in Microsoft Excel, PowerPoint, Power BI, Google Sheet, Google Forms and Other Tools.

CA Deepak Gupta,is Co-founder of Studycafe. He is Microsoft Office Specialist and Corporate Trainer of AI Tools, Microsoft Excel.

He is Finance Influencer having more than 250K followers on Social Media. CA Deepak Gupta, is Having more than 14 plus years of experience, and he has Worked with best brands Like, Hero, Wipro, Ericsson before Starting Studycafe. He has Trained more than 20000 Persons in Microsoft Excel, PowerPoint, Power BI, Google Sheet, Google Forms and Other Tools.

StudyCafe

StudyCafe Delhi, Delhi, India

Delhi, Delhi, India 3423

3423My Recent Articles

- UltraTech Cement slapped with Rs. 808.78 Cr Income Tax Demand

- GST: High Court upheld constitutional validity of Section 16(2)(c), asks government to address ITC issues of genuine purchasers

- Old vs New Tax Regime for Tax Year 2026-27

- High court criticizes Income Tax Department for not releasing ITR Utilities despite 11 years of directions

- Fino Payments Bank CEO Rishi Gupta Gets Bail in GST Case, Bank Clarifies No Direct Link

Up Next

Loading suggestions…

Recent Posts

All Posts

Recent Posts

All Posts