TDS deducted and not deposited to Government can neither allowed or recovered from Deductee: ITAT:

ITAT Delhi in the matter of Kushal Navlakha vs. DCIT has ruled out that TDS deducted and not deposited to Government cannot be recovered from Deductee.

TDS Deducted but not deposited

Table of Contents

Relevant Text:

2. The grievance of the assessee read as under:1. That in facts and circumstances of the case, the order passed u/s. 250(6) of the Act by the Ld. CIT(A)-10 against the Assessee holding that the claim of TDS by the Assessee has been rightly disallowed by the DCIT (CPC) Bengaluru, is wrong, passed without following due process of law and in thus void ab initio, which needs to be struck down.

2. That in facts and circumstances of the case, the Ld. CIT(A) has wrongly held that the Assessee should follow up with the deductor and persuade the tax deducted at source to enable the Assessee to get the credit of tax deducted as this is illogical, without any sanctity of law and thus the disallowance of tax deducted, needs to be struck down.

3. That in facts and circumstances of the case, the Ld. CIT(A) has wrongly held that the Assessee has merely made assertions and does not have any corroborating document or any supporting evidences available with the Assessee to prove that the tenant of the Assessee deducted tax at source out of rent payments made to the Assessee as this is completely wrong and incorrect and thus the order of the CIT(A) needs to be struck down. Rs.52,200/-.

4. That in facts and in circumstances of the case the order of the CIT(A), by holding that, both, deduction of tax and subsequent deposit of such tax by the deductor are mandatory to give the credit of tax to the deductee, is bad in law, incorrect and arbitrary and thus the disallowance needs to be struck down.

5. That in facts and in circumstances of the order of Ld. CIT(A) is unjust, incorrect and arbitrary as he has not followed the provisions of the Act and not followed various judicial precedents of various higher courts in true letter and spirit which are in favour of the Assessee and thus the order of the Ld. CIT(A) needs to be struck down.

6. That in facts and circumstances of the case the order of the Ld. CIT(A) is incorrect, unjust and bad in law as the disallowance of TDS is a debatable issue and the same cannot be disallowed in order u/s. 143(1) of the Act and thus the disallowance needs to be struck down.

7. The appellant craves leave to add, alter amend, vary, and/ or withdraw any or all of the above grounds of Appeal.

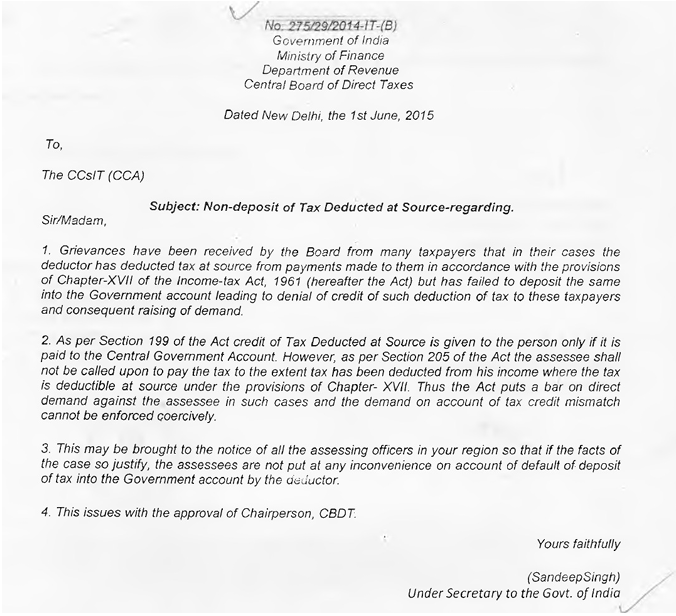

3. The sum and substance of the grievance of the assessee is that because the TDS deducted by the tenant amounting to Rs.52200/- was not deposited in the Government account the AO erred in recovering the amount from the assessee. 4. Briefly stated the facts of the case are that the assessee has let out its property to Mr. Rajeev Dhingra at a gross rent per month of Rs.43500/- totaling to Rs.522000/-on which Mr. Dhingra deducted tax at source @ 10% amounting to Rs.52200/-. It is an undisputed fact that Mr. Dhingra did not deposit this amount in the Government account and, therefore, the credit for TDS was denied by the AO. 5. On such facts we cannot direct the AO to give the credit of TDS the appeal of the assessee has to be dismissed. 6. However, in the interest of justice it would not be out of place to quote CBDT Circular on Non-Deposit of Tax Deducted at Source dated 1st June 2015. 7. In the light of the aforementioned CBDT circular, though we have dismissed the appeal of the assessee, yet we direct the AO not to take any recovery action for the outstanding tax liability keeping in mind the mandate of aforestated CBDT circular. With these directions the appeal is dismissed.

For Official appeal Download PDF Given Below:

7. In the light of the aforementioned CBDT circular, though we have dismissed the appeal of the assessee, yet we direct the AO not to take any recovery action for the outstanding tax liability keeping in mind the mandate of aforestated CBDT circular. With these directions the appeal is dismissed.

For Official appeal Download PDF Given Below:About Author

Reetu

Content Manager

Studycafe

Studycafe Delhi, Delhi, India

Delhi, Delhi, India 8072

8072My Recent Articles

- Income Tax Guide for Indian Defence Personnel for Tax Filing, Taxable Allowances and Other Benefits

- Income Tax Return Breaking: ITR Forms released for AY 25-26

- Ex-DRT Officials Sentenced to 5 Years Rigorous Imprisonment by Madras High Court along with Rs.27 Lakh Fine

- GSTN issued Advisory on Case Sensitivity in IRN Generation

- RBI to issue Notes of Rs.10 and Rs.500 bearing Signature of Guv Malhotra

Loading suggestions…

Recent Posts

All Posts

Recent Posts

All Posts