Income Tax Rebate under Old and New Tax Regime for FY 2025-26:

This article discusses an important benefit provided by the income tax, which is rebate u/s 87A of the income tax Act.

Income Tax Rebate for FY 2025-26 under Both Tax Regime

Table of Contents

Income Tax Rebate under Old and New Tax Regime for FY 2025-26

This article discusses an important benefit provided by the income tax, which is rebate u/s 87A of the income tax Act.

Example 2: Tax liability for the Financial year 2025-26 in the case of Y (who is a resident individual). His net income (computed under the alternative tax regime under section 115BAC (1A)) is as follows:-

Situation 1 - Net Income: Rs.3,10,000

Situation 2 - Net Income: Rs.6,10,000

Situation 3 - Net Income: Rs.7,00,000

Situation 4 - Net Income: Rs.9,00,000

Y does not opt for the regular tax regime under section 115BAC(6).

Please note:

In above Illustrations, Tax Does not include Cess.

The Understanding based on ITR Filing Utilities of FY 2023-24.

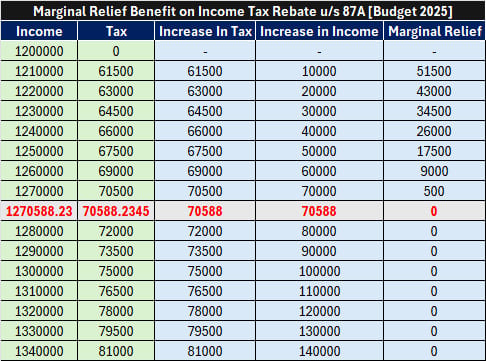

The income of Mr. A is Rs. 1200000. His Tax Liability will be Zero as he is eligible for a Tax Rebate of Rs. 60,000.

The income of Mr. B is Rs. 1210000. His Tax Liability will be Rs. 61500 as he is not eligible for a Tax Rebate.

In Above, Increase in Income is Rs. 10000, but increase in tax is Rs. 61500. Thus increase in income is more than increase in Tax.

Thus Mr. B is eligible for Marginal Relief of Rs. 10000. His Final Tax Liability will be Rs. 10400.

Analysis for Marginal Relief Benefit on Income Tax Rebate u/s 87A is given below.

Rebate u/s 87A for FY 2025-26

With a view to providing tax relief to individual taxpayers who are in a lower tax bracket, a tax rebate is provided under Section 87A. Conditions for Rebate: This rebate is available if the following two conditions are satisfied -- The taxpayer is a resident individual (he/she may be ordinarily resident or not ordinarily resident).

- His total income or net income or taxable income does not exceed Rs.5 Lakh in the Old Tax Regime or Rs.12 Lakh in the New Tax Regime.

- an amount of income tax payable on his total income or

- an amount up to Rs. 60,000. (whichever is less)

- an amount equal to the amount of income tax payable on his total income or

- an amount of Rs. 12,500. (whichever is less)

| Particulars | Situation 1 | Situation 2 | Situation 3 | Situation 4 |

| Net Income | 3,60,000 | 6,50,000 | 11,00,000 | 13,00,000 |

| Income tax on net income | 0 | 12,500 | 50,000 | 75,000 |

| Less: Rebate under section 87A | 0 | 12,500 | 50,000 | Nil |

| Balance | Nil | Nil | Nil | 75,000 |

| Add: Surcharge | Nil | Nil | Nil | Nil |

| Total | Nil | Nil | Nil | 75,000 |

| Add: Health and education cess @4% | Nil | Nil | Nil | 3,000 |

| Tax Liability | Nil | Nil | Nil | 78,000 |

| Particulars | Situation 1 | Situation 2 | Situation 3 | Situation 4 |

| Net Income | 3,10,000 | 6,10,000 | 7,00,000 | 9,00,000 |

| Income tax on net income | 500 | 16,000 | 25,000 | 45,000 |

| Less: Rebate under section 87A | 500 | 16,000 | 25,000 | Nil |

| Balance | Nil | Nil | Nil | 45,000 |

| Add: Surcharge | Nil | Nil | Nil | Nil |

| Total | Nil | Nil | Nil | 45,000 |

| Add: Health and education cess @4% | Nil | Nil | Nil | 1,800 |

| Tax Liability | Nil | Nil | Nil | 46,800 |

No Rebate on Special Incomes:

As per the Budget Memo:

The provisions of sub-section (1A) of section 115BAC are subject to the other provisions of Chapter XII i.e. determination of tax in certain special cases. Hence, proviso to section 87A clearly provides that tax on incomes chargeable at special rates (for e.g.: capital gains u/s 111A, 112 etc.) as specified under various provisions of Chapter XII, are not included while determining the rebate of income-tax under the first proviso to section 87A.Rebate in New Tax Regime [Financial year 2025-26]

| Income Chargeable to Tax U/S 115BAC | Special Rate Income (Assuming STCG u/s 111A) | Total Income | Total Tax | Rebate |

| Rs. 12,00,000 | 0 | Rs. 12,00,000 | NTR: Rs. 60,000 | Rs. 60,000 |

| 0 | Rs. 12,00,000 | Rs. 12,00,000 | STCG: Rs. 2,40,000 | 0 |

| Rs. 9,00,000 | Rs. 2,00,000 | Rs. 11,00,000 | NTR: Rs. 30,000 STCG: Rs. 40,000 | Rs. 30,000 |

| Rs. 9,00,000 | Rs. 4,00,000 | Rs. 13,00,000 | NTR: Rs. 30,000 STCG: Rs. 80,000 | Rs. 30,000 |

| Rs. 13,00,000 | Rs. 4,00,000 | Rs. 17,00,000 | NTR: Rs. 75,000 STCG: Rs. 80,000 | 0 |

What is Marginal Relief Benefit on Income Tax Rebate u/s 87A?

Marginal Relief under New Tax Regime - The rebate under section 87A is subject to marginal relief from the assessment year 2024-25. If net income exceeds Rs. 12,00,000 but does not exceed Rs. 1270588, income tax on such income cannot exceed the amount by which the net income exceeds Rs. 12,00,000. Let us understand this with the below mentioned example:| Particulars | Income | Tax | Increase In Tax | Increase in Income | Marginal Relief |

| Mr. A | 1200000 | 0 | Tax Liability is Zero due to rebate | ||

| Mr. B | 1210000 | 61500 | 61500 | 10000 | 51500 |

About Author

CA Pratibha Goyal

Co Founder

CA Pratibha Goyal is Chartered Accountant qualified in 2016, is a Member of The Institute of Chartered Accountants of India having wide experience in the field of Auditing, Taxation, ROC, GST and Secretarial matters etc.

She has written over a thousand articles & has made several videos on topics related to Auditing & Taxation. As a Speaker she has delivered various sessions on various branches of NIRC of ICAI.

CA Pratibha Goyal is Chartered Accountant qualified in 2016, is a Member of The Institute of Chartered Accountants of India having wide experience in the field of Auditing, Taxation, ROC, GST and Secretarial matters etc.

She has written over a thousand articles & has made several videos on topics related to Auditing & Taxation. As a Speaker she has delivered various sessions on various branches of NIRC of ICAI.

Studycafe

Studycafe New Delhi, Delhi, India

New Delhi, Delhi, India 1486

1486My Recent Articles

- Biggest Labour Reform in Indian History: 4 Labour Codes Effective from today

- Tax Audit and ITR Due date not extended in this case: Know More

- Government notifies Agreement and Protocol between India and Qatar [Read Notification]

- CA Breaking: Results of ICAI Examination to be announced soon, Know probable Date

- Breaking: GSTR-3B Due Date for September 2025 extended by CBIC amid Diwali Festivities

Up Next

Loading suggestions…

Recent Posts

All Posts

Tags

No tags yet.

Recent Posts

All Posts

Tags

No tags yet.