TDS on sale of Property U/S 194IA

TDS on sale of Property U/S 194IA : Budget 2013-14 introduced TDS on sale of property @ 1 % on all Immovable property i.e any land (other th

Table of Contents

TDS on sale of Property U/S 194IA :

Budget 2013-14 introduced TDS on sale of property @ 1 % on all Immovable property i.e any land (other than agricultural land) or any building or part of building having value over Rs. 50 Lakhs under Section 194 IA.

Important points on TDS on sale of Property U/S 194 IA:

- As per the provisions u/s 194 IA of the Income Tax Act, any buyer of immovable property with value of Rs 50 lakhs and above purchased on or after 1st june,2013 will have to deduct 1% TDS at the time of making payment to seller.

- Such immovable property mentioned above includes any building or part there of or any land but it does not include agricultural land.

- No TDS is to be deducted if the sale consideration is less than Rs 50lakhs. But if the consideration is paid in installments & the aggregate value is more than specified limit than TDS has to be deducted on each installment.

- Deduction of TDS is the responsibility of buyer not the seller. The buyer has to deduct TDS @ 1% of the total sales consideration, For example, if you have bought a property at Rs 51 lakh, you have to pay tax on Rs 51 lakh and not on Rs 1 lakh (i.e. Rs 51 lakh - Rs 50 lakh).

- TAN (Tax Deduction Account Number) details of only seller are needed not the buyer. That means buyer need not obtain a TAN.

- PAN (Permanent Account Number) details of both buyer and seller are mandatory. If Seller does not provide details of PAN, TDS will be deducted @ 20%. TDS is deducted at the time of payment or at the time of giving credit to the seller, whichever is earlier.

- Seller needs to obtain Form 26QB & buyer needs to obtain Form 16B.

- As per the CBDT notification no. 30/2016 dated April 29, 2016, the due date of payment of TDS on transfer of immovable property has been extended to thirty days (from existing seven days) from the end of the month in which the deduction is made. Example: If a taxpayer has made payment of sale consideration in the month of February, then corresponding TDS should be deposited on or before (thirty days) March 30th.

Guidelines for making payments of TDS on sale of property and obtaining Form 16B for the seller and Form 26QB for the buyer.

Step 1: Payment through Challan 26QB (Online and Offline)

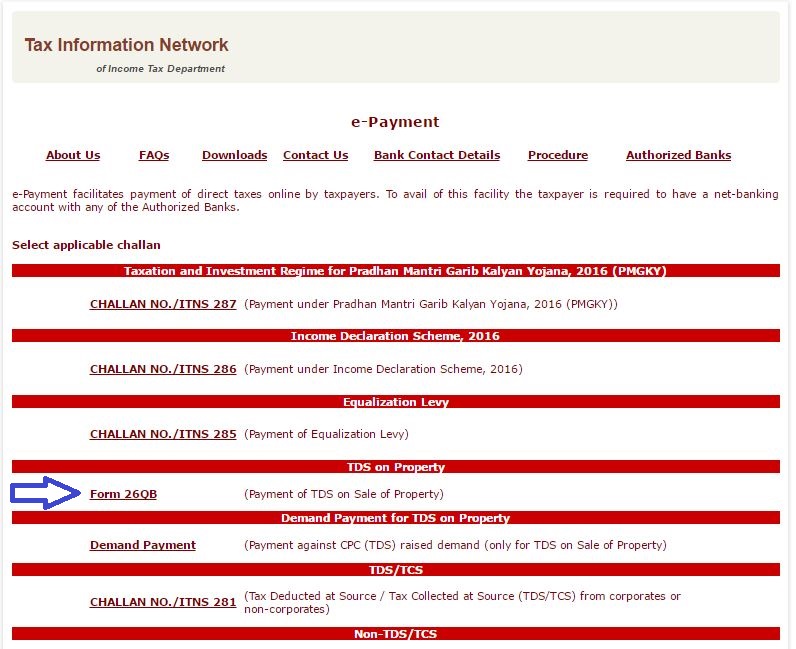

- Firstly one has to go to the following link for making the payment: https://onlineservices.tin.egov-nsdl.com/etaxnew/tdsnontds.jsp

- Once this link is opened click on Form 26QB (Payment of TDS on sale of property).

- Select (0021) in case of non corporate payer and 0020 in case of corporate payer.

- On filling in the various details called for in that form, click on Proceed at the bottom of the page, this will then take you to the next page, which will give you the option to select your bank.

- For making the payment 2 options are available at the bottom of the page: e-tax payment immediately (through net banking facility) and e-tax payment on a subsequent date (e-payment of taxes by visiting any of the Bank branches). Choose the one which you prefer and click on Proceed.

- Option 1 for payment : If you opt for e- tax payment immediately (through net banking) then you select the bank, then login using the normal online process for your bank.

- Option 2 for payment : If you opt for e-tax payment on a subsequent date (e-payment of taxes by visiting any of the Bank branches)then an online receipt for Form 26QB with a unique Acknowledgment Number will be generated for you. This is valid for 10 days after generation. You can take this to one of the authorized banks along with your cheque. The bank will proceed with the online payment on your behalf.

- Once the payment is made the bank will let you print challan 280 with a tick on (800), which is payment of TDS on sale of property.

- Take a printout of the challan and keep the same for your records and for the builder/seller if required.

- This was the first phase of the process i.e payment has been completed.

Step 2: Generation of Form 16B or Form 26QB

After depositing TDS to the government, the buyer is required to furnish the TDS certificate (Form 16B) to the seller. This is available around five days after depositing the TDS.

- For a registered user, to download Form 16B one has to wait for five days for the details to be reflected on TRACES website-https://www.tdscpc.gov.in/.

- For a first time user, you will have to register on this website -https://www.tdscpc.gov.in/. as a Tax Payer with your PAN Card Number and the Challan number issued during payment.

- Once you register whether as seller or buyer, you will be able to obtain the Form 16B or Form 26QB which has been approved and is reflected against your PAN in your Form 26AS.

- Check Form 26 AS within 30 days and you will notice that the payment you have made is reflected against TDS on sale of property is reflected in Part F of the Form 26 AS under Details of Tax Deducted at Source on Sale of Immoveable Property u/s 194(IA) [For Buyer of Property].

- This will give you details such as the TDS certificate number (generated by TRACES), name of deductee, PAN of deductee, acknowledgement number, total transaction amount, transaction date, TDS deposited, date of deposit, status of booking and date of booking.

Step 3: Download Form 26QB or Form 16B

After your payment in Form 26AS has been reflected, login to TRACES to Download your Form 26QB or Form 16B.

- Login to TRACES website, and click on Downloads tab.

- In the drop down menu click on requested downloads . If no application has been made you will be asked to make a request for download, here fill in the acknowledgment number (nine digit number) which is reflected on Form 26AS Part F as mentioned above. Once this is done, you will be able to view the status of your application, which generates an application request number.

- Within a couple of hours, the application gets processed and you will be able to view your Form 16B by putting in the request number which you have obtained. Download the .zip file. The password to open the .zip file is Date of Birth of Deductor (the format is DDMMYYYY). Your form will be available inside the .zip file as a pdf. You can take a printout of the same for your records as well as for handing over to the seller of the property.

- A similar process has to be followed by the seller to obtain form 26QB.

FAQ's on TDS on sale of Property:

1. Reason for Introduction of TDS on Property

P. Chidambaram while introducing TDS on Property said that Transactions of Immovable Property are usually undervalued and under-reported. Almost half of the Transactions don t even carry the PAN Card No. of the parties concerned.With a view to improving the reporting of such transactions and the taxation of Capital Gains, P. Chidambaram has introduced section 194IA which states that TDS on transactions of immovable property is to be deducted @ 1% where the consideration exceeds Rs. 50 Lakhs. This Section 194IA would be applicable wef 1st June 2013.

2. Amount on which the TDS is to be deducted

TDS @ 1% is to be deducted on all Property Transactions which are above Rs. 50 Lakhs. This TDS is to be deducted on all types of Property Transactions irrespective of whether the property in consideration is a flat or a building or a vacant plot. TDS is to be deducted irrespective of whether it is a Residential Property or Commercial or Industrial Property. TDS is to be deducted on all types of property transactions except Agricultural Land.

3. Due date of tax to be deposited with Govt

As per the CBDT notification no. 30/2016 dated April 29, 2016, the due date of payment of TDS on transfer of immovable property has been extended to thirty days (from existing seven days) from the end of the month in which the deduction is made.

Example: If a taxpayer has made payment of sale consideration in the month of February, then corresponding TDS should be deposited on or before (thirty days) March 30th.

4. What If More than 1 Buyer or 1 Seller

In case there is more than 1 buyer and the individual purchase price of each buyer is less than Rs. 50 Lakhs, but the aggregate value of the transaction exceeds Rs. 50 Lakhs, Section 194IA would be applicable and the TDS on Property would be required to be deducted and deposited with the govt before the due date.

Similarly, if there is more than 1 seller and the individual sale price of each seller is less than Rs. 50 Lakhs, but the aggregate value of the transaction exceeds Rs. 50 Lakhs, Section 194-IA would be applicable and TDS would be required to be deducted by the buyer at the time of making the payment to the seller. In case of more than 1 buyer/ 1 seller, Form 26QB has to be filled in separately for each buyer-seller combination. Eg: In case of 1 buyer and 2 sellers 2 forms have to be submitted, and in case of 2 buyers and 2 sellers 4 forms have to be submitted for their respective property share.

5. Interest / Penalty for Non-Deduction/ Deposit of TDS on Property

Yes, Interest on Late Deposit of TDS on Property In case the TDS has not been deducted, the buyer would be required to pay 1% interest per month on the amount not deducted. In case, the TDS has been deducted but has not been paid, Interest @ 1.5% per month would be applicable in such a case.

6. It is important for both the buyer and the seller to file an Income Tax Return in the year of purchase

No it is not mandatory but It is advisable for both the buyer and the seller to file an Income Tax Return in the year of purchase.

7. I am a buyer. Should i deduct TDS on the amount exceeding the property value of Rs 50 lakh or the entire amount at which I have bought the property

The buyer has to deduct TDS @ 1% of the total sales consideration, For example, if you have bought a property at Rs 51 lakh, you have to pay tax on Rs 51 lakh and not on Rs 1lakh (i.e. Rs 51lakh - Rs 50lakh).

8. I am a buyer. How do I procure TAN to report the TDS on sale of property

TAN is the Tax Deduction Account Number. Neither the buyer, nor the seller is required to procure the TAN for deducting TDS on the sale and purchase of the property. However, it is mandatory for the buyer to quote his or her PAN as well as the seller(s) s PAN while deducting TDS on the purchase transaction.

9. Section 194-IA as per Income tax Act, 1961:

(1) Any person, being a transferee, responsible for paying (other than the person referred to in section 194LA) to a resident transferor any sum by way of consideration for transfer of any immovable property (other than agricultural land), shall, at the time of credit of such sum to the account of the transferor or at the time of payment of such sum in cash or by issue of a cheque or draft or by any other mode, whichever is earlier, deduct an amount equal to one per cent of such sum as income-tax thereon.

(2) No deduction under sub-section (1) shall be made where the consideration for the transfer of an immovable property is less than fifty lakh rupees.

(3) The provisions of section 203A shall not apply to a person required to deduct tax in accordance with the provisions of this section.

Explanation For the purposes of this section,

(a) "agricultural land" means agricultural land in India, not being a land situate in any area referred to in items (a) and (b) of sub-clause (iii) of clause (14) of section 2;

(b) "immovable property" means any land (other than agricultural land) or any building or part of a building.

In the above article we have tried to explain each aspect of TDS on sale of Property. But still if you have any doubts regarding deduction of TDS and Deposit you can comment below.

About Author

CA Deepak Gupta

Co Founder

StudyCafe

StudyCafe Delhi, Delhi, India

Delhi, Delhi, India 3423

3423My Recent Articles

- UltraTech Cement slapped with Rs. 808.78 Cr Income Tax Demand

- GST: High Court upheld constitutional validity of Section 16(2)(c), asks government to address ITC issues of genuine purchasers

- Old vs New Tax Regime for Tax Year 2026-27

- High court criticizes Income Tax Department for not releasing ITR Utilities despite 11 years of directions

- Fino Payments Bank CEO Rishi Gupta Gets Bail in GST Case, Bank Clarifies No Direct Link

Loading suggestions…

Recent Posts

All Posts

Tags

No tags yet.

Recent Posts

All Posts

Tags

No tags yet.