GSTR 3B to be filed for August to December,2017

GSTR 3B to be filed for August to December,2017 GSTR 3B is a simplified form of return introduced by the CBEC that needs to be filled on sel

Table of Contents

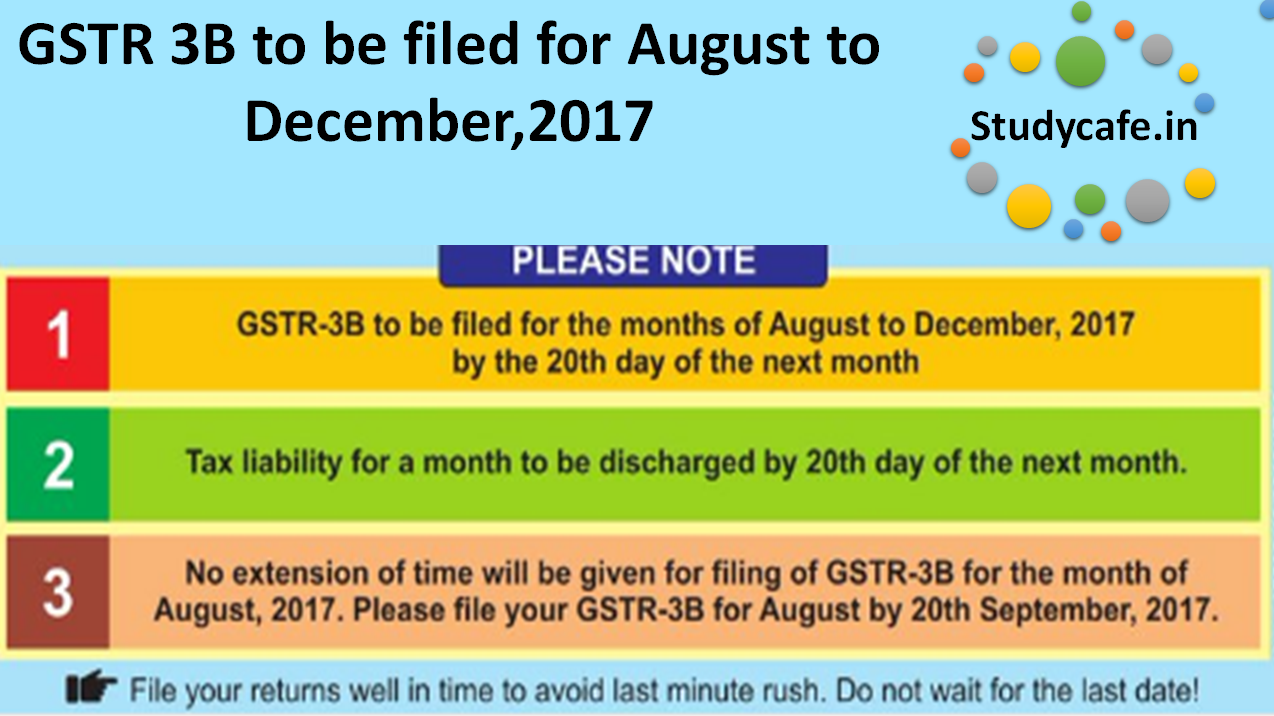

GSTR 3B to be filed for August to December,2017

GSTR 3B is a simplified form of return introduced by the CBEC that needs to be filled on self assessment basis. It is the form of returnin which taxpayers need to declare only the summary of outward and inward supplies unlike the invoice-wise details required in Form GSTR-1 and Form GSTR-2. Earlier it was only to be filed by the first two months i.e July 2017 & August 2017.But considering the current scenario of confusion in general public at large and the problems that are being faced on the GSTN portal.The GST council has decided in 21st meeting held on 09.09.2017 at Hyderabad that GSTR-3B to be filed regularly from month August to December, 2017. Check press release for the same. Initially the due date for filing GSTR 3B was 20th day of the following month. But as you can see in the press release above, there is a long list of due date extensions for return filing the month of July,2017. Even the due date for GSTR 3B for the month of July was extended twice by issuing notifications for the same. There is a lot of confusion whether the due date for GSTR 3B for the month of August 2017 is extendedWhat is the new due date for filing GSTR3B for August month What is the due date of GSTR 3B for August 2017 Only GSTR 3B is to be filed or other monthly returns are also required what is the deadline for GSTR 3B for August 2017 etc. etc. Let me make this clear as there is no extension in the due date of GSTR 3B for the month of August 2017. The deadline to file the GSTR 3B return for August is 20th September,2017 only. Whereas the due dates for filing GSTR 1,GSTR 2 andGSTR 3 for the month of August 2017 will be notified again in near future. This were shared on the official twitter handle of CBEC (Last updated on 13/09/2017)|

Month |

Due date  |

1st extension in due date |

2nd extensionin due date |

| July 2017 | 20th August,2017 | 25th August,2017 (Ntfn no. 24/2017) | 28th August,2017 (Ntfn no. 23/2017) |

| August 2017 | 20th September, 2017 |

-  |

- |

| September 2017 | 20thOctober, 2017 (Ntfn no. 35/2017) |

- |

- |

| October 2017 | 20th November, 2017 (Ntfn no. 35/2017) |

- |

- |

| November 2017 | 20th December, 2017 (Ntfn no. 35/2017) |

- |

- |

| December 2017 | 20th January, 2018 (Ntfn no. 35/2017) |

- |

- |

- Form GSTR-3B consists of 6 headings.

- In which you need to give information regarding the summary details/consolidated details pf of outward supplies, inward supplies, eligible Input tax credit and the details regarding the tax payment.

- Click here to download GSTR 3B

- GSTR 3B to be filed mandatorily by all normal registered taxpayers

- Nil returns to be filed in case of no business

- Summary of information about sale and purchase,available input tax credit, tax payable, tax paid is to be furnished

- All input tax credit availed and utilised will be posted in the ITC ledger

- Unutilized ITC can be used in subsequent months

- While filling up form GSTR 3B, dont forget to Save partially filled form by clicking save GSTR 3B button

- After pressing submit, no modification is possible therefore check the details carefully before pressing submit

- If form GST TRAN-1 is submitted Click Check balance button to view the balance available for credit under integrated tax, Central tax, State tax and Cess ( including transitional credit also)

Let us discuss the form GSTR 3B in Detail :

- To begin with One needs to enter the month and year in the space provided on left hand side And it will also require the GSTIN no. and legal name of registered person.

- 3.1 Details of outward supplies and inward supplies liable to reverse charge

- 3.2 Of the supplies shown in 3.1 (a) above, details of inter state supplies made to unregistered persons, composite taxable persons and UIN holders

- 4. Eligible ITC

- Import of Goods: Tax credit of IGST paid on import of goods.

- Import of Service: Tax credit of IGST paid on import of services.

- Inward supplies liable to reverse charge: Details of tax credit which is available for inward supplies of goods and services which are liable for reverse charge mechanism.(For eg. GTA services, purchases from unregistered dealers, sponsorship services etc. Note :import of goods or services will not be included)

- Inward Supplies from ISD:Input tax credit received from Input Service Distributor (ISD).

- All other ITC: Apart from above, any other ITC relating to inward supplies will be recorded here.

- As per rules 42 & 43 of CGST rules

- Others

- 5. Value of Exempt, nil - rated and non GST inward supplies

- Under this heading details of inward supplies for both inter state and intra state made from the composite dealers, inward supplies which are either exempt or nil-rated needs to be recorded separately here.

- Also the details of Non-GST inward supplies forboth inter state and intra stateneeds to be recorded separately here.

- 6.1 Payment of Tax

- 6.2 TDS/TCS credit

- Verification

About Author

Ankita Khetan

Author

765

765My Recent Articles

- ICAI announcement for CA Final Students issued on 7th May 2018

- Intra State E way bill to be roll out in Assam from May 16, 2018

- Press release for incentive for digital payments & change in GST Rate

- Changes in shareholding pattern of GSTN - Press release dated 4th May 2018

- Press Release issued by CBIC for Simplified GST Return System in 27th GST Council meeting

Up Next

Loading suggestions…

Recent Posts

All Posts

Tags

No tags yet.

Recent Posts

All Posts

Tags

No tags yet.