Big Tax Dispute: Rs 7.96 Cr Addition Slashed After New Evidence, But Rule 46A Ignored by AO:

Rs 7.96 Cr addition was cut to Rs 24.18 L based on fresh evidence, but it was accepted without the AO’s review. Court held this violated Rule 46A and due process.

Fresh Evidence Reduced Addition; Rule 46A Issue Upheld On Appeal

Big Tax Dispute: Rs 7.96 Cr Addition Slashed After New Evidence, But Rule 46A Ignored by AO

Can ITAT rely on new evidence admitted without AO’s opportunity or Rule 46A compliance?

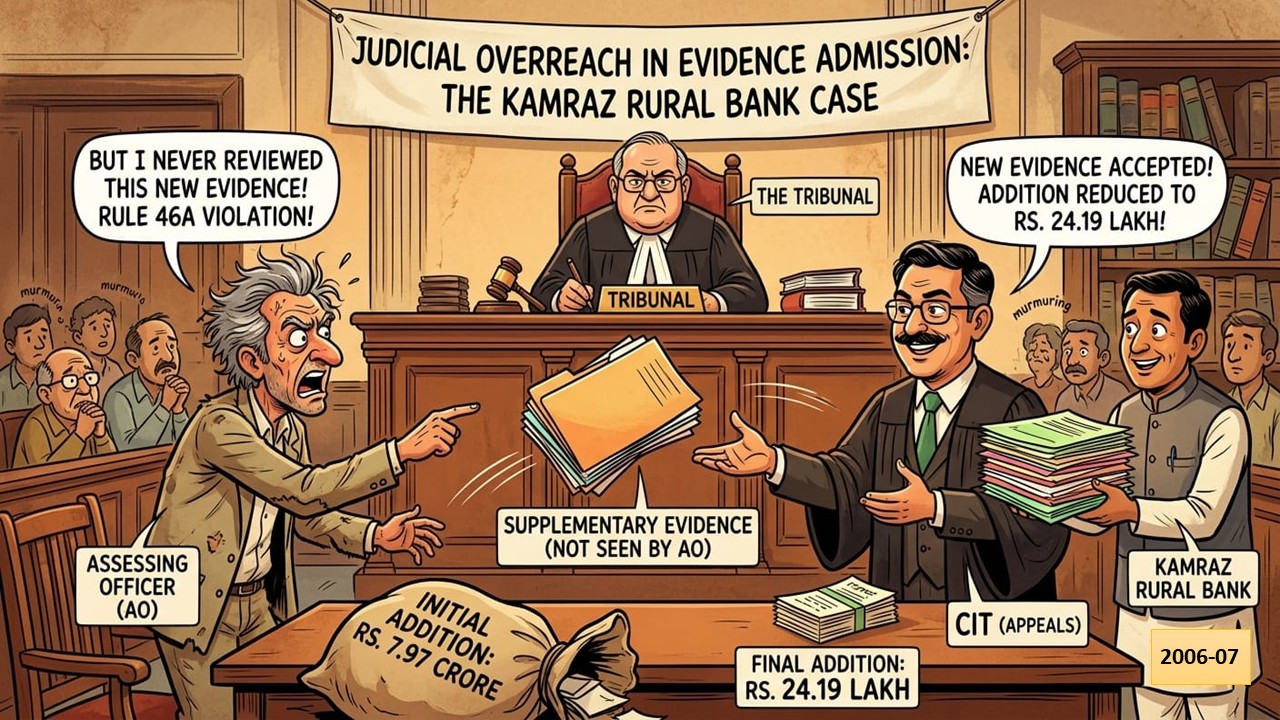

Fact Of The Case

In the 2006-07 assessment year, Kamraz Rural Bank reported an income of Rs 51,946,000/-. The Assessing Officer (AO) later added Rs. 79,680,000/- to the bank's income under Section 40(a)(ia) for not withholding tax on interest payments over Rs. 10,000/-.

During the appeal, the Commissioner of Income Tax (Appeals) accepted new evidence from the bank showing that only Rs. 24,18,596/- was subject to TDS, reducing the addition. This adjustment was made without allowing the AO to review the new evidence, violating Rule 46A of the Income Tax Rules, a decision later upheld by the Tribunal.

Issue of the Case

Was the ITAT justified in upholding an order based on new evidence accepted without allowing the Assessing Officer to review it or documenting reasons for the delay as per Rule 46A?

Decision of the Court

The High Court granted the appeal, overturning prior decisions due to the lower authorities' failure to follow legal protocols.

The court ruled that Rule 46A is mandatory; an appeals officer cannot accept new evidence without written justification and must allow the original tax officer to verify or contest it, violating the right to be heard.

About Author

Saloni Kumari

Content Writer

Saloni is a Content Writer with 2+ years of experience at studycafe.in. She writes legal, taxation, and finance related content including GST, Income Tax etc. Skilled in translating complex judicial pronouncements and regulatory developments into clear, and reader-friendly articles. Experienced in covering judgements of ITAT, High Court, GSTAT, and news related to Income Tax, GST, and corporate law. She can be reached at [email protected].

Saloni is a Content Writer with 2+ years of experience at studycafe.in. She writes legal, taxation, and finance related content including GST, Income Tax etc. Skilled in translating complex judicial pronouncements and regulatory developments into clear, and reader-friendly articles. Experienced in covering judgements of ITAT, High Court, GSTAT, and news related to Income Tax, GST, and corporate law. She can be reached at [email protected].

StudyCafe

StudyCafe Delhi, Delhi, India

Delhi, Delhi, India 2484

2484My Recent Articles

- ITAT Says Identity and Creditworthiness Irrelevant Where Loan Was Directly Paid to Haryana Mining DepartmentPremium

- Earlier Rejection Cannot Be Sole Ground to Reject Fresh Section 12AB and 80G Registration Applications, Says ITATPremium

- Cash Deposited During Demonetisation Cannot Be Taxed Under Section 69A if Linked to Business, Holds ITAT Premium

- ITAT Condones 1,731-Day Delay, Remands Cancer Trust's Section 12A Registration Application for Fresh ConsiderationPremium

- ITAT Lowers Estimated Profit Rate from 8% to 4% After Considering State Shutdown and Medicine Trade MarginsPremium

Up Next

Loading suggestions…

Recent Posts

All Posts

Recent Posts

All Posts