Tax Audit Applicability for FY 2020-21

Tax Audit Applicability for FY 2020-21 Finance Act 2020, has introduced a mojor change in Section 44AB of Income Tax Act. Clause 23 of Finan

Tax Audit Applicability for FY 2020-21

Finance Act 2020, has introduced a mojor change in Section 44AB of Income Tax Act.

Clause 23 of Finance Act 2020 is as given below:

23. In section 44AB of the Income-tax Act,––

(A) in clause (a),––

(i) the word “or” occurring at the end shall be omitted;

(ii) the following proviso shall be inserted, namely:––

‘Provided that in the case of a person whose––

(a) aggregate of all amounts received including amount received for sales, turnover or gross receipts during the previous year, in cash, does not exceed five per cent. of the said amount; and

(b) aggregate of all payments made including amount incurred for expenditure, in cash, during the previous year does not exceed five per cent. of the said payment,

this clause shall have effect as if for the words “one crore rupees”, the words “five crore rupees” had been substituted; or’;

(B) in the Explanation, in clause (ii), after the word “means”, the words “date one month prior to” shall be inserted.

Tax Audit Applicability for FY 2020-21[/caption]

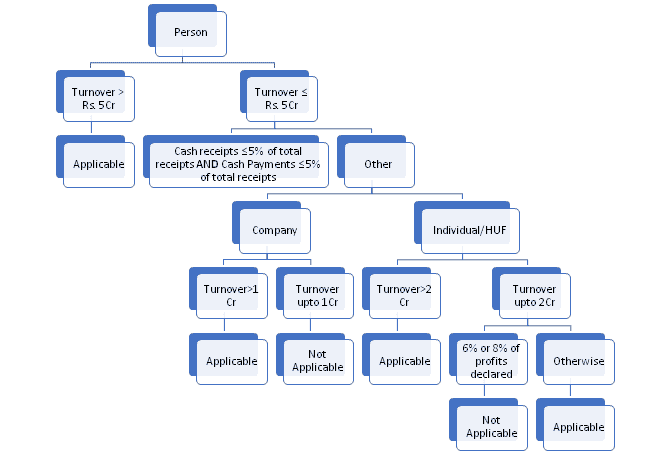

Provisions of Presumptive taxation are applicable where income of taxpayer exceeds the maximum amount which is not chargeable to income-tax in any previous year.

Presently (i.e FY 19-20),

This position can be understood with the help of Example:

[caption id="attachment_88070" align="aligncenter" width="664"] Tax Audit Applicability for FY 2020-21[/caption]

Provisions of Presumptive taxation are applicable where income of taxpayer exceeds the maximum amount which is not chargeable to income-tax in any previous year.

Presently (i.e FY 19-20),

- where the turnover of an assessee does not exceed Rs. 2 crores and

- he does not show profits equal to 6% or 8% as per 44AD,

Lets understand the Anamoly with the help of an Example:

1. Turnover of Mr A is Rs. 3.9 Cr. His cash receipts and payments are not exceeding 5% of receipts & payments. In this case, he is not liable to Audit irrespective of fact whether he shows profits equal to 6% or 8% or not. 2. For Example, Turnover of Mr A is Rs. 1.9 Cr. His cash receipts and payments are not exceeding 5% of receipts & payments. In this case, he is liable to Audit if he shows profits less than 6% or 8% as the case may be.About Author

Pratibha Goyal

Admin

This Account belongs to Admistrator of Studycafe.

This Account belongs to Admistrator of Studycafe.

Studycafe

Studycafe Delhi, Delhi, India

Delhi, Delhi, India 1080

1080My Recent Articles

- Chartered Accountants Association Embraces Income Tax Faceless Proceedings

- CBDT condones delay in filing form 10IC for AY 20-21: Know upto when to file the form to take concessional tax benefit

- ICAI Announced date of Live Coaching Classes for CA Intermediate Nov 2022 Exam

- ICAI Announced Registration Date for Online Home-Based Practical Training Assessment

- ICAI Released Mock Test Papers Series for May 2022 CA Exam

Up Next

Loading suggestions…

Recent Posts

All Posts

Tags

No tags yet.

Recent Posts

All Posts

Tags

No tags yet.