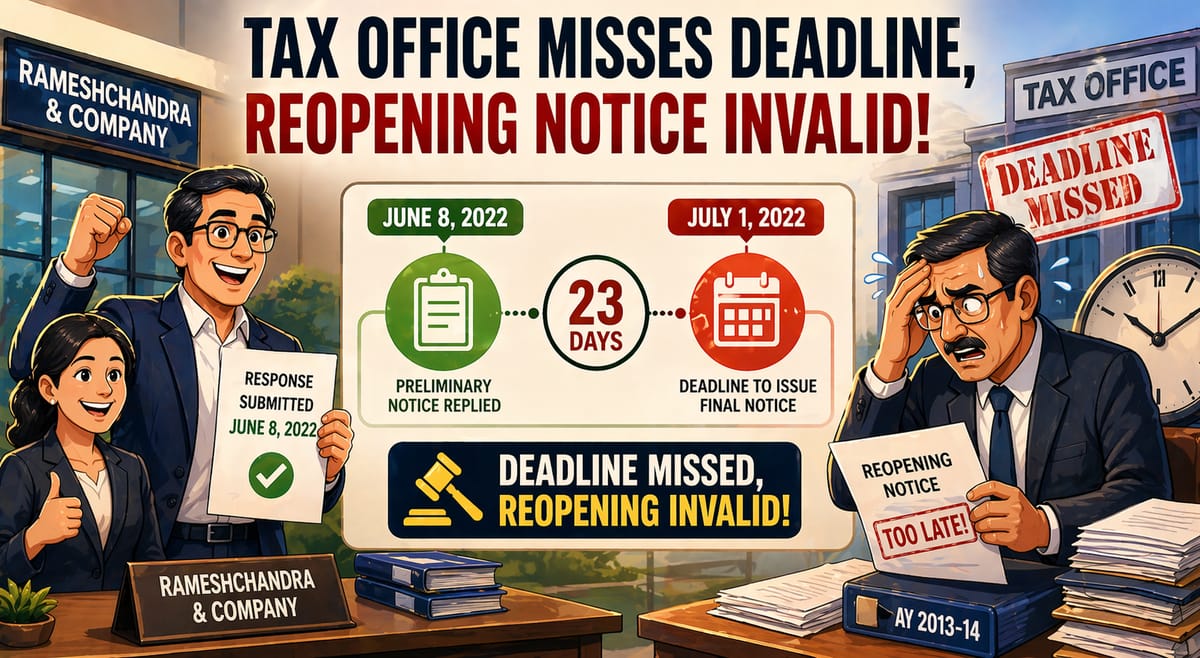

A small delay made a big difference. After the company replied on June 8, 2022, the tax office had only 23 days to send the final notice, but they sent it almost a month late. Because of this delay, they lost their legal right, and the tribunal cancelled the reassessment.

Khushi Jain | Apr 24, 2026 |

The tax office issued the reassessment notice nearly a month late, prompting the Tribunal to conclude it had lost its authority to proceed.

Facts of the case

The tax office tried to reopen the assessment for Rameshchandra & Company for the 2013-14 tax year but missed a legal deadline. After the company responded to a preliminary notice on June 8, 2022, the tax office had only 23 days to issue the final notice, with a deadline of July 1, 2022.

They failed to send the notice until July 28, 2022, nearly a month late. As the deadline had passed, the Tribunal ruled that the tax office lost its authority to proceed, dismissing the reassessment.

Issue of the case

Whether the notice issued on July 28, 2022, was barred by limitation?

Decision of the Tribunal

The Tribunal decided in favor of the company and annulled the tax office’s reassessment due to its initiation occurring too late.

According to the law, the tax office was allotted a 23-day “surviving period” to complete its documentation. Given that the company responded to a preliminary notice on June 8, 2022, the office was obligated to issue the final notice by July 1, 2022.

Nevertheless, the office did not dispatch the notice until July 28, 2022. As they failed to meet this stringent deadline, the court ruled that the tax office forfeited its legal right to continue with the case.

In case of any Doubt regarding Membership you can mail us at [email protected]

Join Studycafe's WhatsApp Group or Telegram Channel for Latest Updates on Government Job, Sarkari Naukri, Private Jobs, Income Tax, GST, Companies Act, Judgements and CA, CS, ICWA, and MUCH MORE!"