Tax Audit Due Date, Criteria and Requirements

Tax Audit Due Date, criteria and requirements As due date of Tax Audit for year 2018-2019 is approaching near, here are some of the FAQ's on

Tax Audit Due Date, criteria and requirements

As due date of Tax Audit for year 2018-2019 is approaching near, here are some of the FAQ's on Basics of Tax Audit under Income Tax Act.

What is tax Audit

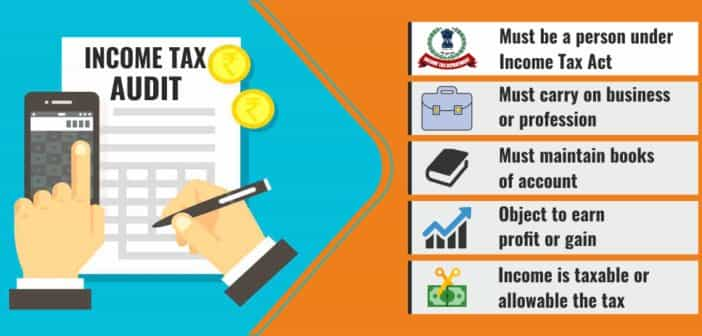

The dictionary meaning of the term "audit" is check, review, inspection, etc. There are various types of audits prescribed under different laws like company law requires a company audit, cost accounting law requires a cost audit, etc. The Income-tax Law requires the taxpayer to get the audit of the accounts of his business/profession from the view point of Income-tax Law.

Section 44AB gives the provisions relating to the class of taxpayers who are required to get their accounts audited from a chartered accountant. The audit under section 44AB aims to ascertain the compliance of various provisions of the Income-tax Law and the fulfillment of other requirements of the Income-tax Law. The audit conducted by the chartered accountant of the accounts of the taxpayer in pursuance of the requirement of section 44AB is called tax audit.

The chartered accountant conducting the tax audit is required to give his findings, observation, etc., in the form of audit report. The report of tax audit is to be given by the chartered accountant in Form Nos. 3CA/3CB and 3CD. .

Who is required to get the accounts audited

As per section 44AB of the Income Tax Act, 1961, following classes of persons are mandatorily required to get their accounts audited:-

1.) An individual who in engaged in any business and his annual turnover is 1 crore of more in the financial year under question.

2.) An individual who is engaged in any profession and his gross receipts is 50 lakhs or more in the financial year under question.

3.) An individual who opts for the presumptive taxation scheme under Section 44AD but later on claims that the profits for said business is lower than the profits calculated in accordance with the presumptive taxation scheme. Also, where such an assessee claims that his total income is less than the basic exemption limit, then he is required to get his accounts audited.

4.) An individual who opts for presumptive taxation scheme under Section 44AE but then claims that the profits for such business are lower than the profits calculated in accordance with the limits laid down under section 44AE.

5.) An individual who qualifies to choose the presumptive taxation scheme under Section 44BBB but then claims that the profits for such business are lower than the profits calculated in accordance with the limits laid down under section 44BBB.

What is the due date to get the accounts audited

The due date for getting the accounts audited under section 44AB is 30th September (subject to extensions) of the assessment year. The assessee should get its accounts audited by a practicing chartered accountant by this date, or any other date notified in this regard and obtain a tax audit report duly signed and certified by him. Also, The tax audit report is to be electronically filed by the chartered accountant to the Income Tax Department. After the filing of the Income Tax Report by the chartered accountant, the taxpayer has to approve the submitted reports using the e-fling account with the Income Tax Department.

What if the accounts are already audited under any other law

In such cases, the taxpayer need not get his accounts audited again for income tax purposes. It is sufficient if accounts are audited under such other law before the due date of filing the return. The taxpayer can furnish this prescribed audit report under Income tax law.

What are the consequences for not getting the accounts audited

In case any person, who is liable to get his accounts audited under section 44AB, fails to get his accounts audited, then the provisions of section 271B shall apply. Any person who doesnt get the accounts audited will be imposed with a penalty of:

1.) 0.5% of the total sales in business or 0.5% of the total receipts in profession of the current financial year.

2.) A sum of Rs 1,50,000/-

The lower among the above will be levied as penalty.

About Author

Tista

Student

Delhi, Delhi, India

Delhi, Delhi, India 39

39My Recent Articles

- Cancellation and Revocation of Cancellation of GST Registration

- Expectations from Budget 2020

- Deduction in respect of interest on loan taken for affordable housing Section 80EEA

- Carry forward and Set-off of Losses in case of Start-ups

- TDS PROVISIONS UNDER GST, TDS RATE IN GST, PERSONS NOTIFIED TO DEDUCT TDS

Loading suggestions…

Recent Posts

All Posts

Tags

Recent Posts

All Posts