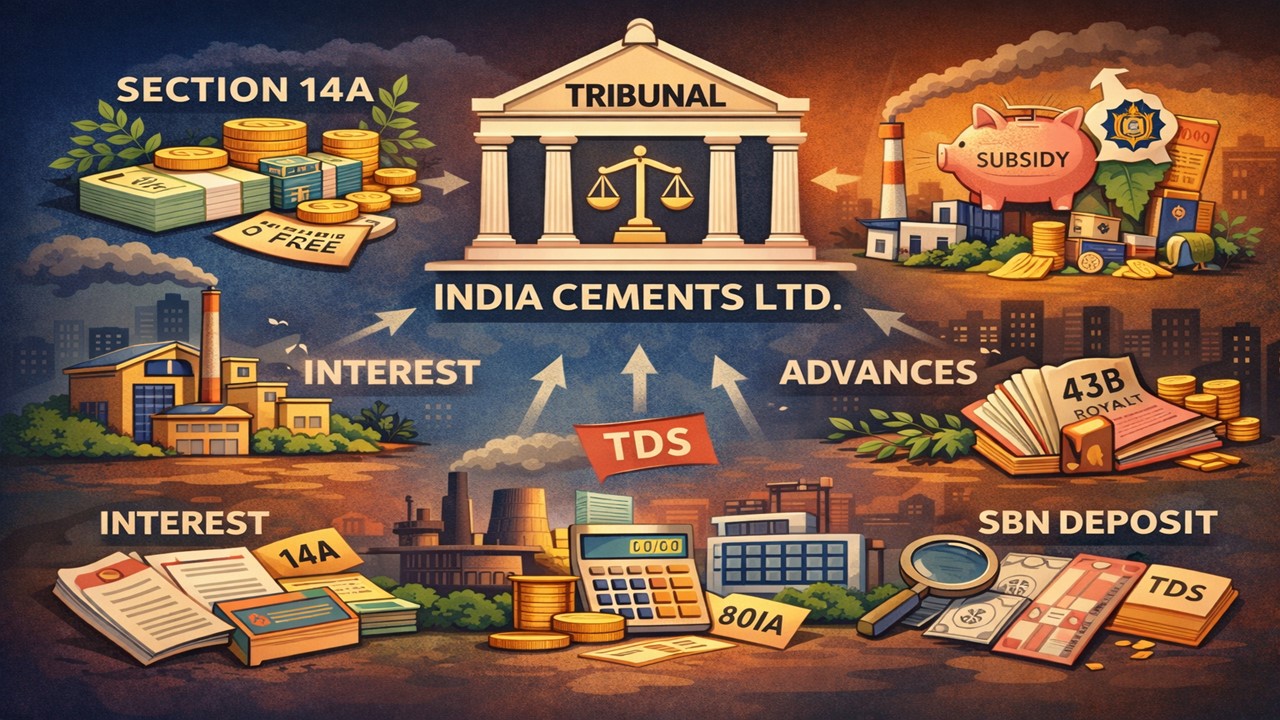

ITAT Partly Allows Appeal on Section 14A, Interest, Subsidy and Other Tax Issues:

The assessee, The India Cements Ltd., filed an appeal before the income tax department, raising several grounds covering Section 14A disallowance, interest on loans, vastu fees, subsidies, and royalty.

ITAT Gives Relief on Section 14A and 80-IA Claims, But Subsidy and Royalty Taxability Upheld

ITAT Partly Allows Appeal on Section 14A, Interest, Subsidy and Other Tax Issues

The Income Tax Appellate Tribunal partly allowed a company's appeal against CIT(A)'s order confirming the AO's additions. The assessee, The India Cements Ltd., filed an appeal before the income tax department, raising several grounds covering Section 14A disallowance, interest on loans, vastu fees, subsidies, and royalty.

Section 14A Disallowance

The AO disallowed expenses under section 14A of the Income Tax Act 1961 in terms of rule 8D of the Income Tax Rules 1962, saying that the expenditure incurred in relation to earning tax-free income is not an allowable expense. The AO had noted that the assessee held substantial investments that could generate tax-free income for the assessee. The AO made an addition of Rs 10,744,451, which was earned by the assessee company from the sale of mutual funds exempted under section 10(39) of the Act. The assessee argued that the investments were made out of its own funds, and the same should not be disallowed.

The Tribunal, however, the computation was limited to only investments yielding exempt income, citing the assessee's own case for AY 2013-14. The Tribunal directed the AO to recompute and restrict the disallowance to 1% of the monthly average of the exempt income-yielding investments, as per amended Rule 8D.

Interest on Interest-Free Advances

The AO had disallowed interest on the interest-free advances given by the assessee to its subsidiaries. The company claimed that the advances were given for the purpose of the business and the assessee had enough own funds to cover the average balance of interest-free advances. Additionally, in the assessee's own case for the previous year, the tribunal had deleted the same order. The Tribunal cited the Supreme Court's ruling, which held that if the interest-free loans given are sufficiently covered with the non-interest-bearing fund available with the assessee, then disallowance of interest on borrowed funds cannot be made. Therefore, the assessee directed the AO to delete the disallowance.

Disallowance of Depreciation

The AO and CIT(A) had rejected depreciation on the payment made by the assessee to Dr K. Venkatesan, a vastu expert, which was capitalised to the cost of buildings. The AO held that such expenses cannot be treated as business expenditures. The tribunal upheld this disallowance based on its AY 2013-14 ruling in the assessee's own case.

Taxability of Maharashtra Govt Subsidy

The assessee was granted a subsidy by the Maharashtra government for establishing a new manufacturing unit in the state. The assessee company was allowed to keep the sales tax collected on the sale of goods produced by these manufacturing units instead of giving it to the state government. This amount was adjusted and treated as a subsidy granted by the state government. The assessee claimed that the subsidy received at Parli Unit, Maharashtra, is a capital receipt. However, the AO held that this subsidy was taxable in nature and added it to the assessee's income.

The Tribunal held that the subsidy is taxable income under section 2(24)(xviii) (Finance Act 2015), citing the case of Hyundai Motor India Ltd. Therefore, the Tribunal upheld the CIT(A) and AO's decision.

Section 43B Royalty Disallowance

The issue was about royalty payable to the government for limestone mining. The AO said this royalty falls under Section 43B and is deductible only when it is actually paid. Since most of the royalty was not paid before the filing of the ROI, it was disallowed. The CIT(A) reduced the allowance to Rs 39,026,158. Since the assessee was not able to explain why the royalty payable to the government under the Mines and Mineral (Development Regulation) Act cannot be subject to provisions under Section 43B of the Act, the Tribunal upheld the decision of CIT(A).

Leave Encashment Disallowance

The AO had disallowed the provision for leave encashment by applying Section 43B, which allows deduction only when payment is made. The company argued that this section cannot be applied while computing book profit under section 115JB. The Tribunal agreed with the company's contention, saying that the AO was required to find whether the provision can be added back or not under the specified clauses set out in Explanation (1) to Section 115JB. Since this was not properly checked, the matter was sent back to the AO for fresh examination.

Disallowance of Interest on Belated TDS

This issue is related to the disallowance of interest paid on late TDS while calculating book profit under section 115JB of the Act. The AO had added back the interest paid on TDS. The Tribunal noted that this issue was already covered in the assessee's favor in their own case for an earlier year. Therefore, the interest paid for the belated deposit of TDS was allowed as a deduction while computing book profit under section 155JB.

Disallowance Under Section 80IA

This issue is related to the disallowance of deduction under section 80IA of the Income Tax Act for two captive power units. TPO disagreed with the benchmarking exercise used by the assessee. The TPO adopted the methods followed by his predecessor, and the allowable deduction was recalculated under Section 80-IA by adopting a rate of Rs 3.53 per unit as per the power generating tariff notified by TNERC and Rs 3.44 per unit as per the Notification of APERC. By using these reduced transfer prices, it was concluded that both power units had incurred a loss, and therefore, the deduction claimed under section 80-IA was disallowed.

The Tribunal noted that the same issue was already decided in the company’s favour in earlier years. So, the Tribunal allowed the deduction and deleted the disallowance.

Addition Under Section 68 Towards SBN Deposit

This issue is related to the addition made under section 68 of the Income Tax Act towards the deposit of Specified Bank Notes during the Demonetization Period. The assessee had explained that the amount was the repayment of loans (advances) by employees who were travelling across different locations on the date of notification of demonetization. They have returned the advances comprising SBNs later.

The Tribunal held that even though the assessee had explained the source of such receipts, the claim was not substantiated. Since the assessee had not submitted any details or evidence substantiating its claim, the Tribunal remitted the matter back to the AO and directed it to submit the supporting evidence.

About Author

Nidhi

Content Writer

Nidhi is a skilled content writer specializing in personal finance. She creates clear, engaging articles on mutual funds, investments, insurance, and wealth-building strategies. With a passion for simplifying complex financial topics, Nidhi helps readers make informed money decisions with confidence. She can be reached at [email protected]

Nidhi is a skilled content writer specializing in personal finance. She creates clear, engaging articles on mutual funds, investments, insurance, and wealth-building strategies. With a passion for simplifying complex financial topics, Nidhi helps readers make informed money decisions with confidence. She can be reached at [email protected]

Studycafe

Studycafe New Delhi, Delhi, India

New Delhi, Delhi, India 1833

1833My Recent Articles

- Karnataka High Court Gives Another Chance in GST Matter Due to Lack of Hearing

- Delay Should Be Condoned if Explanation is Unrefuted: ITAT

- Non-Service of Income Tax Notice, Ill health of taxpayer, ITAT condones Appeal filing delay

- Books of Accounts Cannot be Rejected Without Any Specific Defect: ITAT Kolkata

- Karnataka High Court Sends ITC Matter Back to GST Authorities for Reconsideration

Up Next

Loading suggestions…

Recent Posts

All Posts

Tags

Recent Posts

All Posts