GST Notices issued for first claim and then reversal of IGST on ineligible ITC [Know More]:

![GST Notices issued for first claim and then reversal of IGST on ineligible ITC [Know More]](https://assets.studycafe.in/uploads/2024/02/GST-Notices-issued-for-first-claim-and-then-reversal-of-IGST-on-ineligible-ITC.jpg)

The GST Department has now started issuing Notices so as to first claim IGST ITC and then reverse IGST on ineligible ITC as per instructions given in CBIC Circular No. 170/02/2022-GST.

GST Notices issued for ITC Claim

GST Notices issued for first claim and then reversal of IGST on ineligible ITC [Know More]

The GST Department has now started issuing Notices so as to first claim IGST ITC and then reverse IGST on ineligible ITC as per instructions given in CBIC Circular No. 170/02/2022-GST.

The Text of the Notice is as follows:

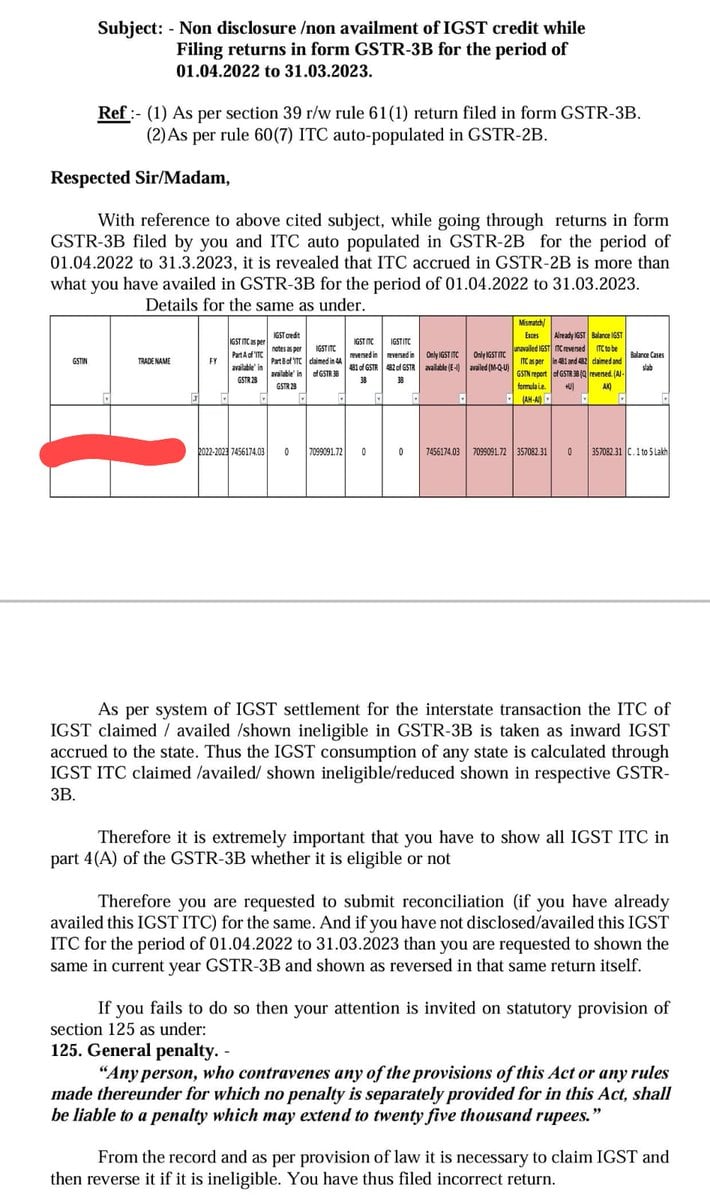

Sub: Non-disclosure/non-availment of IGST credit while Filing returns in form GSTR-3B for the period of 01.04.2022 to 31.03.2023.

With reference to above cited subject, while going through returns in form GSTR-3B filed by you and ITC auto-populated in GSTR-2B for the period of 01.04.2022 to 31.3.2023, it is revealed that ITC accrued in GSTR-2B is more than what you have availed in GSTR-3B for the period of 01.04.2022 to 31.03.2023.

According to the IGST settlement mechanism for interstate transactions, the ITC of IGST claimed, availed, or shown ineligible in GSTR-3B is treated as inward IGST accrued to the state. Thus, the IGST consumption of each state is determined using the IGST ITC claimed/availed/shown ineligible/reduced in the relevant GSTR-3B.

Therefore it is extremely important that you have to show all IGST ITC in part 4 (A) of the GSTR-3B whether it is eligible or not.

As a result, if you have already claimed this IGST ITC, you must submit a reconciliation. And if you have not disclosed/acquired this IGST ITC for the period of 01.04.2022 to 31.03.2023, you are required to show the same in the current year GSTR-3B and reversed in that same return.

If you fails to do so then your attention is invited on statutory provision of section 125 as under:

125. General penalty.

"Any person, who contravenes any of the provisions of this Act or any rules made thereunder for which no penalty is separately provided for in this Act, shall be liable to a penalty which may extend to twenty five thousand rupees."

From the record and as per provision of law it is necessary to claim IGST and then reverse it if it is ineligible. You have thus filed an incorrect return.

About Author

Reetu

Content Manager

Reetu is a Content Writer with 4+ years of experience in GST, Income Tax, Finance, Company Law, Education and Career Related Content. She is a B.COM (Honrs.) Graduate.

Studycafe

Studycafe Delhi, Delhi, India

Delhi, Delhi, India 8072

8072My Recent Articles

- Income Tax Guide for Indian Defence Personnel for Tax Filing, Taxable Allowances and Other Benefits

- Income Tax Return Breaking: ITR Forms released for AY 25-26

- Ex-DRT Officials Sentenced to 5 Years Rigorous Imprisonment by Madras High Court along with Rs.27 Lakh Fine

- GSTN issued Advisory on Case Sensitivity in IRN Generation

- RBI to issue Notes of Rs.10 and Rs.500 bearing Signature of Guv Malhotra

Up Next

Loading suggestions…

Recent Posts

All Posts

Tags

Recent Posts

All Posts