CA Nilesh Mahajan | Aug 24, 2022 |

UNDERSTANDING OF INTEREST ON DELAYED PAYMENT OF OUTPUT GST LIABILITY

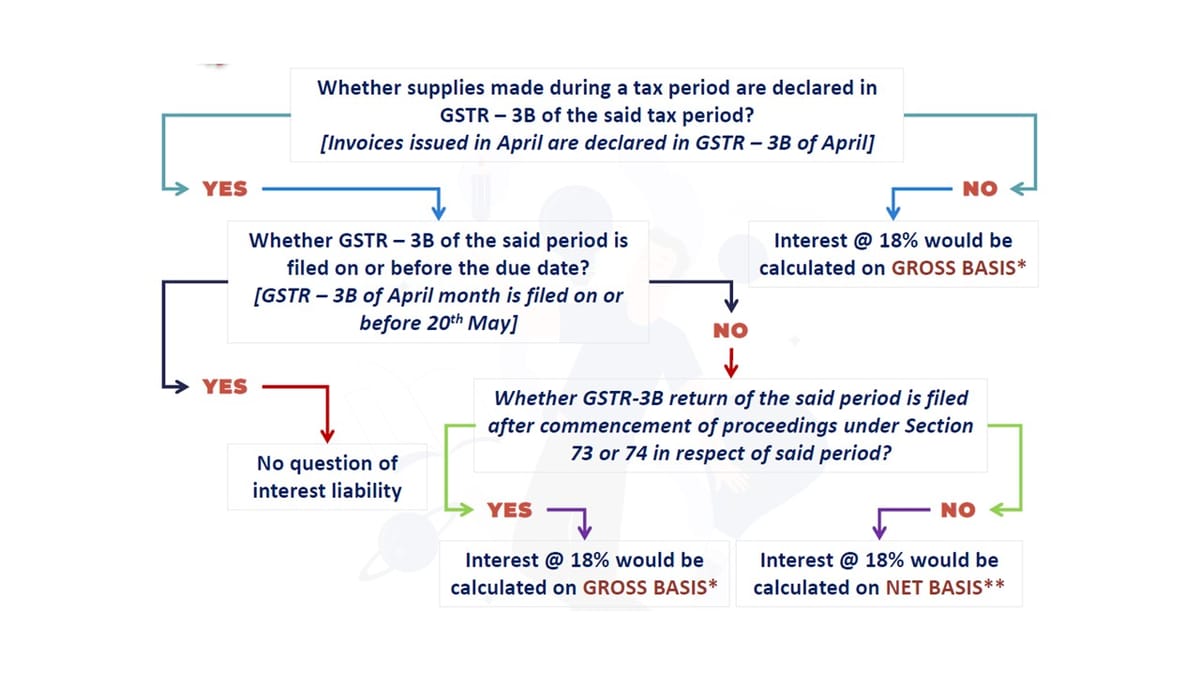

*Gross basis [Section 50 (1) read with Rule 88B (2)]: Interest will be calculated on delayed payment of GST through debiting both cash as well as credit ledgers

**Net basis [Proviso to Section 50 (1) read with Rule 88B (1)]: Interest will be calculated on delayed payment of GST to the extent is paid by way of debiting cash ledger even if delayed payment of GST is paid by way of debiting both credit & cash ledgers

| Sr No | Return/ Tax period | Supplies declared in tax period are pertaining to | Amt [Rs.] | Due date for tax period | Actual filing date | Payment made through | Interest will be calculated on | |

| Credit ledger | Cash ledger | |||||||

| A | April | April | 10,000 | 20th May | 1st June | 6,000 | 4,000 | 4,000 |

| B | April | March | 15,000 | 20th May | 1st June | 10,000 | 5,000 | 15,000 |

Section 50. Interest on delayed payment of tax.

(1) Every person who is liable to pay tax in accordance with the provisions of this Act or the rules made thereunder, but fails to pay the tax or any part thereof to the Government within the period prescribed, shall for the period for which the tax or any part thereof remains unpaid, pay, on his own, interest at such rate, not exceeding eighteen per cent., as may be notified by the Government on the recommendations of the Council:

Provided that the interest on tax payable in respect of supplies made during a tax period and declared in the return for the said period furnished after the due date in accordance with the provisions of section 39, except where such return is furnished after commencement of any proceedings under section 73 or section 74 in respect of the said period, shall be levied on that portion of the tax that is paid by debiting the electronic cash ledger.

(2) The interest under sub-section (1) shall be calculated, in such manner as may be prescribed, from the day succeeding the day on which such tax was due to be paid.

(3) Where the input tax credit has been wrongly availed and utilised, the registered person shall pay interest on such input tax credit wrongly availed and utilised, at such rate not exceeding twenty-four per cent. as may be notified by the Government, on the recommendations of the Council, and the interest shall be calculated, in such manner as may be prescribed

Rule 88B. Manner of calculating interest on delayed payment of tax

(1) In case, where the supplies made during a tax period are declared by the registered person in the return for the said period and the said return is furnished after the due date in accordance with provisions of section 39, except where such return is furnished after commencement of any proceedings under section 73 or section 74 in respect of the said period, the interest on tax payable in respect of such supplies shall be calculated on the portion of tax which is paid by debiting the electronic cash ledger, for the period of delay in filing the said return beyond the due date, at such rate as may be notified under sub-section (1) of section 50.

(2) In all other cases, where interest is payable in accordance with sub section (1) of section 50, the interest shall be calculated on the amount of tax which remains unpaid, for the period starting from the date on which such tax was due to be paid till the date such tax is paid, at such rate as may be notified under sub-section (1) of section 50.

(3) In case, where interest is payable on the amount of input tax credit wrongly availed and utilised in accordance with sub-section (3) of section 50, the interest shall be calculated on the amount of input tax credit wrongly availed and utilised, for the period starting from the date of utilisation of such wrongly availed input tax credit till the date of reversal of such credit or payment of tax in respect of such amount, at such rate as may be notified under said sub-section (3) of section 50.

Explanation.-For the purposes of this sub-rule, –

(1) input tax credit wrongly availed shall be construed to have been utilised, when the balance in the electronic credit ledger falls below the amount of input tax credit wrongly availed, and the extent of such utilisation of input tax credit shall be the amount by which the balance in the electronic credit ledger falls below the amount of input tax credit wrongly availed.

(2) the date of utilisation of such input tax credit shall be taken to be, –

(a) the date, on which the return is due to be furnished under section 39 or the actual date of filing of the said return, whichever is earlier, if the balance in the electronic credit ledger falls below the amount of input tax credit wrongly availed, on account of payment of tax through the said return; or

(b) the date of debit in the electronic credit ledger when the balance in the electronic credit ledger falls below the amount of input tax credit wrongly availed, in all other cases.

In case of any Doubt regarding Membership you can mail us at [email protected]

Join Studycafe's WhatsApp Group or Telegram Channel for Latest Updates on Government Job, Sarkari Naukri, Private Jobs, Income Tax, GST, Companies Act, Judgements and CA, CS, ICWA, and MUCH MORE!"