IGST not Payable on Residential Dwelling Rented for the Purpose Hostel

IGST not Payable on Residential Dwelling Rented for the Purpose Hostel The Hon’ble Karnataka High Court in Taghar Vasudeva Ambrish v. Appellate Autho…

Table of Contents

IGST not Payable on Residential Dwelling Rented for the Purpose Hostel

The Hon’ble Karnataka High Court in Taghar Vasudeva Ambrish v. Appellate Authority for Advance Ruling Karnataka [W.P. No. 14891 of 2020 (T-RES) dated February 07, 2022] quashed the order passed by the AAAR, denying exemption to the assessee on the service of renting of property used for the purpose of a hostel for the students and working women. Held that, such service will fall within the purview of residential dwelling and is used for residential purposes. Thus, exempted from payment of Integrated Goods and Services Tax (“IGST”).

(Author can be reached at [email protected])

DISCLAIMER: The views expressed are strictly of the author and A2Z Taxcorp LLP. The contents of this article are solely for informational purpose and for the reader’s personal non-commercial use. It does not constitute professional advice or recommendation of firm. Neither the author nor firm and its affiliates accepts any liabilities for any loss or damage of any kind arising out of any information in this article nor for any actions taken in reliance thereon. Further, no portion of our article or newsletter should be used for any purpose(s) unless authorized in writing and we reserve a legal right for any infringement on usage of our article or newsletter without prior permission.

To Read Judgment Download PDF Given Below:

(Author can be reached at [email protected])

DISCLAIMER: The views expressed are strictly of the author and A2Z Taxcorp LLP. The contents of this article are solely for informational purpose and for the reader’s personal non-commercial use. It does not constitute professional advice or recommendation of firm. Neither the author nor firm and its affiliates accepts any liabilities for any loss or damage of any kind arising out of any information in this article nor for any actions taken in reliance thereon. Further, no portion of our article or newsletter should be used for any purpose(s) unless authorized in writing and we reserve a legal right for any infringement on usage of our article or newsletter without prior permission.

To Read Judgment Download PDF Given Below:

Facts:

Taghar Vasudeva Ambrish (“the Petitioner”) is the owner of a residential property wherein, the ownership of the building was partitioned among five of the owners (“the Lessors”) with each individual being the absolute owner of a specified floor of the building. The Lessors collectively entered into a lease deed in with M/S. D Twelve Spaces Private Limited (“the Lessee”) on June 21, 2019., wherein, the Lessors leased out their portion of the building to the Lessee for the purpose of sub-lease/sub-licence and to be used as hostel for providing long term accommodation to students and working professionals with the duration of stay ranging from 3 months to 12 months, in return for the consideration of an agreed monthly rent. As per exemption notification the Central Government exempted payments of goods and services in respect of services mentioned therein, which includes renting services which are provided with respect to residential dwelling for use as residence. This petition has been filed by the Petitioner being aggrieved by the ruling of the AAAR, Karnataka in Advance Ruling No. KAR/AAAR-01/2020-21 dated August 31, 2020 (“the Impugned Order”), wherein the AAAR upheld the order passed by the AAR, Karnataka, holding that the Petitioner would not be entitled to the exemption on services viz., renting of residential dwelling for use as a residence under Entry 13 of the Notification No.9/2017 - Integrated Tax (Rate) dated 28.06.2017 (“Exemption Notification”) as the property rented out by the Petitioner is a hostel building which is more akin to sociable accommodation rather than what is commonly understood as residential accommodation. Further held that, the exemption is available only if the residential dwelling is used as a residence by the person who has taken the same on rent / lease.Issue:

Whether the benefit of the exemption would be available to the Petitioner under exemption notification?Held:

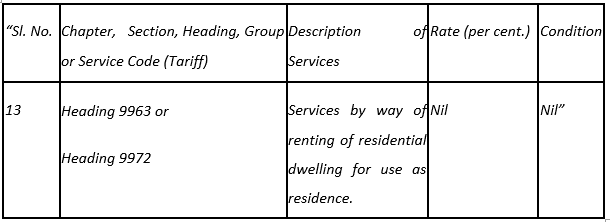

The Hon’ble Karnataka High Court in W.P. No. 14891 of 2020 (T-RES) dated February 07, 2022 held as under:- Analysed Entry 13 of the Exemption Notification and noted that it provides exemption of Integrated Goods and Services Tax (“IGST”) in respect of 'services by way of renting of residential dwelling by way of use as residence', but the expression 'residential dwelling' has not been defined.

- Further noted that as per the education guide issued by CBIC which provides that in normal trade parlance residential dwelling means any residential accommodation and is different from hotel, motel, inn, guest house etc. which is meant for temporary stay. The clarification is in the absence of anything to the contrary in the Act, binds the Respondent.

- Observed that the residential dwelling is being rented, as a hostel to the students and working women will fall within the purview of residential dwelling as the same is used by the students as well as the working women for the purposes of residence. Further, the residential dwelling is being used for the purposes of residence.

- Further observed that, the Exemption Notification does not require the lessee itself use the premises as residence. Therefore, the benefit of exemption cannot be denied to the Petitioner on the ground that the lessee is not using the premises.

- Relied on the judgement of Hon’ble Supreme Court in Kishore Chandra Singh v. Babu Ganesh Prasad Bhagat AIR 1954 SC 316 wherein, it was held that expression residence only connotes that a person eats, drinks and sleeps at that place and not necessarily that the person should own it.

- Stated that, when the word is not defined in the Act itself, it is permissible to refer to the dictionaries to find out the general sense in meaning can be assigned to the expression 'residential dwelling' and it cannot be held that the same does not include hostel which used for residential purposes by students or working women.

- Quashed the Impugned Order.

- Held that the service provided by the Petitioner is covered under Entry 13 of the Exemption Notification and is entitled to avail the benefit of exemption.

Relevant Provision:

Entry 13 of the Exemption Notification:

(Author can be reached at [email protected])

DISCLAIMER: The views expressed are strictly of the author and A2Z Taxcorp LLP. The contents of this article are solely for informational purpose and for the reader’s personal non-commercial use. It does not constitute professional advice or recommendation of firm. Neither the author nor firm and its affiliates accepts any liabilities for any loss or damage of any kind arising out of any information in this article nor for any actions taken in reliance thereon. Further, no portion of our article or newsletter should be used for any purpose(s) unless authorized in writing and we reserve a legal right for any infringement on usage of our article or newsletter without prior permission.

To Read Judgment Download PDF Given Below:About Author

A2ZBimal Jain

Chartered Accountant

CA Bimal Jain is a Member of Institute of Chartered Accountants of India since May 1994 and Member of Institute of Company Secretaries of India since December 2006 along with a Bachelors degree in Law. Also, he is a Qualified SAP - FI/CO Consultant and has more than 21 years of experience in Indirect Taxation and specializes in all aspects of Service Tax, Value Added Tax (VAT)/ Central Sales Tax (CST), Central Excise, Customs, Foreign Trade Policy (FTP), Special Economic Zone (SEZ), Export Oriented Unit (EOU), Export-Import Laws and well acquainted with the concept and impact of way forward Goods and Services tax (GST).

CA Bimal Jain is a Member of Institute of Chartered Accountants of India since May 1994 and Member of Institute of Company Secretaries of India since December 2006 along with a Bachelors degree in Law. Also, he is a Qualified SAP - FI/CO Consultant and has more than 21 years of experience in Indirect Taxation and specializes in all aspects of Service Tax, Value Added Tax (VAT)/ Central Sales Tax (CST), Central Excise, Customs, Foreign Trade Policy (FTP), Special Economic Zone (SEZ), Export Oriented Unit (EOU), Export-Import Laws and well acquainted with the concept and impact of way forward Goods and Services tax (GST).

A2Z Taxcorp LLP

A2Z Taxcorp LLP Delhi, Delhi, India

Delhi, Delhi, India 468

468My Recent Articles

- Actions taken by the department during enquiry need not necessarily be termed as harassment

- Who are liable to generate e-invoice w.e.f October 1, 2022

- Personal penalty cannot be imposed on the Chairman of the Company for failure in ensuring proper accounting of the goods

- Stayed the order of cancellation of GST Registration of the assessee for continuing the trading activities

- Can CA be arrested- Section 69 vs Section 132 of the CGST Act

Up Next

Loading suggestions…

Recent Posts

All Posts

Tags

Recent Posts

All Posts