SABKA VISHWAS DISPUTE RESOLUTION SCHEME, 2019

SABKA VISHWAS DISPUTE RESOLUTION SCHEME, 2019 What are the Objectives of this Scheme 1.) The Scheme is a one time measure for liquidation of

SABKA VISHWAS DISPUTE RESOLUTION SCHEME, 2019

What are the Objectives of this Scheme

1.) The Scheme is a one time measure for liquidation of past disputes of Central Excise, Service Tax and 26 other indirect tax enactments.

2.) The Scheme provides that eligible persons shall declare the unpaid tax dues and pay the same in accordance with the provisions of the Scheme.

3.) The Scheme provides for certain immunities including penalty interest or any other proceedings including prosecution to those persons who pay the declared tax Dues.

Some of the Facts About this Scheme

This Scheme shall be called the Sabka Vishwas (Legal Dispute Resolution) Scheme, 2019.

It shall come into force on such date when notified in the Official Gazette.

Declaration related to excisable goods set forth in the Fourth Schedule (Chapter 24 and 27) to the Central Excise Act, 1944 are not included under the Scheme.

Scheme is applicable to the Central Excise Act 1944 or the Central Excise Tariff Act, 1985 or Chapter V of the Finance Act, 1994 and 26 other Acts and the Rules made thereunder.

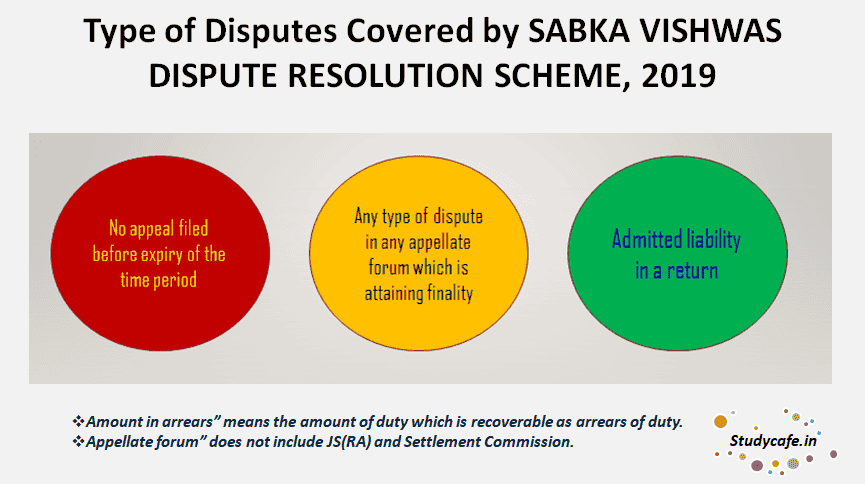

What are the Type of Disputes Covered by SABKA VISHWAS DISPUTE RESOLUTION SCHEME, 2019

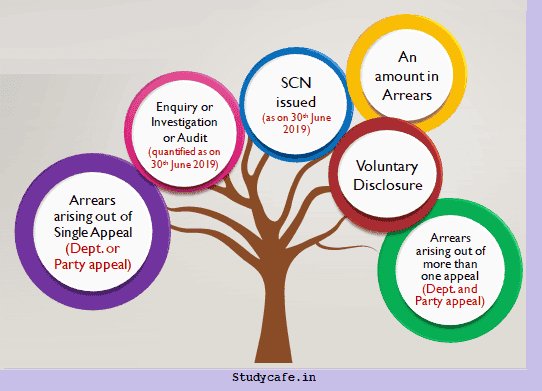

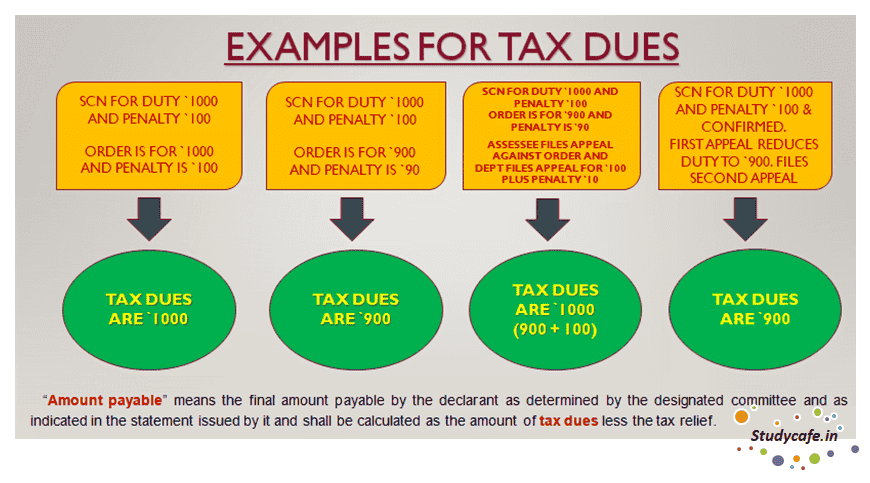

What is meaning of Tax Dues as per SABKA VISHWAS DISPUTE RESOLUTION SCHEME, 2019

Quanified means a written communication of the amount of duty payable under the indirect tax enactment.

Audit means any verification and checks and will commence when a written intimation from the Central Excise officer regarding conducting of Audit is received.

Enquiry or investigation, under any of the indirect tax enactments, shall include the following actions, namely (i) search of premises; (ii) issuance of summon (iii) Letters asking for production of accounts, documents or other evidence (iv) recording of statements.

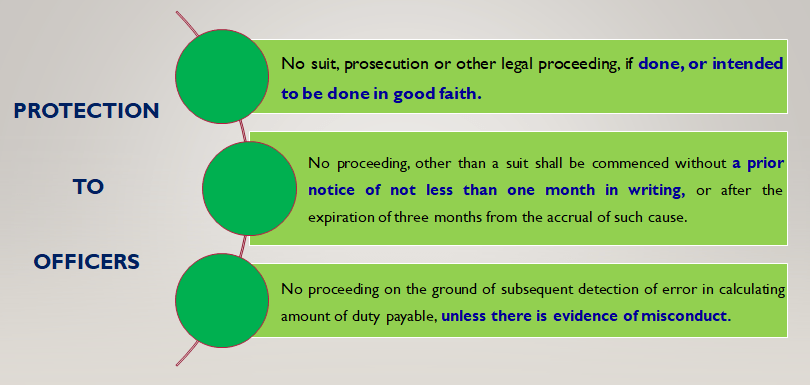

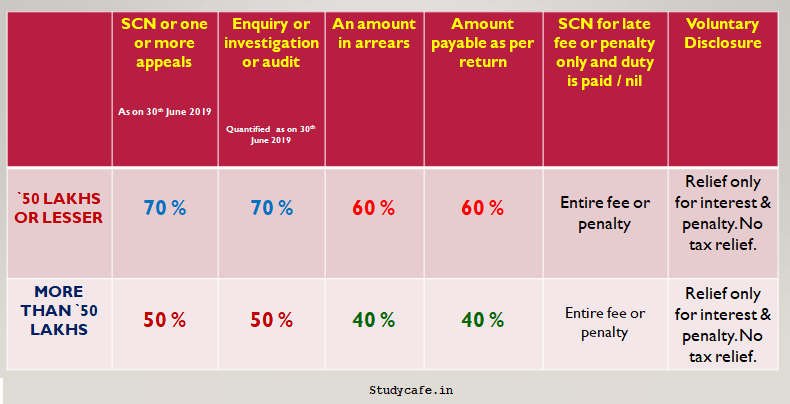

What are the Reliefs available under this scheme

What are PRECONDITIONS and restrictions for Availing this scheme

| PRECONDITIONS: | RESTRICTIONS OF THE SCHEME : |

| The relief calculated shall be subject to the condition that any amount paid as pre-deposit shall be deducted when issuing the statement indicating the amount payable by the declarant. Provided that if the amount of predeposit or deposit already paid > the amount payable the declarant shall not be entitled to any refund. |

(a) Shall not be paid through the input tax credit account. (b) Shall not be taken as input tax credit; or entitle any person to take input tax credit, as a recipient, of the excisable goods or taxable services. (c) Shall not be refundable under any circumstances. |

Who are Not eligible to make a declaration under this scheme

Excisable goods from Fourth Schedule to the Central Excise Act, 1944

Application in the Settlement Commission

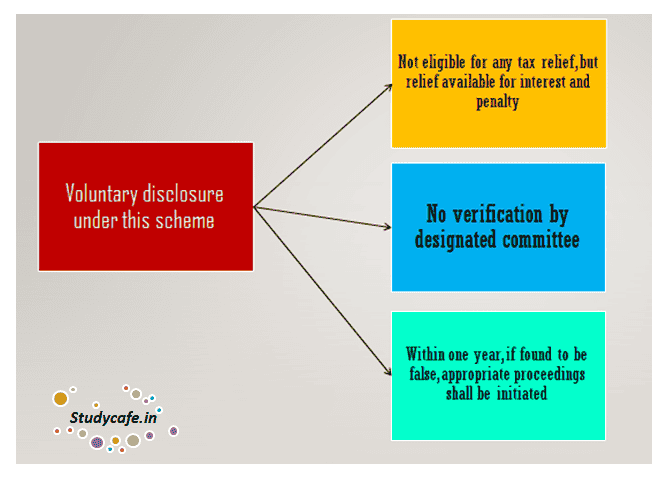

Voluntary Disclosure after being subjected to any enquiry commission investigation or audit & filed a return, indicating duty as payable, but has not paid it

Subjected to enquiry or investigation or audit and duty involved has not been quantified on or before 30th June 2019.

Appeal before appellate forum and heard finally on or before 30th June 2019

Convicted for any offence for the matter for which he he intends to file a declaration.

Issued a SCN and final hearing has taken place on or before 30th June 2019

Issued a SCN for erroneous refund or refund

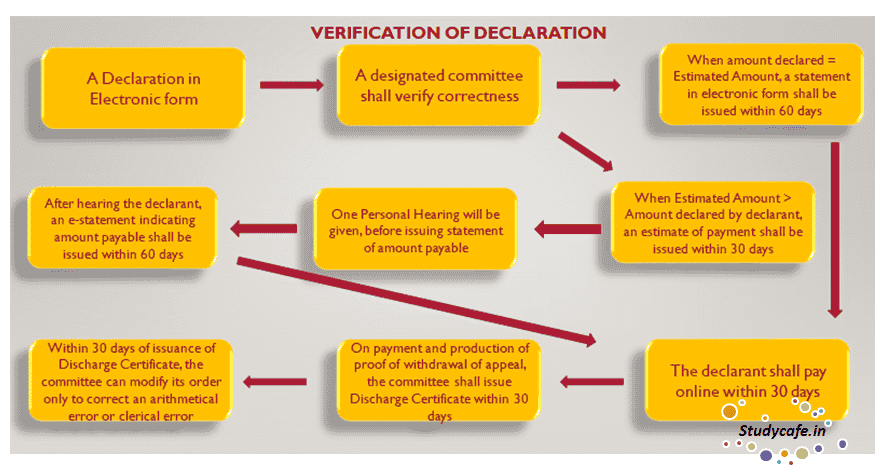

AFTER ISSUANCE OF DISCHARGE CERTIFICATE

a) Not be liable to pay any further duty, interest, or penalty with respect to the matter and the time period covered.

b) Not be liable to be prosecuted under the Indirect Tax enactment.

c) Shall not be reopened in any other proceeding under the Indirect Tax enactment.

d) If false declaration is made in voluntary disclosure, proceedings under the applicable laws shall be started within a time-limit of one year.

Click Here to Buy CA Final Pendrive Classes at Discounted Rate

About Author

CA Pratibha Goyal

Co Founder

Studycafe

Studycafe New Delhi, Delhi, India

New Delhi, Delhi, India 1486

1486My Recent Articles

- Biggest Labour Reform in Indian History: 4 Labour Codes Effective from today

- Tax Audit and ITR Due date not extended in this case: Know More

- Government notifies Agreement and Protocol between India and Qatar [Read Notification]

- CA Breaking: Results of ICAI Examination to be announced soon, Know probable Date

- Breaking: GSTR-3B Due Date for September 2025 extended by CBIC amid Diwali Festivities

Loading suggestions…

Recent Posts

All Posts

Tags

No tags yet.

Recent Posts

All Posts

Tags

No tags yet.