Notice for Discrepancies in GST Returns - GST ASMT-10

Notice for Discrepancies in GST Returns - GST ASMT-10 These days a large number of taxpayers are getting GST Return Discrepancy notices in the form o…

Notice for Discrepancies in GST Returns - GST ASMT-10

These days a large number of taxpayers are getting GST Return Discrepancy notices in the form of GST ASMT-10. Through this article, I have tried summarising all about the relevant provisions related to this Form.

Form GST ASMT-10

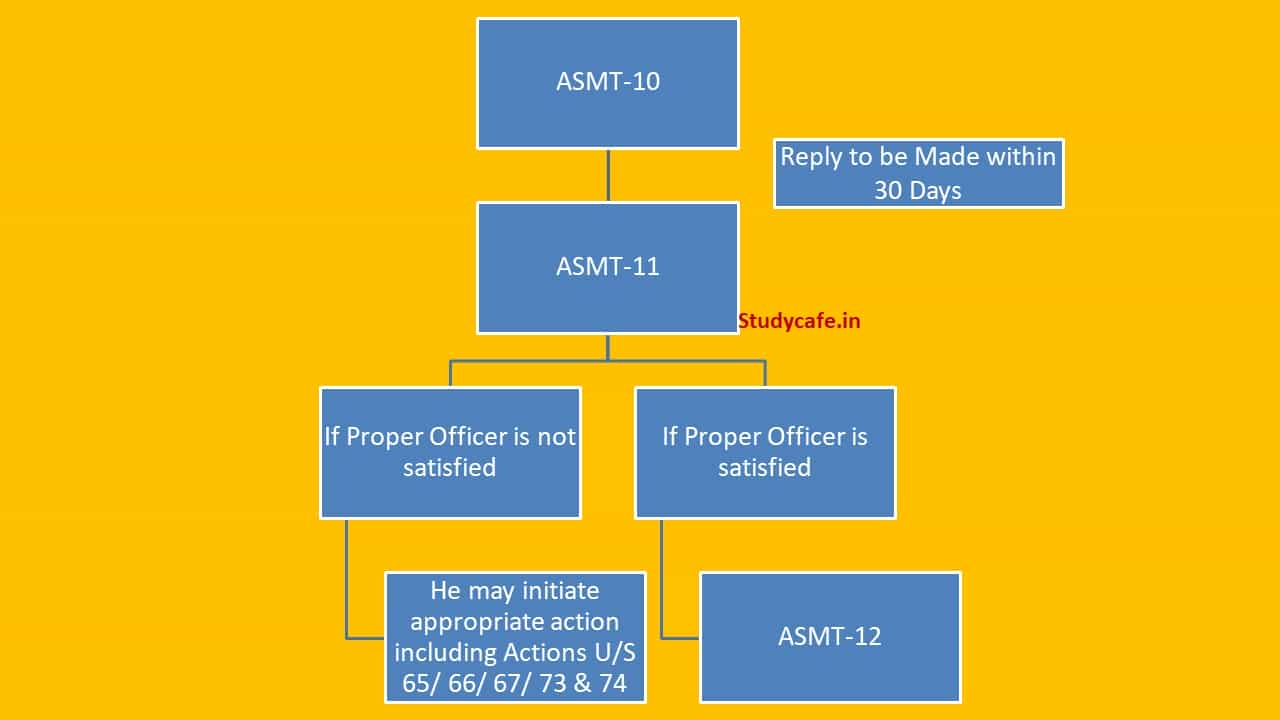

What is Proper Officer is Satisfied with the Explanation of Taxpayer?

If Proper Officer is Satisfied with the Explanation of Taxpayer, he shall him accordingly in FORM GST ASMT-12.

What if Proper Officer is not satisfied with the Explanation of the Taxpayer?

If the proper officer is not satisfied with the Explanation of the Taxpayer he may initiate appropriate action including those under:

Section 65: Audit by tax authorities

Section 66: Special audit

Section 67: Inspection, search and seizure

Section 73: Determination of tax not paid or short paid or erroneously refunded or input tax credit wrongly availed or utilized for any reason other than fraud or any wilful misstatement or suppression of facts

Section 74: Determination of tax not paid or short paid or erroneously refunded or input tax credit wrongly availed or utilized by reason of fraud or any wilful-misstatement or suppression of facts.

What is Proper Officer is Satisfied with the Explanation of Taxpayer?

If Proper Officer is Satisfied with the Explanation of Taxpayer, he shall him accordingly in FORM GST ASMT-12.

What if Proper Officer is not satisfied with the Explanation of the Taxpayer?

If the proper officer is not satisfied with the Explanation of the Taxpayer he may initiate appropriate action including those under:

Section 65: Audit by tax authorities

Section 66: Special audit

Section 67: Inspection, search and seizure

Section 73: Determination of tax not paid or short paid or erroneously refunded or input tax credit wrongly availed or utilized for any reason other than fraud or any wilful misstatement or suppression of facts

Section 74: Determination of tax not paid or short paid or erroneously refunded or input tax credit wrongly availed or utilized by reason of fraud or any wilful-misstatement or suppression of facts.

What if Taxpayer has admitted his liability in Form FORM GST ASMT-10 and he fails to pay the same?

If the Taxpayer has admitted his liability in Form FORM GST ASMT-10 and he fails to pay the same, Proper Officer may initiate appropriate action including those under:

Section 65: Audit by tax authorities

Section 66: Special audit

Section 67: Inspection, search and seizure

Section 73: Determination of tax not paid or short paid or erroneously refunded or input tax credit wrongly availed or utilized for any reason other than fraud or any wilful misstatement or suppression of facts

Section 74: Determination of tax not paid or short paid or erroneously refunded or input tax credit wrongly availed or utilized by reason of fraud or any wilful-misstatement or suppression of facts.

How can I View Notice GST ASMT-10?

What if Taxpayer has admitted his liability in Form FORM GST ASMT-10 and he fails to pay the same?

If the Taxpayer has admitted his liability in Form FORM GST ASMT-10 and he fails to pay the same, Proper Officer may initiate appropriate action including those under:

Section 65: Audit by tax authorities

Section 66: Special audit

Section 67: Inspection, search and seizure

Section 73: Determination of tax not paid or short paid or erroneously refunded or input tax credit wrongly availed or utilized for any reason other than fraud or any wilful misstatement or suppression of facts

Section 74: Determination of tax not paid or short paid or erroneously refunded or input tax credit wrongly availed or utilized by reason of fraud or any wilful-misstatement or suppression of facts.

How can I View Notice GST ASMT-10?

- Form GST ASMT-10 is a Notice for intimating discrepancies in the return after scrutiny. [Section 61 & Rule 99]

- Proper Officer is required to quantify the amount of tax, interest, and any other amount payable in relation to such discrepancy if possible.

- Some of the common examples of discrepancies for which notice can be issued are:

- Difference between the tax liability reported in GSTR- 1 & GSTR -3B

- Difference between the ITC Claimed in GSTR- 3B & reflected in GSTR -2B/GSTR-2A

- Difference between the tax liability as per E-Way Bill & GSTR -3B

- The taxpayer is required to provide an explanation for such discrepancy within thirty days from the date of service of the notice.

- The additional period may be permitted by Proper Officer on request of the Taxpayer.

What is Proper Officer is Satisfied with the Explanation of Taxpayer?

If Proper Officer is Satisfied with the Explanation of Taxpayer, he shall him accordingly in FORM GST ASMT-12.

What if Proper Officer is not satisfied with the Explanation of the Taxpayer?

If the proper officer is not satisfied with the Explanation of the Taxpayer he may initiate appropriate action including those under:

Section 65: Audit by tax authorities

Section 66: Special audit

Section 67: Inspection, search and seizure

Section 73: Determination of tax not paid or short paid or erroneously refunded or input tax credit wrongly availed or utilized for any reason other than fraud or any wilful misstatement or suppression of facts

Section 74: Determination of tax not paid or short paid or erroneously refunded or input tax credit wrongly availed or utilized by reason of fraud or any wilful-misstatement or suppression of facts.

What if Taxpayer has admitted his liability in Form FORM GST ASMT-10 and he fails to pay the same?

If the Taxpayer has admitted his liability in Form FORM GST ASMT-10 and he fails to pay the same, Proper Officer may initiate appropriate action including those under:

Section 65: Audit by tax authorities

Section 66: Special audit

Section 67: Inspection, search and seizure

Section 73: Determination of tax not paid or short paid or erroneously refunded or input tax credit wrongly availed or utilized for any reason other than fraud or any wilful misstatement or suppression of facts

Section 74: Determination of tax not paid or short paid or erroneously refunded or input tax credit wrongly availed or utilized by reason of fraud or any wilful-misstatement or suppression of facts.

How can I View Notice GST ASMT-10?

- Login to www.gst.gov.in

- Navigate to Dashboard

- Navigate to Services & User Services

- Click on View Additional Notices/Orders option.

About Author

CA Pratibha Goyal

Co Founder

CA Pratibha Goyal is Chartered Accountant qualified in 2016, is a Member of The Institute of Chartered Accountants of India having wide experience in the field of Auditing, Taxation, ROC, GST and Secretarial matters etc.

She has written over a thousand articles & has made several videos on topics related to Auditing & Taxation. As a Speaker she has delivered various sessions on various branches of NIRC of ICAI.

CA Pratibha Goyal is Chartered Accountant qualified in 2016, is a Member of The Institute of Chartered Accountants of India having wide experience in the field of Auditing, Taxation, ROC, GST and Secretarial matters etc.

She has written over a thousand articles & has made several videos on topics related to Auditing & Taxation. As a Speaker she has delivered various sessions on various branches of NIRC of ICAI.

Studycafe

Studycafe New Delhi, Delhi, India

New Delhi, Delhi, India 1486

1486My Recent Articles

- Biggest Labour Reform in Indian History: 4 Labour Codes Effective from today

- Tax Audit and ITR Due date not extended in this case: Know More

- Government notifies Agreement and Protocol between India and Qatar [Read Notification]

- CA Breaking: Results of ICAI Examination to be announced soon, Know probable Date

- Breaking: GSTR-3B Due Date for September 2025 extended by CBIC amid Diwali Festivities

Up Next

Loading suggestions…

Recent Posts

All Posts

Recent Posts

All Posts