Summary of Changes notified by GST Notification No. 37/2023- Central Tax dated 04-Aug-23

Summary of Changes notified by GST Notification No. 37/2023- Central Tax dated 04-Aug-23 Rule 9: Verification of the application and approval Rule 9 …

Summary of Changes notified by GST Notification No. 37/2023- Central Tax dated 04-Aug-23

Rule 9: Verification of the application and approval

Rule 9 is amended so as to enable GST officer to do Physical verification in Absence of person who has applied for registration

Rule 10A: Furnishing of Bank Account Details

Rule has been amended to make it compulsory to provide Bank Statement for Registered person within a period of 30 days from the date of GSTN, or before furnishing Form GSTR-1 or using invoice furnishing facility, whichever is earlier.

Rule 21A: Suspension of registration

Rule 21A has been amended so as to enhance the scope of "Suspension of Registration" where there is a contravention of the provisions of rule 10A [Non-Submission of Bank Statement]. Earlier only mismatch in GST Return [GSTR-3B, GSTR-1 and GSTR-2B] was covered for "Suspension of Registration".

Rule 25: Physical verification of business premises in certain cases

Rule 25 has been amended to provide for physical verification in high risk cases even where Aadhaar has been authenticated.

Rule 43: Manner of determination of input tax credit in respect of capital goods and reversal thereof in certain cases

Explanation has been inserted after rule 43 of CGST Rules, 2017 to prescribe that the value of supply of goods from Duty Free Shops at arrival terminal in international airports to the incoming passengers to be included in the value of exempt supplies for the purpose of reversal of input tax credit.

Rule 46: Tax invoice

To ease compliance burden of the taxpayers, clause (f) of rule 46 of CGST Rules, 2017 is amended to provide for requirement of only name of the State of the recipient, and not the name and full address of the recipient, on the tax invoice in cases of supply of taxable services by or through an ECO or by a supplier of OIDAR services to an unregistered recipient.

Rule 59: Form and manner of furnishing details of outward supplies.

Rule 59 has been amended to expand the scope of restriction on Registered person from filing GSTR-1 or furnishing Invoice Furnishing Facility (IFF). The RP who has received intimation under rule 88D, or; has not complied with provisions of rule 10A cannot file GSTR-1/IFF.

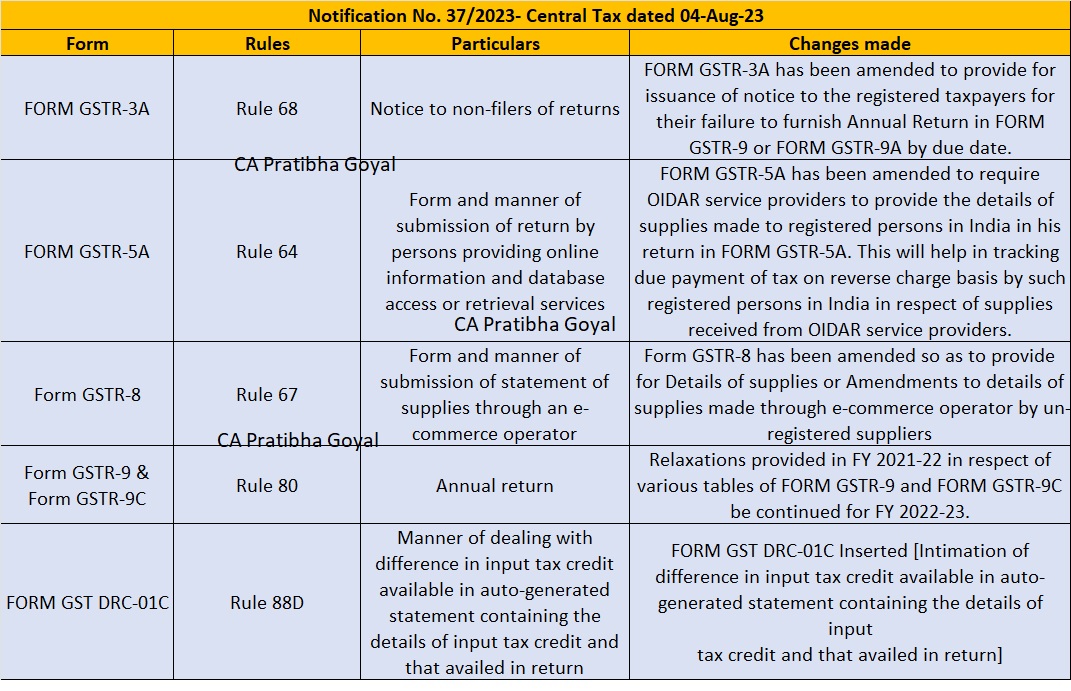

Rule 64: Form and manner of submission of return by persons providing online information and database access or retrieval services

Rule 64 has been amended to require OIDAR service providers to provide the details of supplies made to registered persons in India in his return in FORM GSTR-5A.

Rule 67: Form and manner of submission of statement of supplies through an e-commerce operator

Amendment has been made in Form GSTR-8 in order to incorporate amendments made in Section 52.

Rule 88D: Manner of dealing with difference in input tax credit available in auto-generated statement containing the details of input tax credit and that availed in return

New Rule 88D Notified for Manner of dealing with difference in input tax credit available in auto-generated statement containing the details of input tax credit and that availed in return

Rule 89: Application for refund of tax, interest, penalty, fees or any other amount

GST Refund after adjusting payment of tax can be claimed by casual taxable person only after furnishing the last return.

Rule 94: Order sanctioning interest on delayed refunds

Rule 94 has been amended to exclude the following period form period of delay for payment of interest: (a) any period of time beyond 15 days of receipt of notice in FORM GST RFD-08 under sub-rule (3) of rule 92, that the applicant takes to-

(i) furnish a reply in FORM GST RFD-09, or

(ii) submit additional documents or reply;

and

(b) any period of time taken either by the applicant for furnishing the correct details of the bank account to which the refund is to be credited or for validating the details of the bank account so furnished, where the amount of refund sanctioned could not be credited to the bank account furnished by the applicant.”.

Rule 96: Refund of integrated tax paid on goods or services exported out of India.

Certain provisos omitted

Rule 108: Appeal to the Appellate Authority

Manual filing of Appeal is legalized if the order is not uploaded electronically.

Rule 109: Application to the Appellate Authority.

Manual filing of Appeal is legalized for Department, if the order is not uploaded electronically.

Rule 138F: Information to be furnished in case of intra-State movement of gold, precious stones, etc. and generation of e-way bills

E-way bill requirement notified for inter-state moment of Gold/ Precious stones under chapter 71.

Rule 142B: Intimation of certain amounts liable to be recovered under section 79 of the Act

Rule 142B has been notified by CBIC for recovery of the tax and interest in respect of the amount intimated under Rule 88C (Difference in GSTR-1 and GSTR-3B)

Rule 162: Procedure for compounding of offences

Sub-rule (3A) has been inserted in rule 162 of CGST Rules, 2017 to prescribe the compounding amount for various offences under section 132 of CGST Act, 2017.

Rule 163: Consent based sharing of information

Rule 163 in CGST Rules, 2017 has been inserted to provide for the manner and conditions of consent-based sharing of information of registered persons available on the common portal with other systems.

About Author

CA Pratibha Goyal

Co Founder

CA Pratibha Goyal is Chartered Accountant qualified in 2016, is a Member of The Institute of Chartered Accountants of India having wide experience in the field of Auditing, Taxation, ROC, GST and Secretarial matters etc.

She has written over a thousand articles & has made several videos on topics related to Auditing & Taxation. As a Speaker she has delivered various sessions on various branches of NIRC of ICAI.

CA Pratibha Goyal is Chartered Accountant qualified in 2016, is a Member of The Institute of Chartered Accountants of India having wide experience in the field of Auditing, Taxation, ROC, GST and Secretarial matters etc.

She has written over a thousand articles & has made several videos on topics related to Auditing & Taxation. As a Speaker she has delivered various sessions on various branches of NIRC of ICAI.

Studycafe

Studycafe New Delhi, Delhi, India

New Delhi, Delhi, India 1486

1486My Recent Articles

- Biggest Labour Reform in Indian History: 4 Labour Codes Effective from today

- Tax Audit and ITR Due date not extended in this case: Know More

- Government notifies Agreement and Protocol between India and Qatar [Read Notification]

- CA Breaking: Results of ICAI Examination to be announced soon, Know probable Date

- Breaking: GSTR-3B Due Date for September 2025 extended by CBIC amid Diwali Festivities

Up Next

Loading suggestions…

Recent Posts

All Posts

Recent Posts

All Posts