After a survey led to an excessive tax demand based on just two days of sales, the ITAT stepped in to strike down the "commercially impossible" estimate.

Khushi Jain | May 1, 2026 |

Income Tax reassessment proceedings cannot be held bad in law due to a lack of a signature on notice

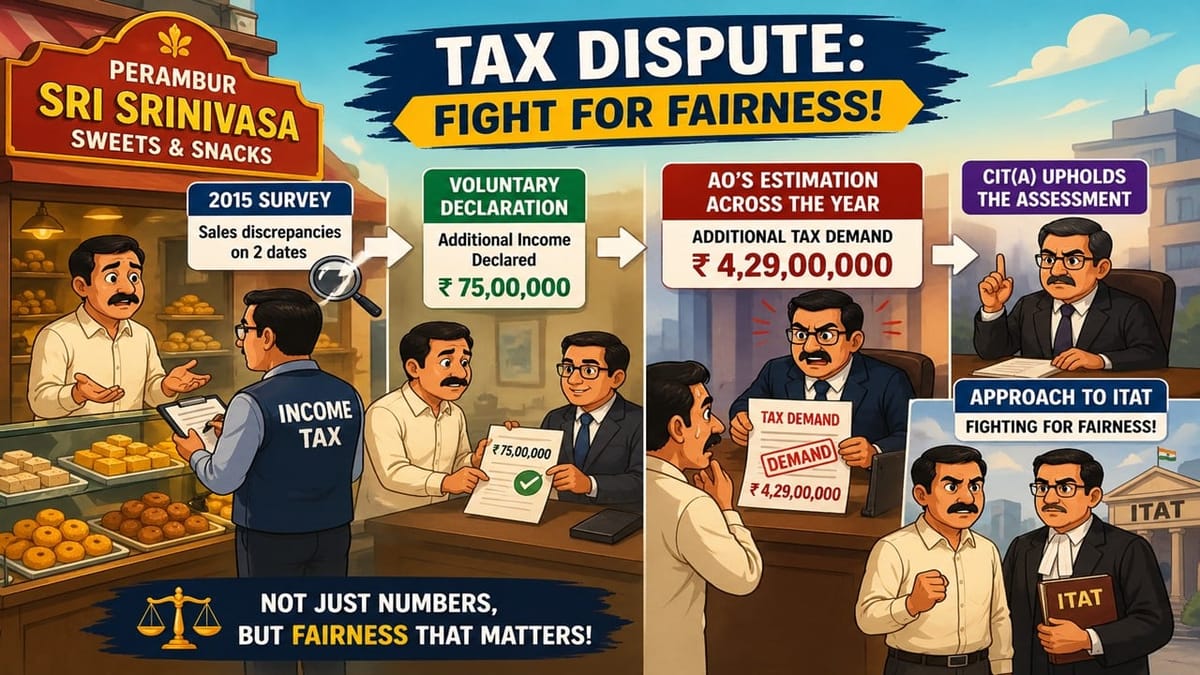

The assessee is a partnership firm engaged in the manufacturing and sale of sweets and snacks. A survey under Section 133A of the Income Tax Act, 1961, was conducted at the assessee’s premises on 03.09.2015. During the survey, discrepancies in sales entries were noted only for two specific dates (25.08.2015 and 28.08.2015), based on which statements were recorded from the firm’s accountant and one of the partners. In response to the survey, the assessee voluntarily offered ₹7,500,000 as additional income in its return filed for the assessment year 2015-16 to avoid prolonged controversy. The AO extrapolated the discrepancies found on those two specific days to the entire year, estimating an additional suppressed turnover of ₹6.56 crores and an additional income of ₹5.04 crores. After accounting for the ₹7,500,000 already offered, the AO made an addition of ₹42,900,000. The Commissioner of Income Tax (Appeals) confirmed this addition, leading the assessee to appeal before the ITAT.

Issue of the case

Were the reassessment proceedings bad in law due to a lack of a signature on the notice issued under Section 148 and the absence of a notice under Section 143(2)?

Was the addition of ₹42,900,000 as business income—based on extrapolation from limited survey findings and a sworn statement—legally sustainable?

Decision of the Tribunal

The tribunal rejected the assessee’s legal challenge. The Department successfully demonstrated that a signed copy of the notice under Section 148 had been duly served and acknowledged by the assessee. The Tribunal allowed the assessee’s appeal and directed the AO to delete the addition of Rs. 42,900,000. No unaccounted assets, investments, unexplained expenditures, or other incriminating material was found during the survey.

The Tribunal reaffirmed that statements recorded under Section 133A do not have conclusive evidentiary value and cannot, by themselves, form the sole basis for an addition without independent supporting material.

The AO’s profit estimation was deemed “commercially implausible” and “arbitrary.” An analysis of the assessee’s own five-year financial history showed an average net profit rate of 4.17%, which proved that the voluntary disclosure of ₹7,500,000 was already more than sufficient to cover any reasonable profit margin on the alleged suppressed sales.

In case of any Doubt regarding Membership you can mail us at [email protected]

Join Studycafe's WhatsApp Group or Telegram Channel for Latest Updates on Government Job, Sarkari Naukri, Private Jobs, Income Tax, GST, Companies Act, Judgements and CA, CS, ICWA, and MUCH MORE!"