TCS on Foreign Remittance: MOF releases FAQs clarifying the covered Transactions:

TCS on Foreign Remittance: MOF releases FAQs clarifying the covered Transactions 1. Why is TCS required to be collected? Ans. Section 206C of the Inc…

TCS on Foreign Remittance

Table of Contents

TCS on Foreign Remittance: MOF releases FAQs clarifying the covered Transactions

1. Why is TCS required to be collected?

Ans. Section 206C of the Income-Tax Act 1961 provides for res in the business of trading in alcohol, liquor, forest produce, scrap etc. Sub-section (IG) of the aforesaid section provides for res on foreign remittance through the Libe1·alised Remittance Scheme and on the sale of overseas tour packages.2. Is TCS applicable to all remittances made abroad?

Ans. No. Only such remittances which are covered under LRS are liable to TCS. These have been detailed in the answer to Q (5) in Part B of the clarifications.3. What is the reason behind the increase in rates of TCS?

Ans. The reasons for the amendment are:- The payment of TCS is not a final tax

- If the TCS payee is a taxpayer, he can claim credit for the res as his tax payment against regular income and adjust it against the advance tax etc., payments accordingly.

- If the TCS is of a person not being a taxpayer, then the 20% rate on such presumed income is not high. The tax rate slab of 20% stands in the new regime for incomes over Rs 12 lacs and is 30% for incomes over Rs 15 lacs.

- Instances have come to notice where the LRS payments are disproportionately high when compared to the disclosed incomes

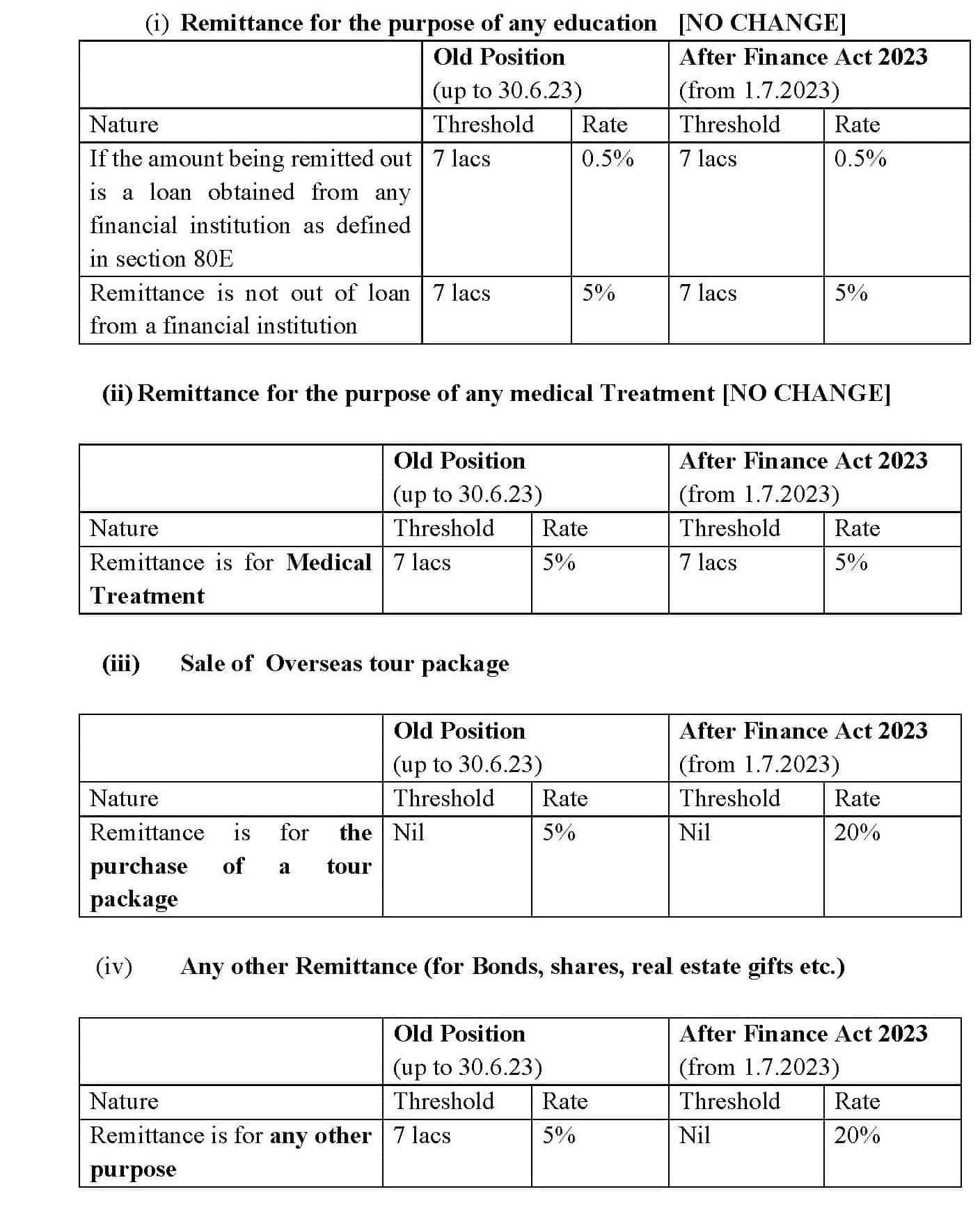

- No changes in medical or Education expenses- Position stays as it was before the Finance Act 2023.

- Primary Impact only on investment in assets such as real estate, bonds, stocks outside India by HNI and tour travel packages or gifts to non-residents.

- Those individuals remitting from their own funds are normally expected to be higher-income taxpayers, and for those remitting through institutional loans for education, a concessional rate of 0.5 % is provided.

4. What are the changes or increases in rates of TCS?

Ans. The TCS rates with the changes brought about in Finance Act 2023 are tabulated as under.

5. What is the impact on travel and incidental expenses related to education and medical treatment?

Ans. For res on remittance for travel and incidental expenses related to education and medical treatment, the rates of res as applicable to remittances for education and medical treatment, respectively, shall apply. A detailed clarification will be issued separately.About Author

CA Pratibha Goyal

Co Founder

CA Pratibha Goyal is Chartered Accountant qualified in 2016, is a Member of The Institute of Chartered Accountants of India having wide experience in the field of Auditing, Taxation, ROC, GST and Secretarial matters etc.

She has written over a thousand articles & has made several videos on topics related to Auditing & Taxation. As a Speaker she has delivered various sessions on various branches of NIRC of ICAI.

CA Pratibha Goyal is Chartered Accountant qualified in 2016, is a Member of The Institute of Chartered Accountants of India having wide experience in the field of Auditing, Taxation, ROC, GST and Secretarial matters etc.

She has written over a thousand articles & has made several videos on topics related to Auditing & Taxation. As a Speaker she has delivered various sessions on various branches of NIRC of ICAI.

Studycafe

Studycafe New Delhi, Delhi, India

New Delhi, Delhi, India 1486

1486My Recent Articles

- Biggest Labour Reform in Indian History: 4 Labour Codes Effective from today

- Tax Audit and ITR Due date not extended in this case: Know More

- Government notifies Agreement and Protocol between India and Qatar [Read Notification]

- CA Breaking: Results of ICAI Examination to be announced soon, Know probable Date

- Breaking: GSTR-3B Due Date for September 2025 extended by CBIC amid Diwali Festivities

Up Next

Loading suggestions…

Recent Posts

All Posts

Recent Posts

All Posts