No DRC-01C Notice if ITC mismatch is less than 25L or 20% [Read GST Council Discussion]:

![No DRC-01C Notice if ITC mismatch is less than 25L or 20% [Read GST Council Discussion]](https://assets.studycafe.in/uploads/2023/12/No-DRC-01C-Notice-if-ITC-mismatch-is-less-than-25L-or-20.jpg)

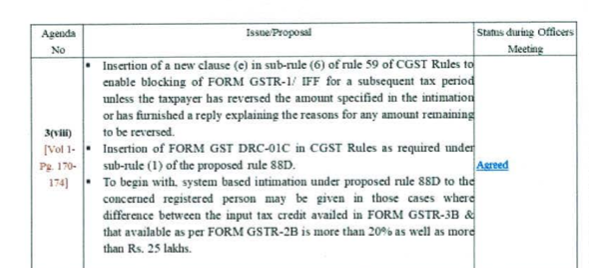

Proposed rule 88D may applied to cases where difference between ITC availed in GSTR-3B vs. GSTR-2B is more than 20% as well as more than Rs. 25 lakhs.

No DRC-01C Notice if ITC mismatch

No DRC-01C Notice if ITC mismatch is less than 25L or 20% [Read GST Council Discussion]

The Central Board of Indirect Taxes and Customs (CBIC) has notified rule 88D for Manner of dealing with difference in input tax credit available in auto-generated statement containing the details of input tax credit and that availed in return by the Central Goods and Services Tax (Second Amendment) Rules, 2023, w.e.f. 4-8-2023.

As per the rule, Where the amount of input tax credit availed by a registered person in the return for a tax period or periods furnished by him in FORM GSTR-3B exceeds the input tax credit available to such person in accordance with the auto-generated statement containing the details of input tax credit in FORM GSTR-2B in respect of the said tax period or periods, as the case may be, by such amount and such percentage, as may be recommended by the Council, the said registered person shall be intimated of such difference in Part A of FORM GST DRC-01C, electronically on the common portal, and a copy of such intimation shall also be sent to his e-mail address provided at the time of registration or as amended from time to time.

Decoding by such amount and such percentage

As per the minutes book of the 50th GST Council meeting, the system-based intimation under proposed rule 88D to the concerned registered person may be given in those cases where the difference between the input tax credit availed in FORM GSTR-3B & that available as per FORM GSTR-2B is more than 20% as well as more than Rs. 25 lakhs.

GST Portal is also following the above-mentioned limits. Please note that since the word 'Prescribed' has not been used in Rule 88D, which means that the limits need not be notified by a separate notification & a recommendation in the Council meeting would suffice.

On his Twitter account, CA Abhas Halakhandi has made these observations.

For Official GST Council Discussion Download PDF Given Below:

GST Portal is also following the above-mentioned limits. Please note that since the word 'Prescribed' has not been used in Rule 88D, which means that the limits need not be notified by a separate notification & a recommendation in the Council meeting would suffice.

On his Twitter account, CA Abhas Halakhandi has made these observations.

For Official GST Council Discussion Download PDF Given Below:

GST Portal is also following the above-mentioned limits. Please note that since the word 'Prescribed' has not been used in Rule 88D, which means that the limits need not be notified by a separate notification & a recommendation in the Council meeting would suffice.

On his Twitter account, CA Abhas Halakhandi has made these observations.

For Official GST Council Discussion Download PDF Given Below:About Author

CA Pratibha Goyal

Co Founder

CA Pratibha Goyal is Chartered Accountant qualified in 2016, is a Member of The Institute of Chartered Accountants of India having wide experience in the field of Auditing, Taxation, ROC, GST and Secretarial matters etc.

She has written over a thousand articles & has made several videos on topics related to Auditing & Taxation. As a Speaker she has delivered various sessions on various branches of NIRC of ICAI.

CA Pratibha Goyal is Chartered Accountant qualified in 2016, is a Member of The Institute of Chartered Accountants of India having wide experience in the field of Auditing, Taxation, ROC, GST and Secretarial matters etc.

She has written over a thousand articles & has made several videos on topics related to Auditing & Taxation. As a Speaker she has delivered various sessions on various branches of NIRC of ICAI.

Studycafe

Studycafe New Delhi, Delhi, India

New Delhi, Delhi, India 1486

1486My Recent Articles

- Biggest Labour Reform in Indian History: 4 Labour Codes Effective from today

- Tax Audit and ITR Due date not extended in this case: Know More

- Government notifies Agreement and Protocol between India and Qatar [Read Notification]

- CA Breaking: Results of ICAI Examination to be announced soon, Know probable Date

- Breaking: GSTR-3B Due Date for September 2025 extended by CBIC amid Diwali Festivities

Up Next

Loading suggestions…

Recent Posts

All Posts

Recent Posts

All Posts