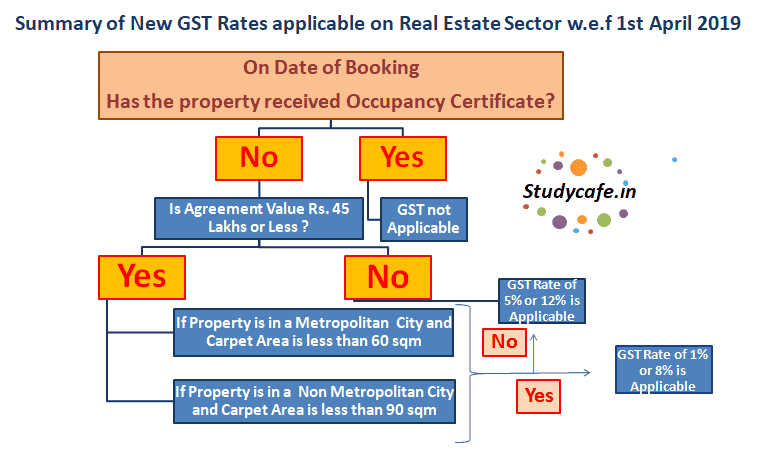

Summary of New GST Rates applicable on Real Estate Sector w.e.f 1st April 2019

Summary of New GST Rates applicable on Real Estate Sector w.e.f 1st April 2019 GST Council in the 34th meeting held on 19th March, 2019 at N

CA Deepak GuptaMar 24, 2019

Last update on Mar 24, 2019

Summary of New GST Rates applicable on Real Estate Sector w.e.f 1st April 2019

GST Council in the 34th meeting held on 19th March, 2019 at New Delhi discussed the operational details for implementation of the recommendations made by the council in its 33rd meeting for lower effective GST rate of 1% in case of affordable houses and 5% on construction of houses other than affordable house.

This step was taken to boost the real estate sector and make housing more affordable as housing is one of the basic need of the Indian economy.

The Summary of New GST Rates applicable on Real Estate Sector w.e.f 1st April 2019 is given below for reference:

Particulars

Applicability

Rate of Tax

Input Tax Credit

Relevant Notification for GST Rate for under construction property

On ready-to-move (RTM) properties for which completion certificates are issued

Not applicable Because Sale of building is treated as activity or transaction which shall be treated neither as a supply of good nor a supply of service as per SCHEDULE III of CGST Act,2017

Not available

SCHEDULE III of CGST Act, 2017

On Under Construction Properties (For Homes Purchased Under Credit-Linked Subsidy Scheme)

Applicable as supply of services as per Schedule I of CGST Act, 2017

12% or 8% as the case maybe.

[See Note 2]

Available

Notification No. 11/2017-Central Tax (Rate) dated the 28th June, 2017 as amended upto 1st January, 2019

On Under Construction Properties (For Homes Purchased Under Credit-Linked Subsidy Scheme)

Decision taken in 34th GST council Meeting

1%

Not available

Official Press Release

On Under Construction Properties (Other than above)

Applicable as supply of services as per Schedule I of CGST Act, 2017

18% or 12% as the case maybe.

[See Note 1]

Available

Notification No. 11/2017-Central Tax (Rate) dated the 28th June, 2017 as amended upto 1st January, 2019

On Under Construction Properties (Other than above)

Decision taken in 34th GST council Meeting

5%

Not available

Official Press Release

On Land purchase and sale

Not applicable. As per Schedule III, sale of land is neither supply of goods nor services.

Not available

SCHEDULE III of CGST Act, 2017

Works contract

Applicable

18%

Available

Notification No. 11/2017-Central Tax (Rate) dated the 28th June, 2017 as amended upto 1st January, 2019

Composite supply of works contract

Applicable

18%

Available

Notification No. 11/2017-Central Tax (Rate) dated the 28th June, 2017 as amended upto 1st January, 2019

Composite supply of works Contract to Government Authorities

Applicable

12%

Available

Notification No. 11/2017-Central Tax (Rate) dated the 28th June, 2017 as amended upto 1st January, 2019

Composite supply of works contract for use by general public

Applicable

12%

Available

Notification No. 11/2017-Central Tax (Rate) dated the 28th June, 2017 as amended upto 1st January, 2019

Composite supply of works contract Affordable Housing

Applicable

12%

Available

Notification No. 11/2017-Central Tax (Rate) dated the 28th June, 2017 as amended upto 1st January, 2019

Note 1 : GST Rate for under construction property is 18%. But in case transfer of land is involved with transfer of property, the value of supply of land is considered as 1/3rd of value of supply. Effective rate of GST is 12% in Such cases.

GST Rate for under construction property

18%

Less: 1/3 of GST Rate for under construction property when land is transferred along with supply.

6%

Effective GST Rate for under construction property

12%

Note 2 : Similarly Effective GST Rate of 8% will be applicable when GST Rate of 12% exists. [Where transfer of land is involved with transfer of property]

GST Rate for under construction property (For Homes Purchased Under Credit-Linked Subsidy Scheme)

12%

Less: 1/3 of GST Rate for under construction property when land is transferred along with supply.

4%

Effective GST Rate for under construction property

8%

[caption id="attachment_60951" align="aligncenter" width="531"]Summary of New GST Rates applicable on Real Estate Sector w.e.f 1st April 2019[/caption]

Disclaimer: The entire contents of this document have been prepared on the basis of relevant provisions and as per the information existing at the time of the preparation. Although care has been taken to ensure the accuracy, completeness and reliability of the information provided, I assume no responsibility therefore. Users of this information are expected to refer to the relevant existing provisions of applicable Laws. The user of the information agrees that the information is not a professional advice and is subject to change without notice. I assume no responsibility for the consequences of use of such information.In no event shall I shall be liable for any direct, indirect, special or incidental damage resulting from, arising out of or in connection with the use of the information.

About Author

CA Deepak Gupta

Co Founder

CA Deepak Gupta,is Co-founder of Studycafe. He is Microsoft Office Specialist and Corporate Trainer of AI Tools, Microsoft Excel.He is Finance Influencer having more than 250K followers on Social Media. CA Deepak Gupta, is Having more than 14 plus years of experience, and he has Worked with best brands Like, Hero, Wipro, Ericsson before Starting Studycafe. He has Trained more than 20000 Persons in Microsoft Excel, PowerPoint, Power BI, Google Sheet, Google Forms and Other Tools.

StudyCafe

StudyCafe Delhi, Delhi, India

Delhi, Delhi, India 3423

3423