Sub-contracting for a service is not an intermediary service: CBIC

Sub-contracting for a service is not an intermediary service: CBIC Central Board of Indirect Taxes and Customs has issued a circular in which they ha…

Table of Contents

Sub-contracting for a service is not an intermediary service: CBIC

Central Board of Indirect Taxes and Customs has issued a circular in which they have clarified doubts related to scope of “Intermediary”.

The concept of ‘intermediary’ was borrowed in GST from the Service Tax Regime. The definition of ‘intermediary’ in the Service Tax law as given in Rule 2(f) of Place of Provision of Services Rules, 2012 issued vide notification No. 28/2012-ST, dated 20-6-2012.

The concept of intermediary services, as defined above, requires some basic pre-requisites, which are discussed below:

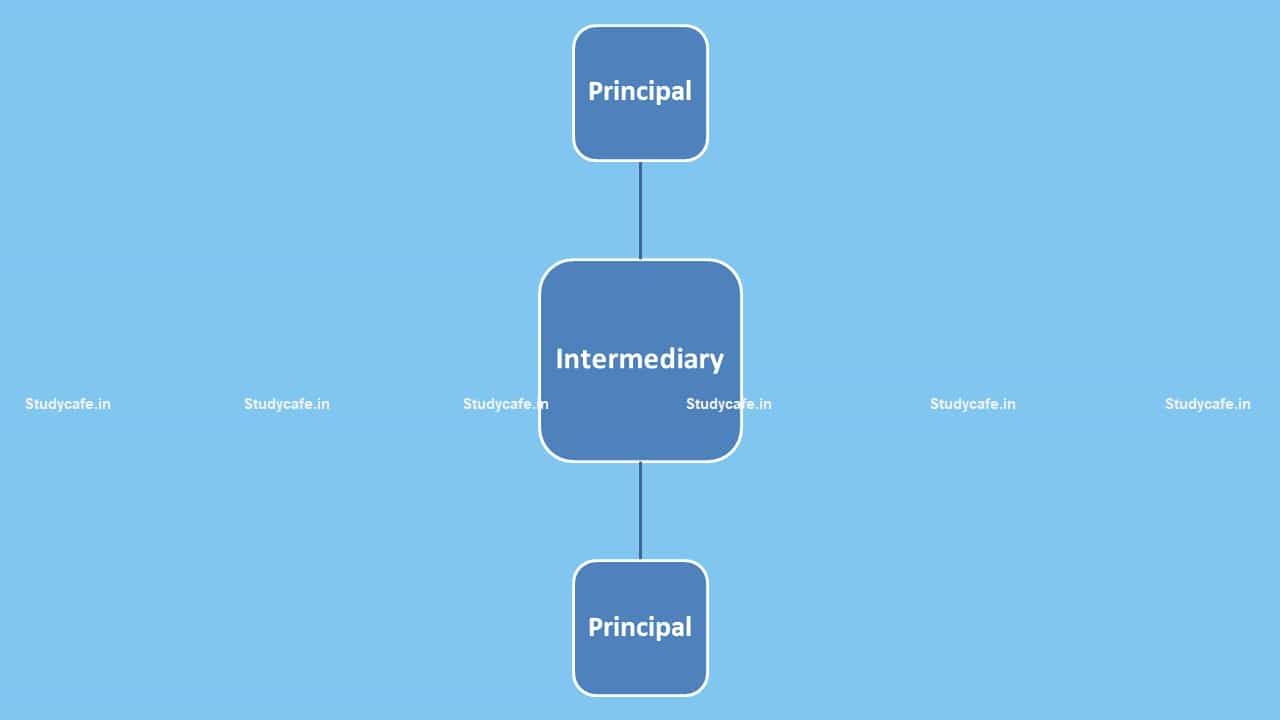

- Minimum of Three Parties

- It usually has two distinct supplies wherein main supply is between 2 principals and their is Ancillary supply, which is the service of facilitating or arranging the main supply.

- Intermediary service provider to have the character of an agent, broker or any other similar person

- It does not include a person who supplies such goods or services or both or securities on his own account

- Sub-contracting for a service is not an intermediary service

About Author

CA Deepak Gupta

Co Founder

CA Deepak Gupta,is Co-founder of Studycafe. He is Microsoft Office Specialist and Corporate Trainer of AI Tools, Microsoft Excel.

He is Finance Influencer having more than 250K followers on Social Media. CA Deepak Gupta, is Having more than 14 plus years of experience, and he has Worked with best brands Like, Hero, Wipro, Ericsson before Starting Studycafe. He has Trained more than 20000 Persons in Microsoft Excel, PowerPoint, Power BI, Google Sheet, Google Forms and Other Tools.

CA Deepak Gupta,is Co-founder of Studycafe. He is Microsoft Office Specialist and Corporate Trainer of AI Tools, Microsoft Excel.

He is Finance Influencer having more than 250K followers on Social Media. CA Deepak Gupta, is Having more than 14 plus years of experience, and he has Worked with best brands Like, Hero, Wipro, Ericsson before Starting Studycafe. He has Trained more than 20000 Persons in Microsoft Excel, PowerPoint, Power BI, Google Sheet, Google Forms and Other Tools.

StudyCafe

StudyCafe Delhi, Delhi, India

Delhi, Delhi, India 3423

3423My Recent Articles

- UltraTech Cement slapped with Rs. 808.78 Cr Income Tax Demand

- GST: High Court upheld constitutional validity of Section 16(2)(c), asks government to address ITC issues of genuine purchasers

- Old vs New Tax Regime for Tax Year 2026-27

- High court criticizes Income Tax Department for not releasing ITR Utilities despite 11 years of directions

- Fino Payments Bank CEO Rishi Gupta Gets Bail in GST Case, Bank Clarifies No Direct Link

Up Next

Loading suggestions…

Recent Posts

All Posts

Recent Posts

All Posts