ICAI releases MCQs on Guidance Note on CARO 2020

ICAI releases MCQs on Guidance Note on CARO 2020 The Institute of Chartered Accountants of India Multiple Choice Questions on Guidance Note

ICAI releases MCQs on Guidance Note on CARO 2020

ICAI releases MCQs on Guidance Note on CARO 2020[/caption]

14. Reporting under clause 3(i)(e) is limited to the adequacy of disclosure in the financial statements and to cases where proceedings are initiated with the company being treated as a benamidar.

15. The auditor should review the minutes of meetings of the Board of Directors, Audit Committee, Risk Management Committee, and other secretarial records to verify whether any reference to proceedings against the company under Prohibition of Benami Property Transactions Act 1988 has been made.

16. “Reasonable intervals” does not depend upon the circumstances of each case.

17. Revaluation need not be performed every year or in every reporting period.

The Institute of Chartered Accountants of India

Multiple Choice Questions on Guidance Note on the Companies (Auditor’s Report) Order, 2020

The Ministry of Corporate Affairs issued the Companies (Auditor’s Report) Order, 2020 (CARO 2020) on 25th February 2020. CARO 2020 would be applicable for audits of the financial year 2020-21 and onwards. CARO 2020 contains several significant changes and several new reporting requirements vis-à-vis CARO 2016. The Auditing and Assurance Standards Board (AASB) of ICAI has issued the Guidance Note on the Companies (Auditor’s Report) Order, 2020 (Guidance Note on CARO 2020) under the authority of the Council of ICAI for providing detailed guidance to the members on CARO 2020. MCQs on Clause (i) of CARO 2020Select True/ False:

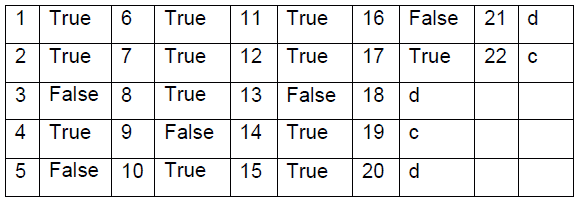

1. Reporting on title deeds of immovable properties is not required where the company is lessee and lease agreement is duly executed in favor of the company. 2. Transfer Development Rights (TDRs), plant and machinery embedded in the land, etc., are not considered as immovable property. 3. The auditor using the work of registered valuer tantamount to using the work of an auditor’s expert as laid out in SA 620, “Using the Work of an Auditor’s Expert”. 4. The reporting under clause 3(i)(e) is not applicable where the notice is received by the company as a beneficial owner. 5. Investment property and Non-current Assets Held for Sale will not be considered by the auditor for reporting under clause 3(i)(a)(A). 6. What constitutes proper records is a matter of professional judgment made by the auditor after considering the facts and circumstances of each case. 7. The purpose of showing the situation of PPE is to make verification possible. 8. Immovable property shall include land, benefits to arise out of the land, and things attached to the earth, or permanently fastened to anything attached to the earth.9. The auditor cannot obtain the support of any legal expert in case there is any dispute or litigation as to the title of the immovable property.

10. Where the proceedings under Prohibition of Benami Property Transactions Act 1988 are initiated post balance sheet date but before the signing of the auditor’s report, the auditor should consider the requirements of SA 560, “Subsequent Events”. 11. It is to be ensured that the information contained in the electronic records remains accessible and unaltered and its origin, destination, date, etc. can be identified. 12. When details of disposals are not available, it may be assumed that the asset sold is the asset that was acquired earliest in point of time. 13. If the PPE register is not maintained by the company, it is not necessary to be mentioned by the auditor while reporting under clause 3(i)(a)(A). [caption id="attachment_90107" align="aligncenter" width="333"] ICAI releases MCQs on Guidance Note on CARO 2020[/caption]

14. Reporting under clause 3(i)(e) is limited to the adequacy of disclosure in the financial statements and to cases where proceedings are initiated with the company being treated as a benamidar.

15. The auditor should review the minutes of meetings of the Board of Directors, Audit Committee, Risk Management Committee, and other secretarial records to verify whether any reference to proceedings against the company under Prohibition of Benami Property Transactions Act 1988 has been made.

16. “Reasonable intervals” does not depend upon the circumstances of each case.

17. Revaluation need not be performed every year or in every reporting period.

Choose the correct option(s):

18. While reporting under clause (i), the auditor has to report on which of the following aspects: a) Benami properties b) Physical verification c) Title deeds d) All of the above 19. The auditor may accept PPE register in electronic form if: a) The controls and security measures in the company are such that once finalized, the PPE register cannot be altered without proper authorization and audit trail b) The PPE register is in such a form that it can be retrieved in a legible form c) Both (a) & (b) d) Neither (a) nor (b) 20. The records relating to property, plant, and equipment should contain the following details: a) Situation b) Original cost c) Component-wise breakup d) All of the above 21. The auditor may have to consider the applicable documentation requirements of intangible assets as laid down in: a) Designs Act, 2000 b) Patents Act, 1970 c) Information Technology Act, 2000 d) All of the above 22. Physical verification of the assets is the responsibility of the ___________ a) auditor b) those charged with governance c) management d) shareholders Answers:About Author

Reetu

Content Manager

Reetu is a Content Writer with 4+ years of experience in GST, Income Tax, Finance, Company Law, Education and Career Related Content. She is a B.COM (Honrs.) Graduate.

Reetu is a Content Writer with 4+ years of experience in GST, Income Tax, Finance, Company Law, Education and Career Related Content. She is a B.COM (Honrs.) Graduate.

Studycafe

Studycafe Delhi, Delhi, India

Delhi, Delhi, India 8072

8072My Recent Articles

- Income Tax Guide for Indian Defence Personnel for Tax Filing, Taxable Allowances and Other Benefits

- Income Tax Return Breaking: ITR Forms released for AY 25-26

- Ex-DRT Officials Sentenced to 5 Years Rigorous Imprisonment by Madras High Court along with Rs.27 Lakh Fine

- GSTN issued Advisory on Case Sensitivity in IRN Generation

- RBI to issue Notes of Rs.10 and Rs.500 bearing Signature of Guv Malhotra

Up Next

Loading suggestions…

Recent Posts

All Posts

Tags

No tags yet.

Recent Posts

All Posts

Tags

No tags yet.