GST PMT-06 Challan for making payment under QRMP Scheme

GST PMT-06 Challan for making payment under QRMP Scheme GST PMT- Challan has gained wide importance these days, especially after the introduction of …

GST PMT-06 Challan for making payment under QRMP Scheme

GST PMT- Challan has gained wide importance these days, especially after the introduction of the QRMP Scheme. Through this article let us understand all about the Form.

What is GST PMT-06?

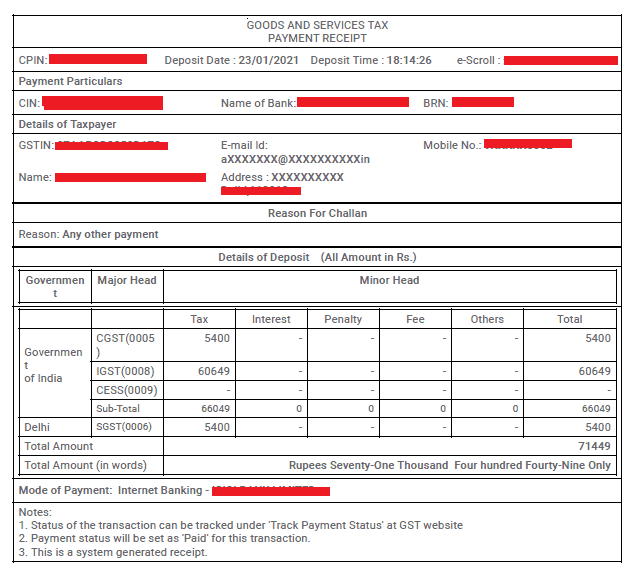

A taxpayer who wants to deposit tax, interest, penalty, fees or any other amount shall generate a challan in FORM GST PMT-06 on the common portal and enter the details of the amount to be deposited by him.

This is not a new concept. This is the same old challan we have been using to pay tax while filing GSTR-3B. Only the FORM GST PMT-06 has come into more notice amid QRMP Scheme.

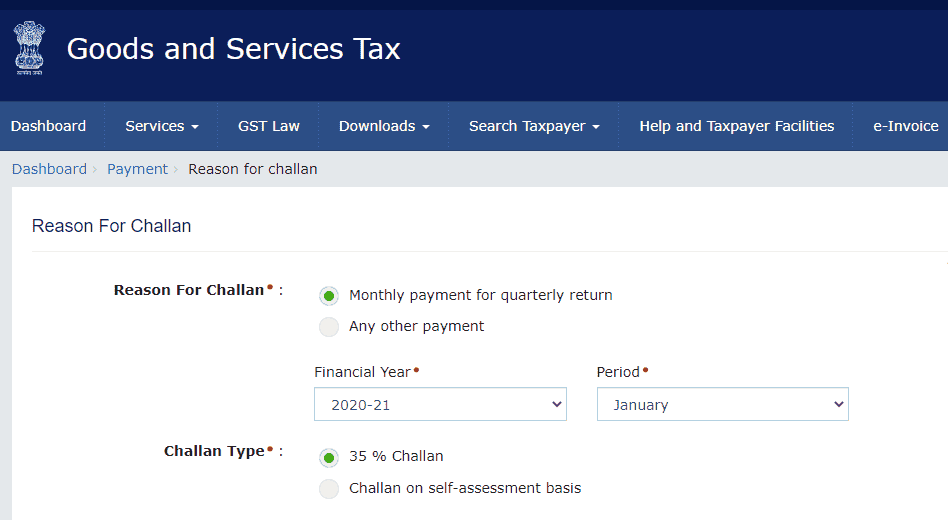

How to Access the GST PMT-06 Challan?

How to Access the GST PMT-06 Challan?

Monthly Payment for Quarterly Return will further be followed by:

Monthly Payment for Quarterly Return will further be followed by:

What are the Due Dates for making Payment of GST Output Liability?

How to Calculate Outstanding Tax Liability for Taxpayers under QRMP Scheme and otherwise?

The Tax liability will be reduced by the amount present in the Cash and credit ledger of the taxpayer.

Please note the below-mentioned Scenario for Better understanding:

Please note that in the 3rd Scenario, the Taxpayer can choose a payment option in M2 as in M1 he was not required to make any tax payment, thus the question of choosing a payment option did not arise.

What is the Late Fees Applicable on delayed Filing of Form GST PMT-06?

No Late Fees is applicable on delayed Filing of Form GST PMT-06.

What is the interest Applicable on delayed payment/short payment of taxes via Form GST PMT-06?

How to Access the GST PMT-06 Challan?

- Go to Services Tab

- Click on Payments

- Click on Create Challan

- Monthly Payment for Quarterly Return; In case you are making payment under QRMP Scheme

- Any other payment

Monthly Payment for Quarterly Return will further be followed by:

- 35% Challan

- Challan on a self-assessment basis

- 35% Challan should be selected when you are making payment through Fixed Sum Method

- Challan on a self-assessment basis should be selected if you are self-assessing your tax.

| Taxpayer | Challan Option | ||

| M1 | M2 | M3 | |

| QRMP Opted | Monthly Payment for Quarterly Return | Monthly Payment for Quarterly Return | Any other payment |

| QRMP Not Opted | Any other payment | Any other payment | Any other payment |

| Taxpayer | M1 | M2 | M3 |

| QRMP Opted | 25th of next Month | 25th of next Month | 22nd/or 24th as per your Place of Bussiness |

| QRMP Not Opted | 20th of next Month | 20th of next Month | 20th of next Month |

| Taxpayer | M1 | M2 | M3 | ||

| QRMP Opted | 35% Payment Option | If RP was a Quarterly Filler | 35% of Tax paid in cash in Previous Quarter | 35% of Tax paid in cash in Previous Quarter | Actual Liability via GSTR-3B |

| If RP was a Monthly Filler | 100% of Tax paid in cash in Previous month | 100% of Tax paid in cash in Previous month | Actual Liability via GSTR-3B | ||

| Self Assessment | Self Assessed Tax | Self Assessed Tax | Actual Liability via GSTR-3B | ||

| QRMP Not Opted | Actual Liability via GSTR-3B | Actual Liability via GSTR-3B | Actual Liability via GSTR-3B | ||

| Senarios | Taxpayer | Tax Liability to be discharged by GST PMT-09 | ||

| M1 | M2 | |||

| 1 | Nil Liability | 35% Payment Option | NA | NA |

| Self Assessment | NA | NA | ||

| 2 | Adequate Cash/ Credit Balance | 35% Payment Option | NA | NA |

| Self Assessment | NA | NA | ||

| 3 | Adequate Cash/ Credit Balance in M1 but not in M2 | 35% Payment Option | NA | Auto-Generated Challan |

| Self Assessment | NA | Self Assessed Amount | ||

| 4 | Inadequate Cash/ Credit Balance | 35% Payment Option | Auto-Generated Challan | Auto-Generated Challan |

| Self Assessment | Self Assessed Amount | Self Assessed Amount | ||

- Delayed Filing of Form GST PMT-06

- Interest Short Payment of Taxes

About Author

CA Pratibha Goyal

Co Founder

CA Pratibha Goyal is Chartered Accountant qualified in 2016, is a Member of The Institute of Chartered Accountants of India having wide experience in the field of Auditing, Taxation, ROC, GST and Secretarial matters etc.

She has written over a thousand articles & has made several videos on topics related to Auditing & Taxation. As a Speaker she has delivered various sessions on various branches of NIRC of ICAI.

CA Pratibha Goyal is Chartered Accountant qualified in 2016, is a Member of The Institute of Chartered Accountants of India having wide experience in the field of Auditing, Taxation, ROC, GST and Secretarial matters etc.

She has written over a thousand articles & has made several videos on topics related to Auditing & Taxation. As a Speaker she has delivered various sessions on various branches of NIRC of ICAI.

Studycafe

Studycafe New Delhi, Delhi, India

New Delhi, Delhi, India 1486

1486My Recent Articles

- Biggest Labour Reform in Indian History: 4 Labour Codes Effective from today

- Tax Audit and ITR Due date not extended in this case: Know More

- Government notifies Agreement and Protocol between India and Qatar [Read Notification]

- CA Breaking: Results of ICAI Examination to be announced soon, Know probable Date

- Breaking: GSTR-3B Due Date for September 2025 extended by CBIC amid Diwali Festivities

Up Next

Loading suggestions…

Recent Posts

All Posts

Recent Posts

All Posts