Presumptive taxation Scheme for non-resident providing services for electronics manufacturing facility [Budget 2025]:

![Presumptive taxation Scheme for non-resident providing services for electronics manufacturing facility [Budget 2025]](https://assets.studycafe.in/uploads/2025/02/PRESUMPTIVE-TAXATION-SCHEME-For-NR-1.jpg)

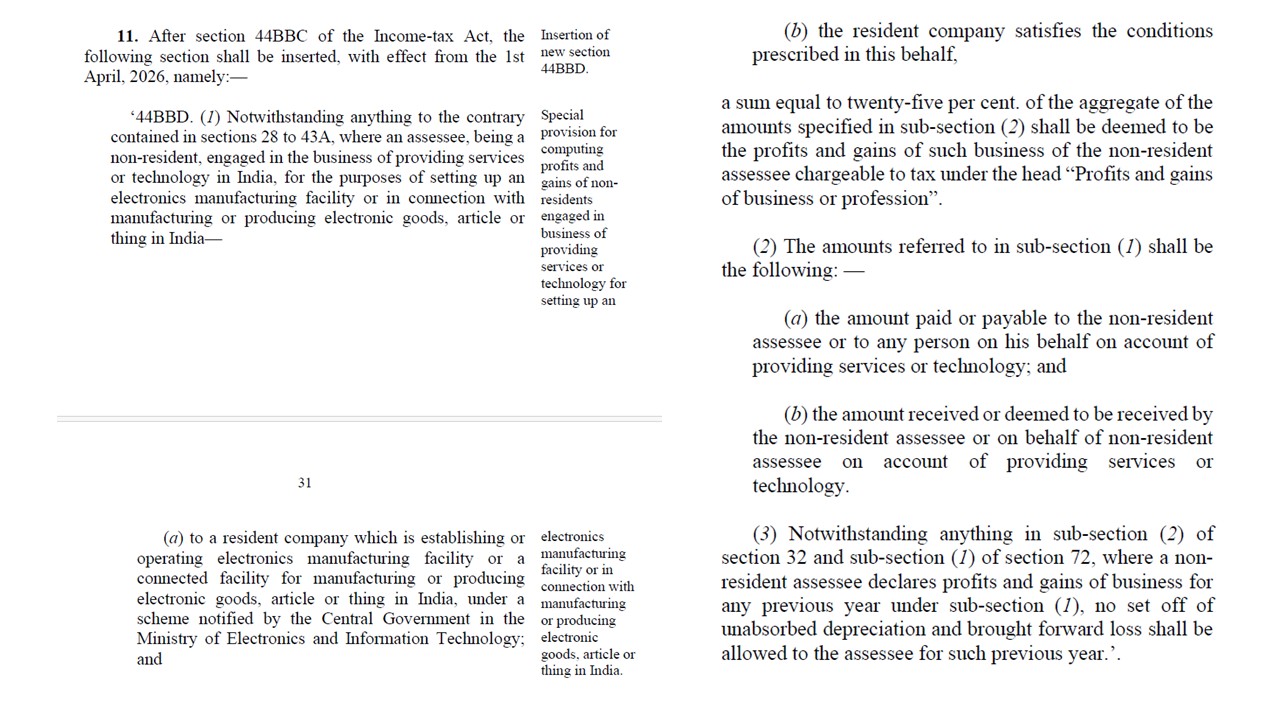

All about Presumptive taxation Scheme for non-resident providing services for electronics manufacturing facility as announced by Budget 2025

Presumptive taxation Scheme for Non-Resident

Presumptive taxation Scheme for non-resident providing services for electronics manufacturing facility [Budget 2025]

In order to position India as the global hub for Electronics System Design and Manufacturing, a comprehensive program for the development of semiconductors and display manufacturing ecosystem in India was approved by Government of India. Ministry of Electronics and Information Technology has notified Schemes for setting up of such facilities in India.

In Budget 2025 Speech, Finance Minister said "It is proposed to provide a presumptive taxation regime for non-residents who provide services to a resident company that is establishing or operating an electronics manufacturing facility. I further propose to introduce a safe harbour for tax certainty for non-residents who store components for supply to specified electronics manufacturing units."

In this context, it has been represented that non-residents will be providing support in setting up of such electronics manufacturing facilities by deploying the technology and providing support services.

In order to ensure certainty and promotion of this industry, it is proposed to provide a presumptive taxation regime for non-residents engaged in the business of providing services or technology, to a resident company which are establishing or operating electronics manufacturing facility or a connected facility for manufacturing or producing electronic goods, article or thing in India, under a scheme notified by the Central Government in the Ministry of Electronics and Information Technology and satisfies such conditions as prescribed in the rules.

It is, therefore, proposed, to insert a new section 44BBD, which deems twenty-five per cent of the aggregate amount received/ receivable by, or paid/ payable to, the non-resident, on account of providing services or technology, as profits and gains of such non-resident from this business. This will result in an effective tax payable of less than 10% on gross receipts, by a non-resident company.

This amendment will take effect from the 1st day of April, 2026 and shall accordingly, apply in relation to the assessment year 2026-27 and subsequent assessment years.

This amendment will take effect from the 1st day of April, 2026 and shall accordingly, apply in relation to the assessment year 2026-27 and subsequent assessment years.

This amendment will take effect from the 1st day of April, 2026 and shall accordingly, apply in relation to the assessment year 2026-27 and subsequent assessment years.About Author

CA Pratibha Goyal

Co Founder

CA Pratibha Goyal is Chartered Accountant qualified in 2016, is a Member of The Institute of Chartered Accountants of India having wide experience in the field of Auditing, Taxation, ROC, GST and Secretarial matters etc.

She has written over a thousand articles & has made several videos on topics related to Auditing & Taxation. As a Speaker she has delivered various sessions on various branches of NIRC of ICAI.

CA Pratibha Goyal is Chartered Accountant qualified in 2016, is a Member of The Institute of Chartered Accountants of India having wide experience in the field of Auditing, Taxation, ROC, GST and Secretarial matters etc.

She has written over a thousand articles & has made several videos on topics related to Auditing & Taxation. As a Speaker she has delivered various sessions on various branches of NIRC of ICAI.

Studycafe

Studycafe New Delhi, Delhi, India

New Delhi, Delhi, India 1486

1486My Recent Articles

- Biggest Labour Reform in Indian History: 4 Labour Codes Effective from today

- Tax Audit and ITR Due date not extended in this case: Know More

- Government notifies Agreement and Protocol between India and Qatar [Read Notification]

- CA Breaking: Results of ICAI Examination to be announced soon, Know probable Date

- Breaking: GSTR-3B Due Date for September 2025 extended by CBIC amid Diwali Festivities

Up Next

Loading suggestions…

Recent Posts

All Posts

Tags

No tags yet.

Recent Posts

All Posts

Tags

No tags yet.