ITAT Quashes Assessment for Exceeding Limited Scrutiny Scope and Ignoring Revised Return:

ITAT quashed the assessment as the AO exceeded the limited scrutiny scope and ignored a valid revised return.

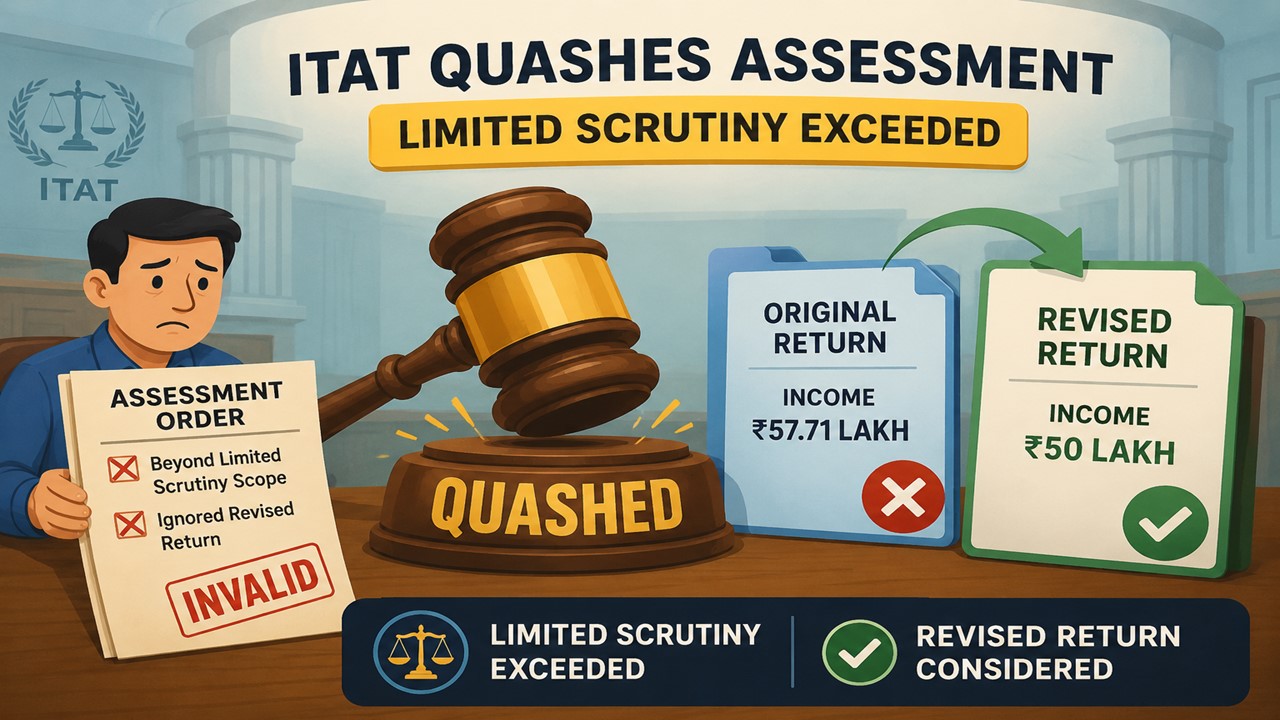

ITAT Quashes Assessment Beyond Limited Scrutiny Scope

ITAT Quashes Assessment for Exceeding Limited Scrutiny Scope and Ignoring Revised Return

The Delhi Bench of the Income Tax Appellate Tribunal (ITAT) has allowed the appeal of taxpayer Paluri Raghavan Gopala for Assessment Year 2015-16. The Tribunal held that the AO had gone beyond the scope of the issues for which the case was selected under "limited scrutiny" and had also ignored a valid revised return filed by the taxpayer.

The taxpayer’s case was initially picked up for limited scrutiny to verify the cash deposits in his bank account. However, during the course of assessment proceedings, the AO not only examined the cash deposits but also rejected the claim of exemption under Section 54F of the taxpayer and treated the capital gains arising from property transactions as business income. The taxpayer maintained that these issues were not the subject of the limited scrutiny notice.

The Tribunal on perusing the notice issued u/s 143(2) observed that the only issue stated therein for verification was cash deposits. The notice did not refer to property transactions or the claim for exemption under Section 54F. Therefore, the ITAT held that the AO had exceeded his jurisdiction by investigating and making additions on matters that were outside the scope of the limited scrutiny proceedings.

The Tribunal also addressed another important issue concerning the taxpayer’s amended return of income. The taxpayer filed the original return declaring income of Rs. 57,71,360 and then revised the return reducing the income to Rs 50 lakh. However, the AO while passing the assessment order has taken into consideration the income declared in original return and has completely ignored the revised return.

The Tribunal referring to the recent judgement of the Tripura High Court in Tripura State Electricity Corporation Ltd. v. PCIT (2025) held that if a valid revised return is filed, the original return would vanish and be substituted by the revised return. The assessment was made on the basis of original return and the revised return was not considered by the AO. Therefore, the assessment was bad.Since the AO had based his assessment on the original return and did not go into the revised return, the assessment was vitiated by a serious legal defect.

On the basis of these two findings, the ITAT accepted the additional grounds of appeal filed by the assessee, held the assessment unsustainable and deleted the additions made by the tax department, and as a result, the appeal filed by the assessee was allowed in full.

About Author

Vanshika verma

Content Writer

Vanshika Verma is a Content Writer with 1+ year of experience at Studycafe.in. A B.Com graduate from Delhi University, She writes articles on Finance, Tax, ICAI, GST, and the latest financial news, with a focus on making complex topics easy for readers and professionals.

Vanshika Verma is a Content Writer with 1+ year of experience at Studycafe.in. A B.Com graduate from Delhi University, She writes articles on Finance, Tax, ICAI, GST, and the latest financial news, with a focus on making complex topics easy for readers and professionals.

Studycafe

Studycafe Delhi, Delhi, India

Delhi, Delhi, India 1581

1581My Recent Articles

- Five Key Bills Likely To Be Introduced in Eighth Session of 18th Lok Sabha

- ITAT Upholds Rs 33.59 Lakh Bogus Derivative Loss Addition, Remands Reassessment Validity IssuePremium

- ITAT Remands Rs 1.31 Crore Tax Demand Case to AO for Fresh AssessmentPremium

- ITAT Grants Fresh Opportunity After Rejection of Section 12A and 80G ApplicationsPremium

- CBDT Notifies Income Tax Exemption to Baddi Barotiwala Nalagarh Development Authority

Up Next

Loading suggestions…

Recent Posts

All Posts

Tags

Recent Posts

All Posts