Nidhi | May 13, 2025 |

Updates to Rules in GST: Effective From April 1, 2025 and June 1, 2025

Starting from April 1, 2025, and June 1, 2025, there are some important changes introduced to the GST rules. Taxpayers should stay updated on the new rules to avoid any penalty or interest and ensure compliance. Here is what you need to know about the updated GST rules.

E-Invoice Generation

E-Invoice Generation

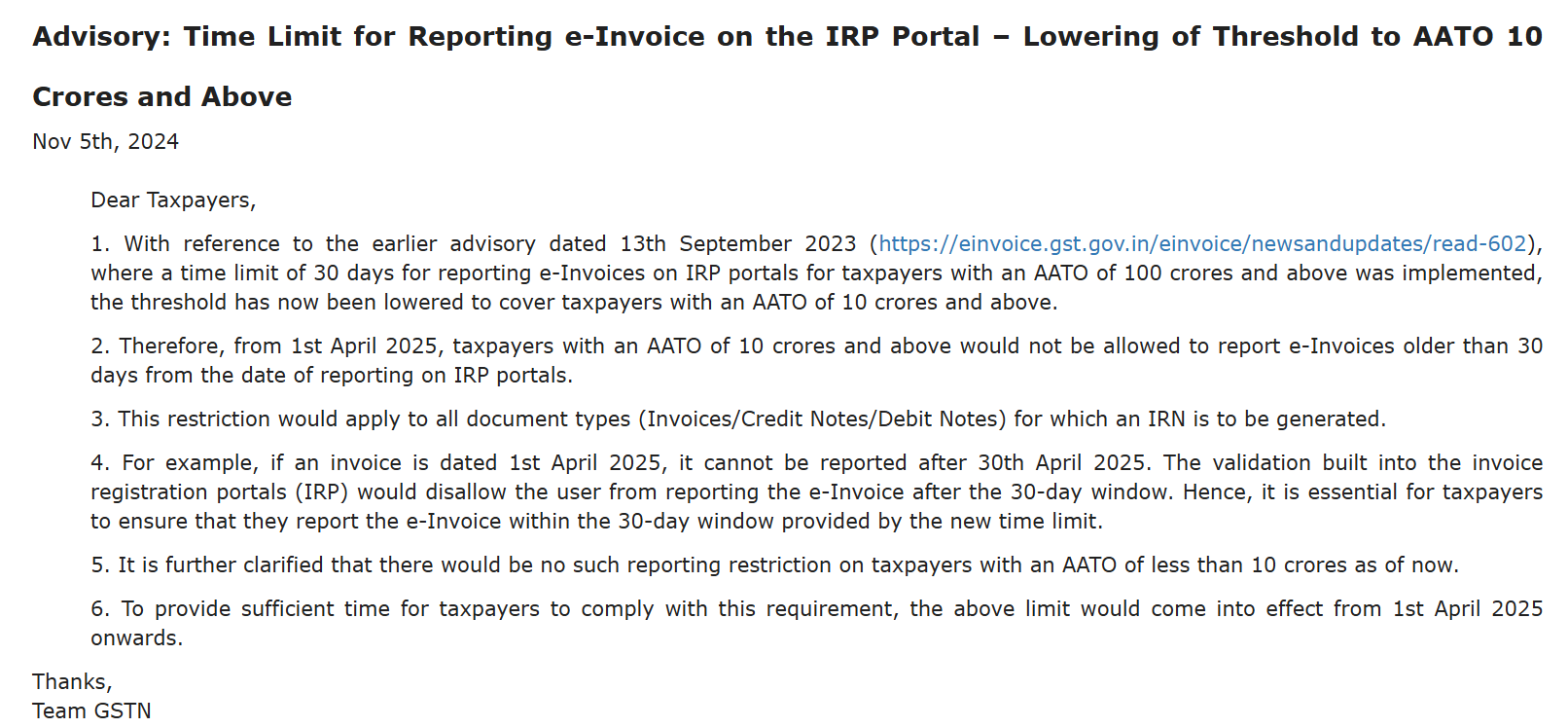

From 1st April 2025, businesses with an annual turnover of Rs. 10 crore or more are required to generate E-invoices on the Invoice Registration Portal (IRP) within 30 days of issuing an invoice.

Previously, this rule only applied to businesses with a turnover of Rs. 100 crore or above. Now, the limit has been cut to Rs. 10 crore, as per the GST Advisory dated 5th November 2024. Therefore, an invoice that is older than 30 days cannot be submitted on IRP.

Two-Factor Login Now Must for GST Portal

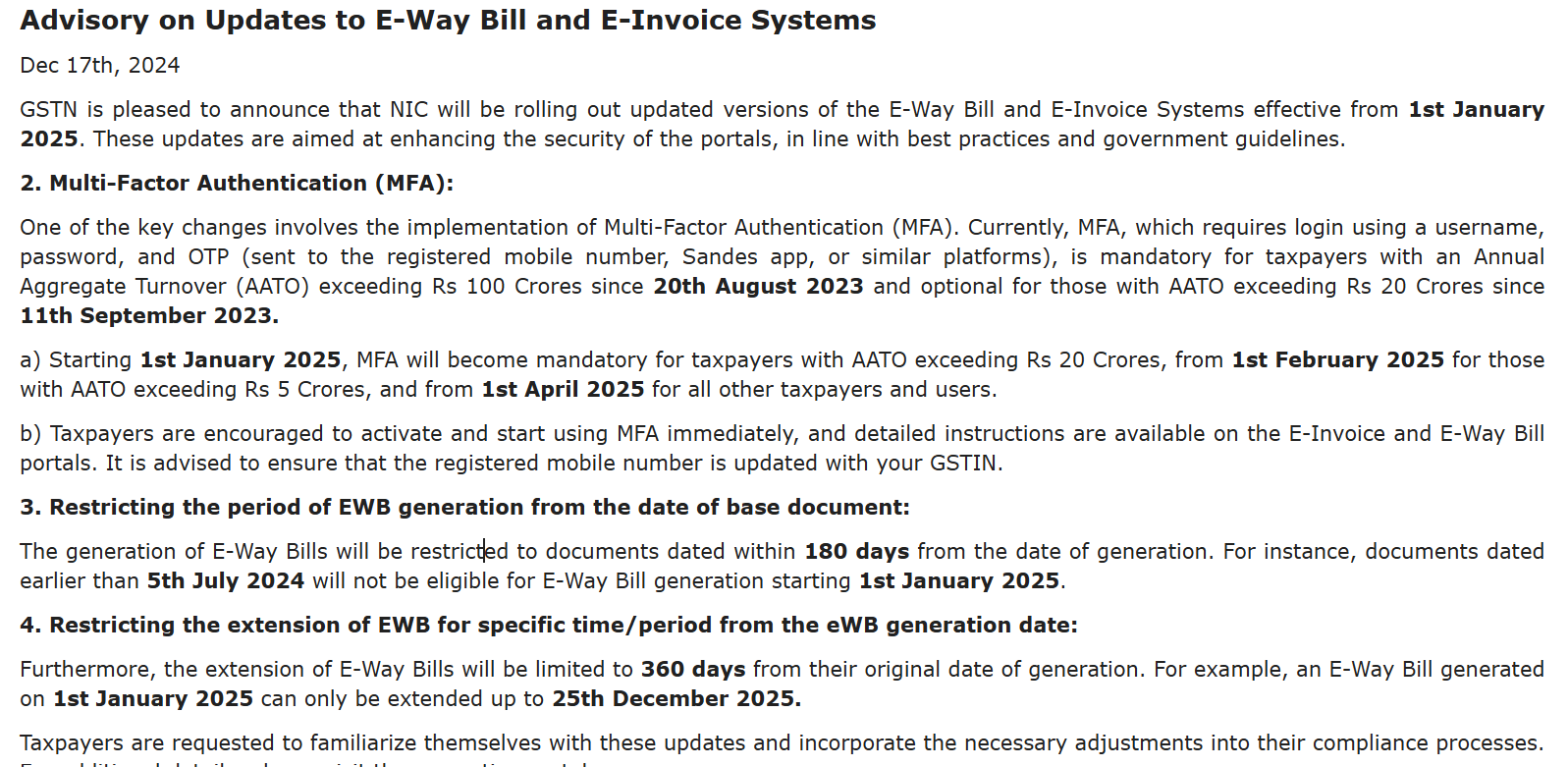

From 1st April 2025, all users are required to complete an extra step while logging into the GST system for e-invoices and e-way bills. Along with your usual login ID and password, you will also need to enter a code (OTP) sent to your registered phone or use the Sandes app.

This extra layer of security has been introduced to keep your account safe from unauthorized access.

Manual Entry of HSN Codes No Longer Needed in GSTR-1

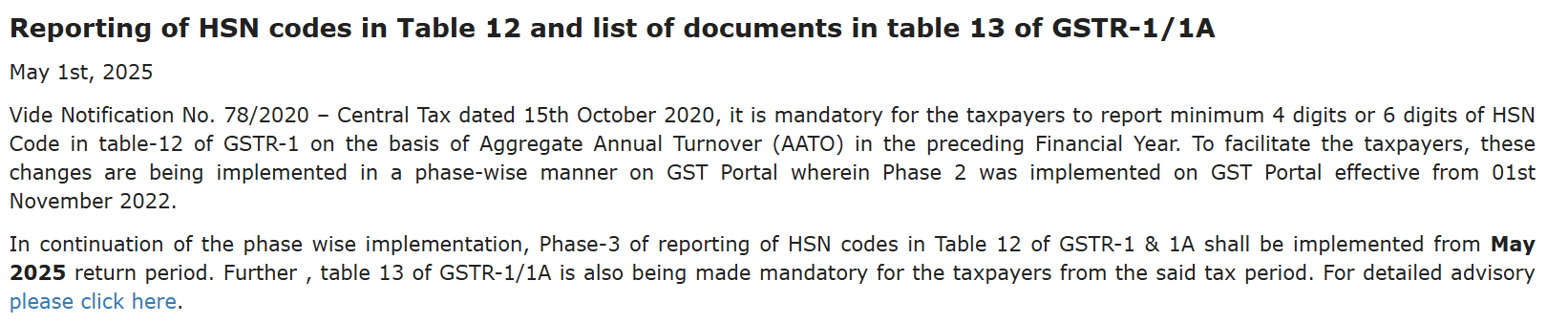

As per GSTN advisory, the manual entry of HSN codes and selecting them from a dropdown in Table 12 of GSTR-1 and GSTR-1A will no longer be needed. This change is already in effect from the return period starting May 2025. Table 12 has also been divided into B2B and B2C supplies, and validation checks are added to verify the taxable value and tax amount.

No Modifications in the Values in Table 3.2 of GSTR-3B

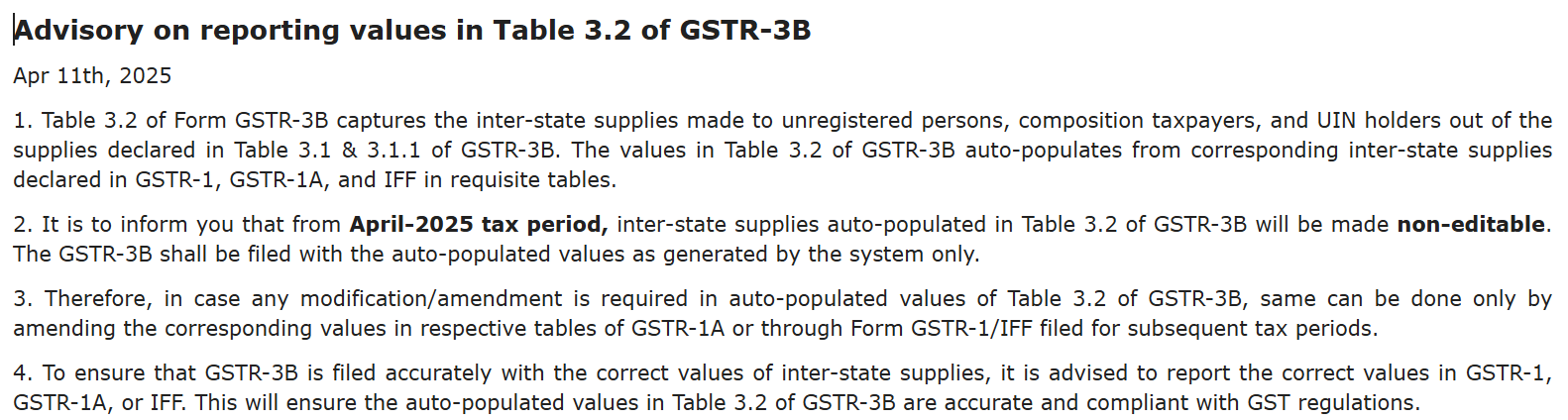

Starting from the April 2025 tax period, inter-state supply details auto-filled in Table 3.2 of GSTR-3B, which relates to sales made to Composition dealers, unregistered persons, and UIN holders, will no longer be editable, as per the GST advisory dated 11 April 2025.

GSTR-3B must now be filed using only the system-generated values, which are based on details filed in GSTR-1A or through Form GSTR-1/IFF. Therefore, taxpayers cannot make any changes or modifications in the auto-filled values of Table 3.2 of GSTR-3B. It can only be done by revising the related values in the relevant tables of GSTR-1A or through Form GSTR-1/IFF in the returns filed for the following tax periods.

To ensure uniformity and avoid duplicate entries, invoice numbers entered in any format (like “abc“, “ABC“, or “Abc“) will now be automatically changed to capital words (i.e., ABC) before generating the IRN. This matches the way invoice numbers are already handled in GSTR-1, where the system does not care about letter case.

However, taxpayers do not need to manually change the invoice number. The IRN system will automatically do it. But from 01 June 2025, it is advised to start using uppercase letters while generating invoices to stay in line with the system.

In case of any Doubt regarding Membership you can mail us at [email protected]

Join Studycafe's WhatsApp Group or Telegram Channel for Latest Updates on Government Job, Sarkari Naukri, Private Jobs, Income Tax, GST, Companies Act, Judgements and CA, CS, ICWA, and MUCH MORE!"