Guidance Note to all CAs certifying Provisional Financial Statements of Non-Corporates:

ICAI has issued a guidance note to all Chartered Accountants certifying provisional financial statements of non-corporates (except LLPs) w.e.f. 01.04.2024.

Guidance Note on Financial Statements of Non-Corporate Entities

Guidance Note to all CAs certifying Provisional Financial Statements of Non-Corporates

The Institute of Chartered Accountants of India (ICAI) has issued a guidance note to all Chartered Accountants certifying Provisional Financial Statements of Non-Corporates (except LLPs) w.e.f. 01.04.2024.

Accounting Standards issued by the Institute of Chartered Accountants of India (ICAI) act as a pillar for a sound financial reporting system of an entity. Accounting Standards prescribe recognition and measurement principles as well as presentation and disclosure requirements for the events, transactions, and various elements of the financial statements. General Purpose Financial Statements prepared in accordance with the Accounting Standards provide relevant and reliable information about the entity to its stakeholders.

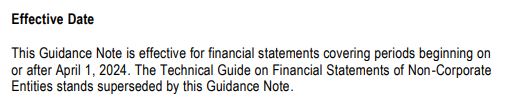

In line with this, the Accounting Standards Board (ASB) of the ICAI had issued a technical guide on financial statements of non-corporate entities recommending the formats of financial statements to strengthen and standardise the financial reporting formats to be followed by non-corporate entities.

The Guidance Note prescribes formats of financial statements for non-corporate entities to enable these entities to communicate their financial performance and financial position in standardised formats, thereby enhancing their comparability.

The Accounting Standards Board of ICAI has prescribed the formats for the presentation of the financial statements of such Non-corporate entities (Sole proprietorships, HUF, Partnership firms, AOP, BOI etc.) in the form of a Guidance Note on Financial Statements of Non-Corporate Entities.

These formats will be applicable for all Provisional Financial certifications and also for next year's tax audit attachments.

Consequences of Non-Compliance of the Same

As per Clause (1) of Part II of the Second Schedule of the CA Act, 1949, a member of the Institute, whether in practice or not, shall be deemed to be guilty of professional misconduct if he contravenes any of the provisions of this Act or the regulations made thereunder or any guidelines issued by the Council.

For Official Guidance Note Download PDF Given Below:

For Official Guidance Note Download PDF Given Below:

For Official Guidance Note Download PDF Given Below:About Author

Reetu

Content Manager

Reetu is a Content Writer with 4+ years of experience in GST, Income Tax, Finance, Company Law, Education and Career Related Content. She is a B.COM (Honrs.) Graduate.

Reetu is a Content Writer with 4+ years of experience in GST, Income Tax, Finance, Company Law, Education and Career Related Content. She is a B.COM (Honrs.) Graduate.

Studycafe

Studycafe Delhi, Delhi, India

Delhi, Delhi, India 8072

8072My Recent Articles

- Income Tax Guide for Indian Defence Personnel for Tax Filing, Taxable Allowances and Other Benefits

- Income Tax Return Breaking: ITR Forms released for AY 25-26

- Ex-DRT Officials Sentenced to 5 Years Rigorous Imprisonment by Madras High Court along with Rs.27 Lakh Fine

- GSTN issued Advisory on Case Sensitivity in IRN Generation

- RBI to issue Notes of Rs.10 and Rs.500 bearing Signature of Guv Malhotra

Up Next

Loading suggestions…

Recent Posts

All Posts

Tags

No tags yet.

Recent Posts

All Posts

Tags

No tags yet.