RD Hyderabad penalises company and 2 directors for late filing of form PAS-03:

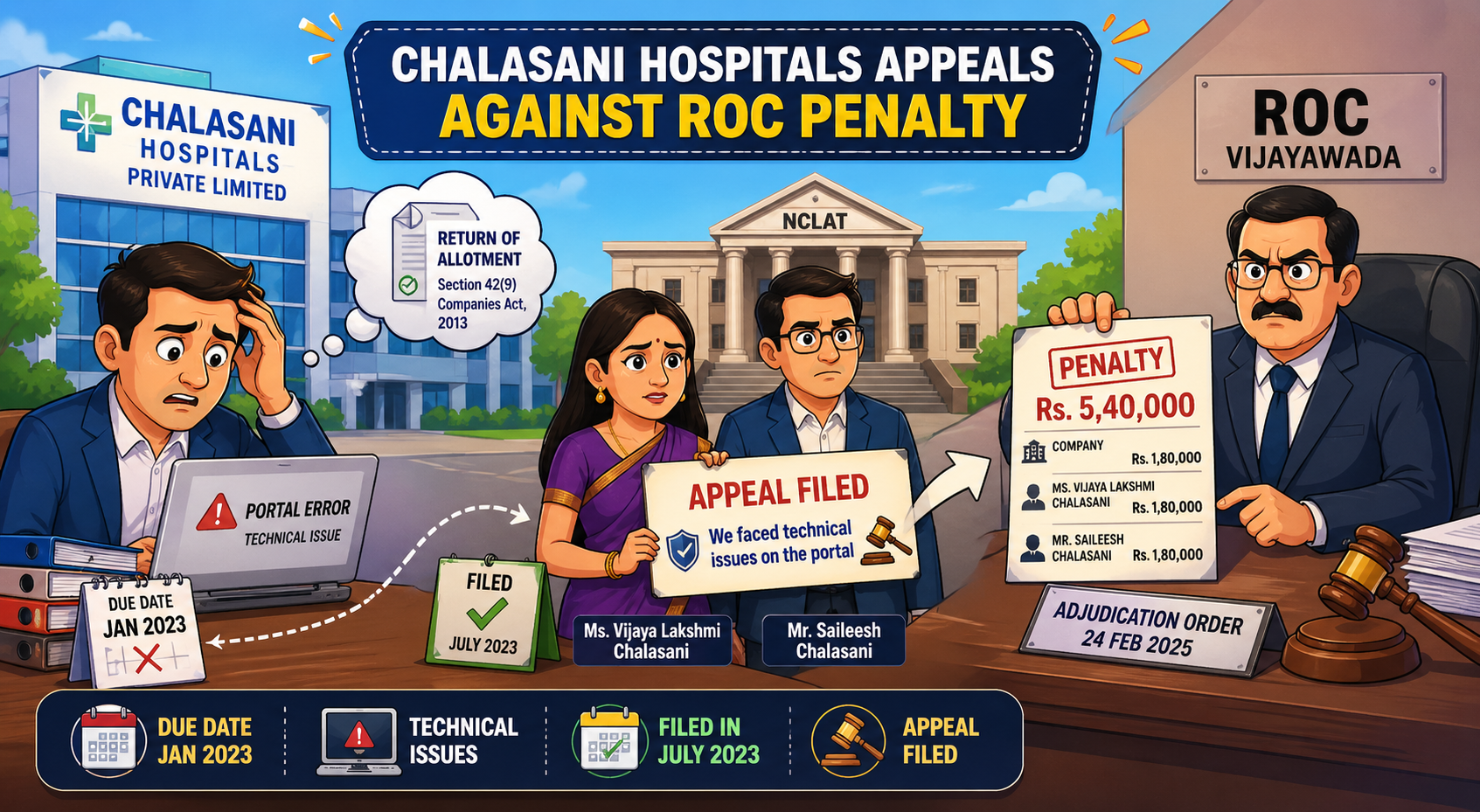

Chalasani Hospitals Pvt. Ltd. and its directors challenged an ROC order over a delayed PAS-3 filing which is originally due in Jan 2023 but filed in July, citing portal issues. A ₹5.4 lakh penalty was imposed.

MCA’s Timely Extension and the Halving of a ₹5.4 Lakh Fine

RD Hyderabad penalises company and 2 directors for late filing of form PAS-03

On February 24, 2025, the Registrar of Companies (ROC) in Vijayawada fined Chalasani Hospitals Private Limited and its two directors (Ms. Vijaya Lakshmi Chalasani and Mr. Saileesh Chalasani). Each party was fined ₹1,80,000, bringing the total penalty to ₹5,40,000.

The company was penalized under Section 42(9) of the Companies Act, 2013, because they did not file the "return of allotment" (Form PAS-03) on time. This form is a mandatory document that companies must submit when they issue new shares to investors.

The company and its directors appealed the penalty, arguing that the delay was not their fault. They pointed out two main factors:

They claimed they could not file the form earlier because of ongoing technical glitches on the official Ministry of Corporate Affairs (MCA) website.

Government Extension: They provided proof of MCA General Circular No. 4/2023, which officially extended the deadline for filing Form PAS-03 until March 31, 2023.

Issue involved in the case

Whether the penalty imposed by the ROC for the delayed filing of the return of allotment under Section 42(9) of the Companies Act, 2013, was accurate, given the appellants' claim that a portion of the delay was caused by portal issues and was covered by a government-issued time extension.

Decision of RD Hyderabad

The Regional Director (RD) Hyderabad accepted the appellants' argument regarding the MCA circular, noting that the period from January 2023 to March 2023 should be exempted.

The period of delay was recalculated to 95 days (from 01-04-2023 to 04-07-2023). Consequently, the penalty was modified to ₹1,000 per day of default. The revised penalty was fixed at ₹95,000 each for the company and the two directors, aggregating to a total of ₹2,85,000. The appellants were directed to pay the penalty from their personal sources/income and were reminded that failure to do so within 60 days would result in further action by the ROC under Section 454(8) of the Companies Act, 2013.

About Author

Khushi Jain

Legal Content Writer

StudyCafe

StudyCafe Delhi, Delhi, India

Delhi, Delhi, India 80

80My Recent Articles

- ROC Chennai Orders Penalty for delay in filing MGT-17: Short Staff no Excuse

- Penalty Order Passed by ROC Chennai for Non-Disclosure in Form PAS-3

- ROC Imposes Penalty For Non-Compliance In Securities Allotment Filing

- GST: Bombay High Court Upholds Validity of Manual Appeal

- From Rs. 275 Crore to Zero: United Breweries Gets Relief in Sales Tax Dispute

Up Next

Loading suggestions…

Recent Posts

All Posts

Recent Posts

All Posts