ITAT Restricts Bogus Purchase Addition to 8% Profit Element, Grants Major Relief to Taxpayer:

ITAT held that where corresponding sales are accepted, only the profit element embedded in alleged bogus purchases can be taxed, restricting the addition to 8% of the disputed purchases

ITAT Restricts Bogus Purchase Addition to 8%

ITAT Restricts Bogus Purchase Addition to 8% Profit Element, Grants Major Relief to Taxpayer

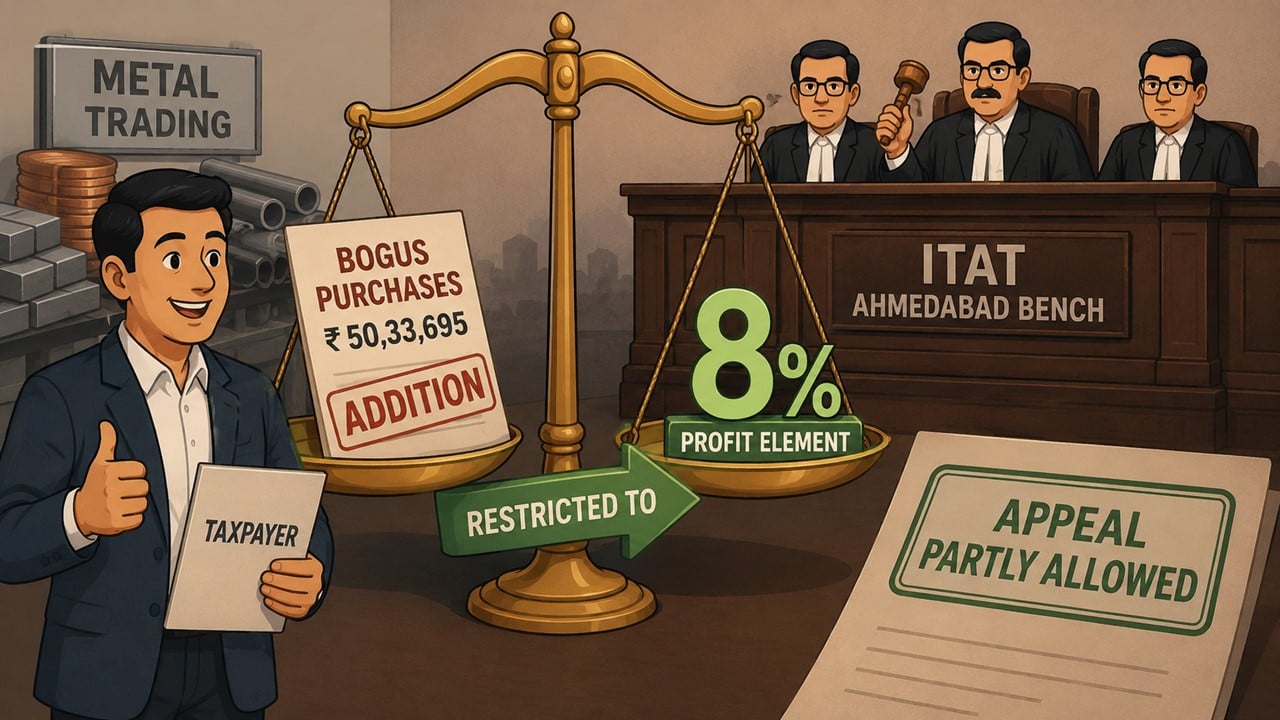

The Income Tax Appellate Tribunal (ITAT), Ahmedabad Bench, has provided huge relief to taxpayer Pruthvi Singh Solanki for Assessment Year 2018-19. The Tribunal partly allowed the appeal and reduced the addition of tax made by the Income Tax Department.

The taxpayer was engaged in the trade of ferrous and non-ferrous metals in the name of Vinay Enterprises. It had purchased goods worth Rs. 50,33,695 from five parties which were believed by the tax department to be bogus or accommodation entry providers. The assessment was re-opened on the basis of information received through Insight Portal of Income Tax Department.

During the assessment proceedings, the Assessing Officer (AO) noticed that the suppliers were only issuing fake bills and not actually supplying any goods. Accordingly, the AO treated the entire amount of purchase of Rs. 50,33,695 as bogus and added the same to the income of the assessee. The CIT(A) has also confirmed the addition.

However, the ITAT noted that the taxpayer was a trader and not a manufacturer. The Tribunal observed that the department had recorded and accepted the corresponding sales against these purchases. Sales, stock records or shortages in inventory were not contested. Therefore, it was unreasonable to assume that no purchases had been made at all.

The Tribunal explained that in such cases, the more likely situation is that the taxpayer may have purchased goods from the grey market at lower prices and obtained bills from suspected parties to reduce taxable profits. In such circumstances, only the profit element embedded in the alleged bogus purchases can be taxed, not the entire purchase value.

During the hearing, the taxpayer's representative agreed that an addition of 8% of the disputed purchases could be accepted as representing the suppressed profit element. The Department's representative also agreed that such an estimation was reasonable.

The ITAT accepted the decision of both parties and restricted the addition to 8% of Rs. 50,33,695 instead of the whole amount. The taxpayer was therefore entitled to substantial relief and the appeal was partly allowed.

About Author

Vanshika verma

Content Writer

Vanshika Verma is a Content Writer with 1+ year of experience at Studycafe.in. A B.Com graduate from Delhi University, She writes articles on Finance, Tax, ICAI, GST, and the latest financial news, with a focus on making complex topics easy for readers and professionals.

Vanshika Verma is a Content Writer with 1+ year of experience at Studycafe.in. A B.Com graduate from Delhi University, She writes articles on Finance, Tax, ICAI, GST, and the latest financial news, with a focus on making complex topics easy for readers and professionals.

Studycafe

Studycafe Delhi, Delhi, India

Delhi, Delhi, India 1581

1581My Recent Articles

- Five Key Bills Likely To Be Introduced in Eighth Session of 18th Lok Sabha

- ITAT Upholds Rs 33.59 Lakh Bogus Derivative Loss Addition, Remands Reassessment Validity IssuePremium

- ITAT Remands Rs 1.31 Crore Tax Demand Case to AO for Fresh AssessmentPremium

- ITAT Grants Fresh Opportunity After Rejection of Section 12A and 80G ApplicationsPremium

- CBDT Notifies Income Tax Exemption to Baddi Barotiwala Nalagarh Development Authority

Up Next

Loading suggestions…

Recent Posts

All Posts

Tags

Recent Posts

All Posts