List of Optional Entries made compulsory in Form GSTR-9 for FY 2021-22

List of Optional Entries made compulsory in Form GSTR-9 for FY 2021-22 This Article discusses List of entries in Form GSTR-9 (GST Annual Return) that…

List of Optional Entries made compulsory in Form GSTR-9 for FY 2021-22

This Article discusses List of entries in Form GSTR-9 (GST Annual Return) that were optional before FY 21-22 and have been made compulsory in Form GSTR-9 for FY 2021-22.

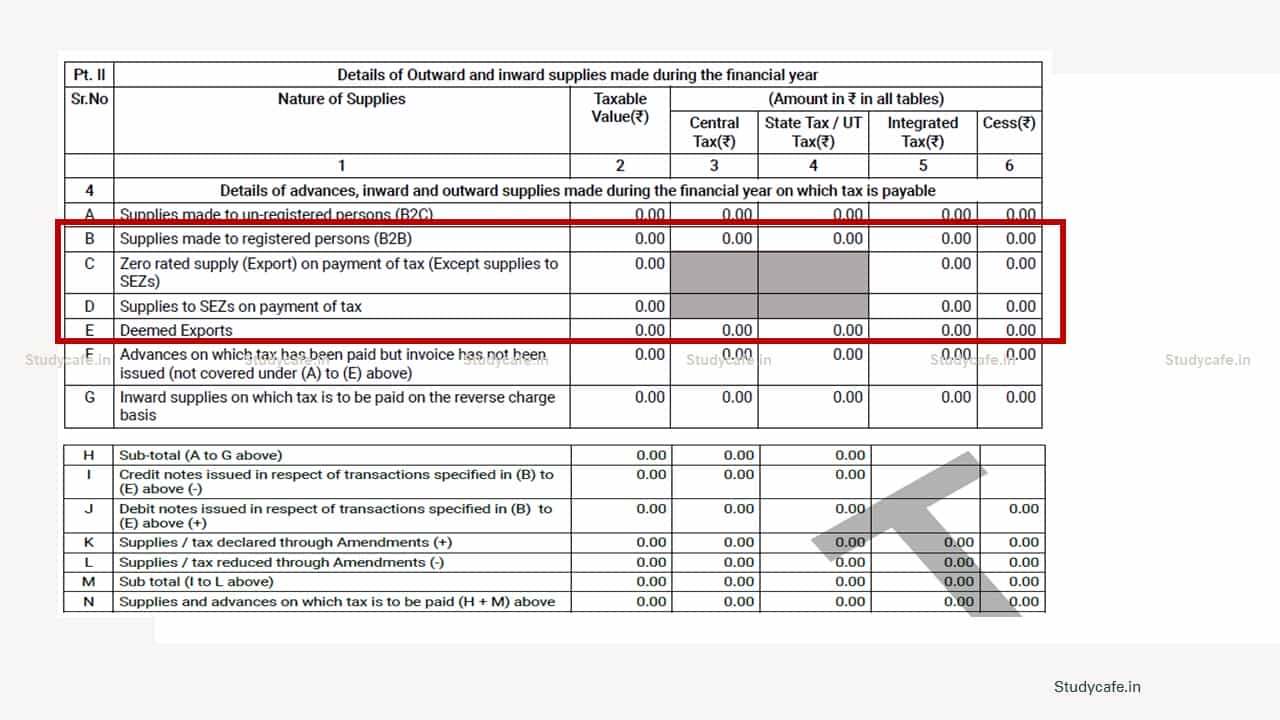

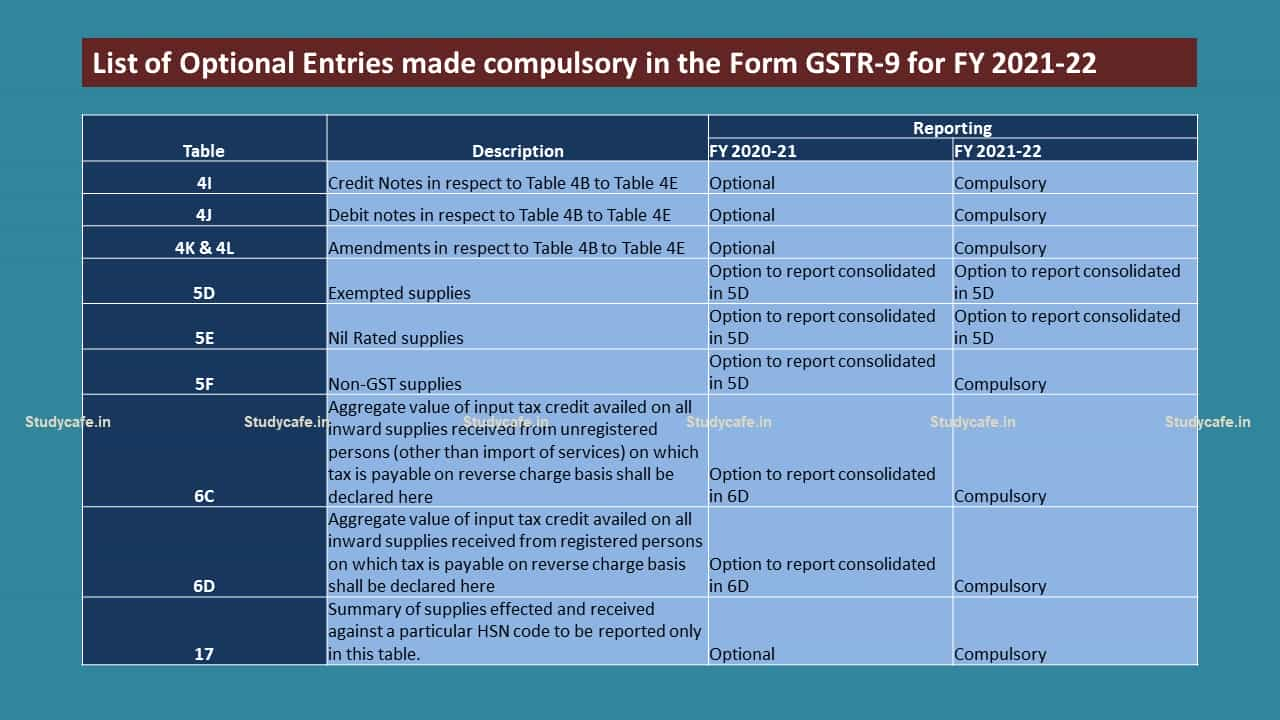

Table 4I to Table 4L

For FY 2017-18, 2018-19, 2019-20, and 2020-21 the registered person shall have the option to fill Table 4B to Table 4E net of Credit Notes (Table 4I), debit notes (Table 4J), and Amendments (4K & 4L) in case there is any difficulty in reporting such details separately in this Table.

These Tables have been made compulsory for FY 2021-22.

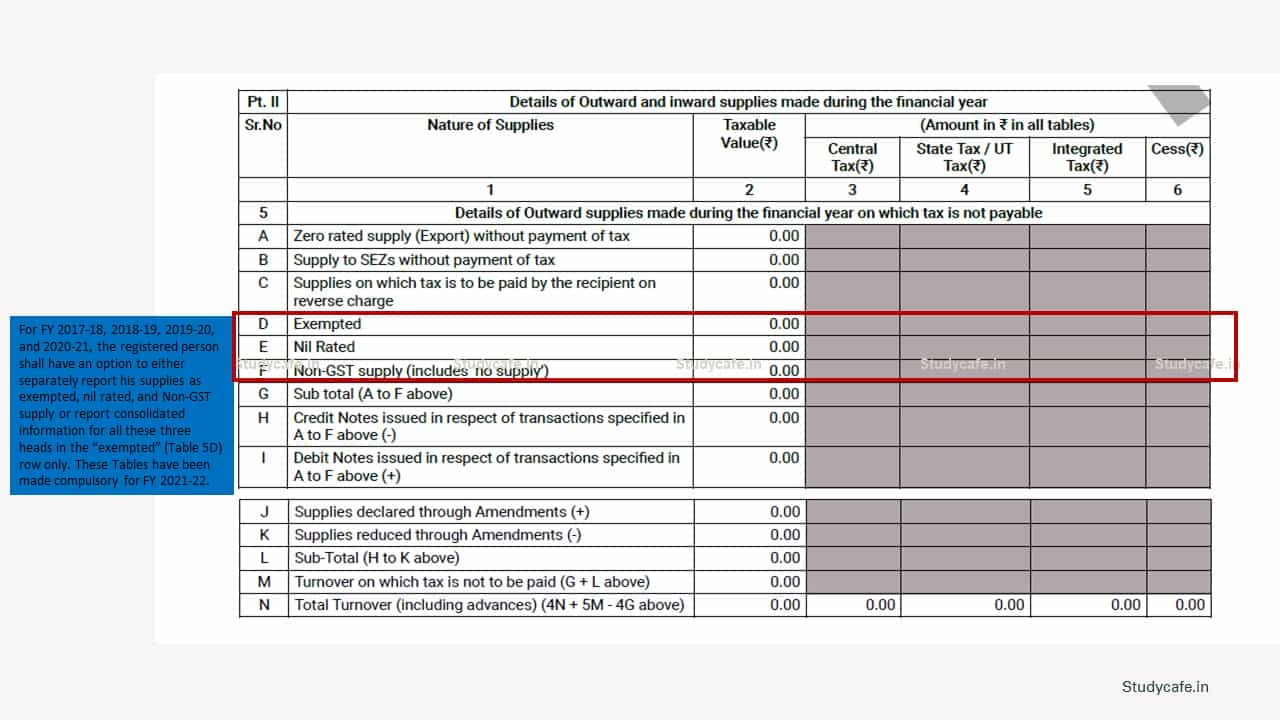

Table 5D, 5E and Table 5F

The aggregate value of exempted (Table 5D), Nil Rated (Table 5E) and Non-GST supplies (Table 5F) shall be declared here.

For FY 2017-18, 2018-19, 2019-20, and 2020-21, the registered person shall have an option to either separately report his supplies as exempted, nil rated, and Non-GST supply or report consolidated information for all these three heads in the “exempted” (Table 5D) row only.

For FY 2021-22, the value of “no supply” shall be declared under Non-GST supply (5F). Exempted and nil-rated supply can be reported respectively in Table 5D and Table 5E or consolidated reporting can be done in Table 5D.

Table 5D, 5E and Table 5F

The aggregate value of exempted (Table 5D), Nil Rated (Table 5E) and Non-GST supplies (Table 5F) shall be declared here.

For FY 2017-18, 2018-19, 2019-20, and 2020-21, the registered person shall have an option to either separately report his supplies as exempted, nil rated, and Non-GST supply or report consolidated information for all these three heads in the “exempted” (Table 5D) row only.

For FY 2021-22, the value of “no supply” shall be declared under Non-GST supply (5F). Exempted and nil-rated supply can be reported respectively in Table 5D and Table 5E or consolidated reporting can be done in Table 5D.

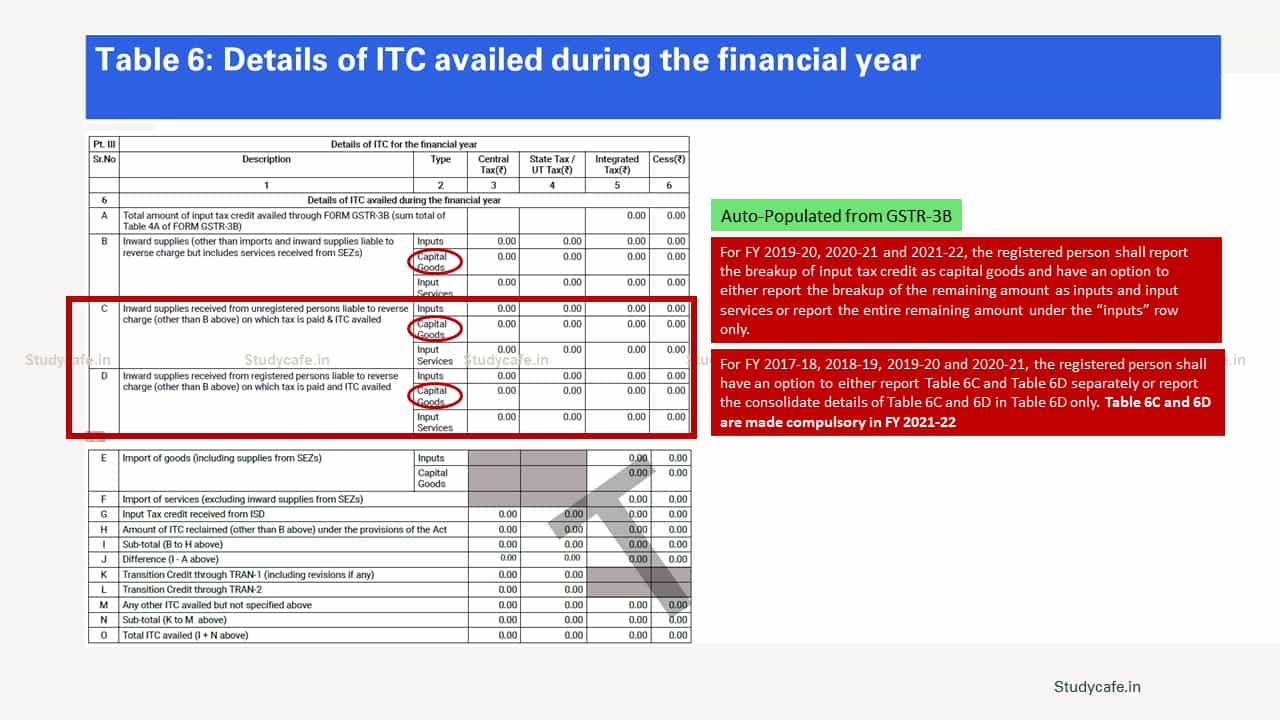

Details of Input Tax Credit

Tables 6B, 6C and 6C

For FY 2019-20, 2020-21 and 2021-22, the registered person shall report the breakup of input tax credit as capital goods and have an option to either report the breakup of the remaining amount as inputs and input services or report the entire remaining amount under the “inputs” row only.

For FY 2017-18, 2018-19, 2019-20 and 2020-21, the registered person shall have an option to either report Table 6C and Table 6D separately or report the consolidate details of Table 6C and 6D in Table 6D only. Table 6C and 6D are made compulsory in FY 2021-22.

Details of Input Tax Credit

Tables 6B, 6C and 6C

For FY 2019-20, 2020-21 and 2021-22, the registered person shall report the breakup of input tax credit as capital goods and have an option to either report the breakup of the remaining amount as inputs and input services or report the entire remaining amount under the “inputs” row only.

For FY 2017-18, 2018-19, 2019-20 and 2020-21, the registered person shall have an option to either report Table 6C and Table 6D separately or report the consolidate details of Table 6C and 6D in Table 6D only. Table 6C and 6D are made compulsory in FY 2021-22.

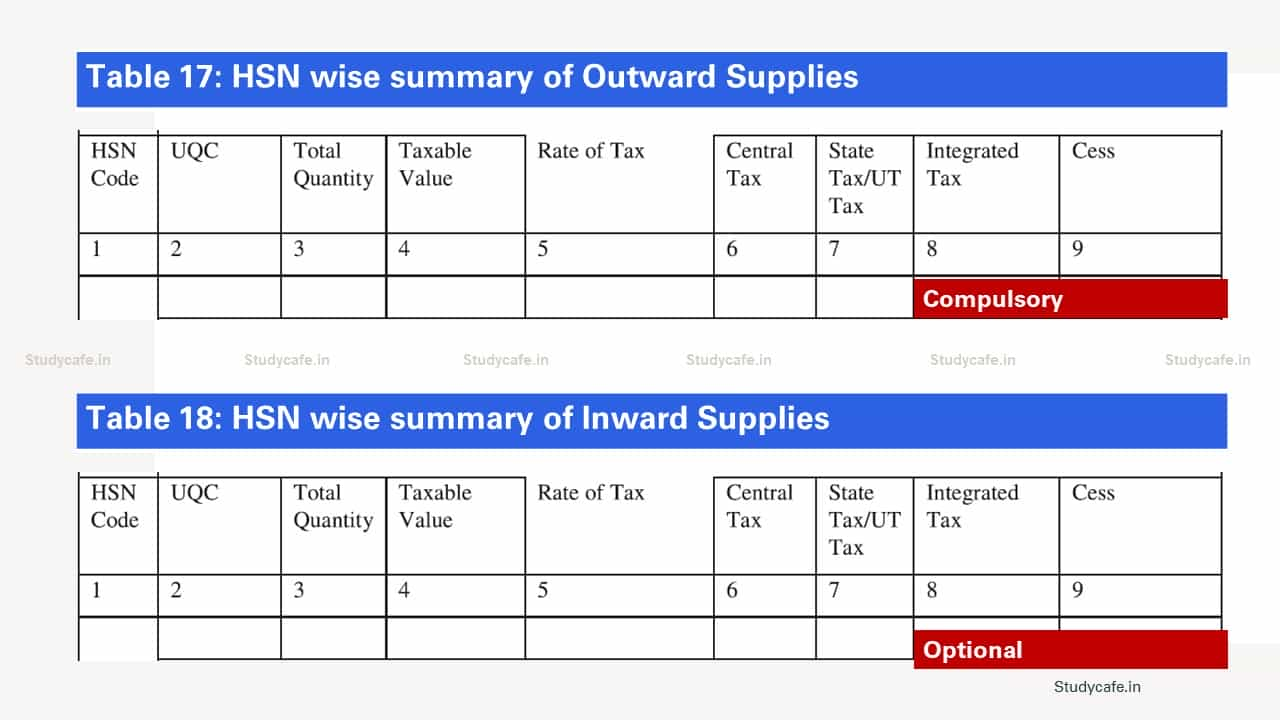

Table 17

Summary of supplies effected and received against a particular HSN code to be reported only in this table. This Table was optional for For FY 2017-18, 2018-19, 2019-20 and 2020-21. Same is made compulsory for FY 2021-22.

Table 17

Summary of supplies effected and received against a particular HSN code to be reported only in this table. This Table was optional for For FY 2017-18, 2018-19, 2019-20 and 2020-21. Same is made compulsory for FY 2021-22.

The Following is Summarised in below-mentioned Table:

The Following is Summarised in below-mentioned Table:

Benefits that are continuing:

Filing of Tables 5H to 5K is made optional.

Bifurcation of Input/Input Services/

Benefits that are continuing:

Filing of Tables 5H to 5K is made optional.

Bifurcation of Input/Input Services/ Capital Goods [Capital Goods to be reported from FY 2020-21] not required in ITC.

Reversals [Table 7A to Table 7H] can still be reported in a consolidated manner. However, reversals on account of TRAN-1 credit (Table 7F) and TRAN-2 (Table 7G) are to be mandatorily reported.

Filing of Tables 12, 13, 15, 16 & 18 is made optional.

Table 5D, 5E and Table 5F

The aggregate value of exempted (Table 5D), Nil Rated (Table 5E) and Non-GST supplies (Table 5F) shall be declared here.

For FY 2017-18, 2018-19, 2019-20, and 2020-21, the registered person shall have an option to either separately report his supplies as exempted, nil rated, and Non-GST supply or report consolidated information for all these three heads in the “exempted” (Table 5D) row only.

For FY 2021-22, the value of “no supply” shall be declared under Non-GST supply (5F). Exempted and nil-rated supply can be reported respectively in Table 5D and Table 5E or consolidated reporting can be done in Table 5D.

Details of Input Tax Credit

Tables 6B, 6C and 6C

For FY 2019-20, 2020-21 and 2021-22, the registered person shall report the breakup of input tax credit as capital goods and have an option to either report the breakup of the remaining amount as inputs and input services or report the entire remaining amount under the “inputs” row only.

For FY 2017-18, 2018-19, 2019-20 and 2020-21, the registered person shall have an option to either report Table 6C and Table 6D separately or report the consolidate details of Table 6C and 6D in Table 6D only. Table 6C and 6D are made compulsory in FY 2021-22.

Table 17

Summary of supplies effected and received against a particular HSN code to be reported only in this table. This Table was optional for For FY 2017-18, 2018-19, 2019-20 and 2020-21. Same is made compulsory for FY 2021-22.

The Following is Summarised in below-mentioned Table:

Benefits that are continuing:

Filing of Tables 5H to 5K is made optional.

Bifurcation of Input/Input Services/ About Author

CA Deepak Gupta

Co Founder

CA Deepak Gupta,is Co-founder of Studycafe. He is Microsoft Office Specialist and Corporate Trainer of AI Tools, Microsoft Excel.

He is Finance Influencer having more than 250K followers on Social Media. CA Deepak Gupta, is Having more than 14 plus years of experience, and he has Worked with best brands Like, Hero, Wipro, Ericsson before Starting Studycafe. He has Trained more than 20000 Persons in Microsoft Excel, PowerPoint, Power BI, Google Sheet, Google Forms and Other Tools.

CA Deepak Gupta,is Co-founder of Studycafe. He is Microsoft Office Specialist and Corporate Trainer of AI Tools, Microsoft Excel.

He is Finance Influencer having more than 250K followers on Social Media. CA Deepak Gupta, is Having more than 14 plus years of experience, and he has Worked with best brands Like, Hero, Wipro, Ericsson before Starting Studycafe. He has Trained more than 20000 Persons in Microsoft Excel, PowerPoint, Power BI, Google Sheet, Google Forms and Other Tools.

StudyCafe

StudyCafe Delhi, Delhi, India

Delhi, Delhi, India 3423

3423My Recent Articles

- UltraTech Cement slapped with Rs. 808.78 Cr Income Tax Demand

- GST: High Court upheld constitutional validity of Section 16(2)(c), asks government to address ITC issues of genuine purchasers

- Old vs New Tax Regime for Tax Year 2026-27

- High court criticizes Income Tax Department for not releasing ITR Utilities despite 11 years of directions

- Fino Payments Bank CEO Rishi Gupta Gets Bail in GST Case, Bank Clarifies No Direct Link

Up Next

Loading suggestions…

Recent Posts

All Posts

Recent Posts

All Posts