House Rent exceeds Rs. 1 Lakh; Submitting proof of rent compulsory to get HRA Deduction [Income Tax Circular]

![House Rent exceeds Rs. 1 Lakh; Submitting proof of rent compulsory to get HRA Deduction [Income Tax Circular]](https://assets.studycafe.in/uploads/2022/12/House-Rent-exceeds-Rs.-1-Lakh-Submitting-proof-of-rent-compulsory-to-get-HRA-Deduction-Income-Tax-Circular.jpg)

House Rent exceeds Rs. 1 Lakh; Submitting proof of rent compulsory to get HRA Deduction [Income Tax Circular] Central Board of Direct Taxes (CBDT) ha…

Table of Contents

House Rent exceeds Rs. 1 Lakh; Submitting proof of rent compulsory to get HRA Deduction [Income Tax Circular]

Central Board of Direct Taxes (CBDT) has released the Circular on TDS on Salaries for FY 22-23.

As per the Circular Drawing & Disbursing Officer (DDOs) have been authorized u/s 192 to allow certain deductions, exemptions or allowances or set-off of certain loss as per the provisions of the Act for the purpose of estimating the income of the assessee or computing the amount of tax deductible under the said section.

The evidence /proof /particulars for some of the deductions/exemptions/allowances/set-off of loss claimed by the employee such as rent receipt for claiming deduction in House Rent Allowance (HRA), evidence of interest payments for claiming loss from self-occupied house property, etc. is not available to the DDO.

To bring certainty and uniformity in this matter, section 192(2D) provides that person responsible for paying (DDOs) shall obtain from the assessee evidence or proof or particular of claims such as House rent Allowance (where aggregate annual rent exceeds one lakh rupees);

House Rent Allowances or HRA and its calculation

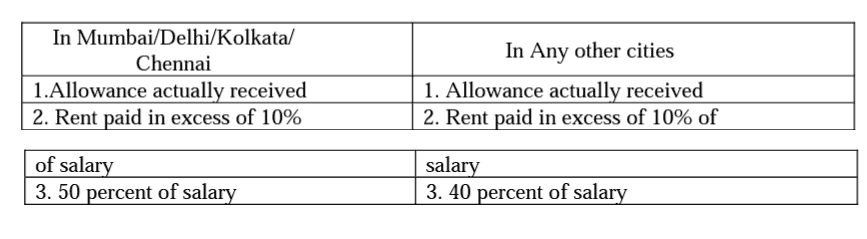

Under section 10(13A) of the Act, any special allowance specifically granted to an assessee by his employer to meet expenditure incurred on payment of rent (by whatever name called) in respect of residential accommodation occupied by the assessee is exempt from Income-tax. The quantum of exemption allowable on account of grant of special allowance to meet expenditure on payment of rent shall be the least of the following:

For this purpose, "Salary" includes dearness allowance, if the terms of employment so provide, but excludes all other allowances and perquisites. It has to be noted that only the expenditure actually incurred on payment of rent in respect of residential accommodation occupied by the assessee subject to the limits laid down in Rule 2A, qualifies for exemption from income-tax.

Rent Paid to Spouse or Parents: Will I get HRA Exemption?

Thus, house rent allowance granted to an employee who is residing in a house/flat owned by him is not exempt from income-tax.

For this purpose, "Salary" includes dearness allowance, if the terms of employment so provide, but excludes all other allowances and perquisites. It has to be noted that only the expenditure actually incurred on payment of rent in respect of residential accommodation occupied by the assessee subject to the limits laid down in Rule 2A, qualifies for exemption from income-tax.

Rent Paid to Spouse or Parents: Will I get HRA Exemption?

Thus, house rent allowance granted to an employee who is residing in a house/flat owned by him is not exempt from income-tax.

For this purpose, "Salary" includes dearness allowance, if the terms of employment so provide, but excludes all other allowances and perquisites. It has to be noted that only the expenditure actually incurred on payment of rent in respect of residential accommodation occupied by the assessee subject to the limits laid down in Rule 2A, qualifies for exemption from income-tax.

Rent Paid to Spouse or Parents: Will I get HRA Exemption?

Thus, house rent allowance granted to an employee who is residing in a house/flat owned by him is not exempt from income-tax.

What evidence can be taken by the employer as proof of rent?

- Rent Agreement

- Rent Receipts,

- PAN/Aadhar of Landlord etc.

About Author

CA Pratibha Goyal

Co Founder

CA Pratibha Goyal is Chartered Accountant qualified in 2016, is a Member of The Institute of Chartered Accountants of India having wide experience in the field of Auditing, Taxation, ROC, GST and Secretarial matters etc.

She has written over a thousand articles & has made several videos on topics related to Auditing & Taxation. As a Speaker she has delivered various sessions on various branches of NIRC of ICAI.

CA Pratibha Goyal is Chartered Accountant qualified in 2016, is a Member of The Institute of Chartered Accountants of India having wide experience in the field of Auditing, Taxation, ROC, GST and Secretarial matters etc.

She has written over a thousand articles & has made several videos on topics related to Auditing & Taxation. As a Speaker she has delivered various sessions on various branches of NIRC of ICAI.

Studycafe

Studycafe New Delhi, Delhi, India

New Delhi, Delhi, India 1486

1486My Recent Articles

- Biggest Labour Reform in Indian History: 4 Labour Codes Effective from today

- Tax Audit and ITR Due date not extended in this case: Know More

- Government notifies Agreement and Protocol between India and Qatar [Read Notification]

- CA Breaking: Results of ICAI Examination to be announced soon, Know probable Date

- Breaking: GSTR-3B Due Date for September 2025 extended by CBIC amid Diwali Festivities

Up Next

Loading suggestions…

Recent Posts

All Posts

Tags

No tags yet.

Recent Posts

All Posts

Tags

No tags yet.