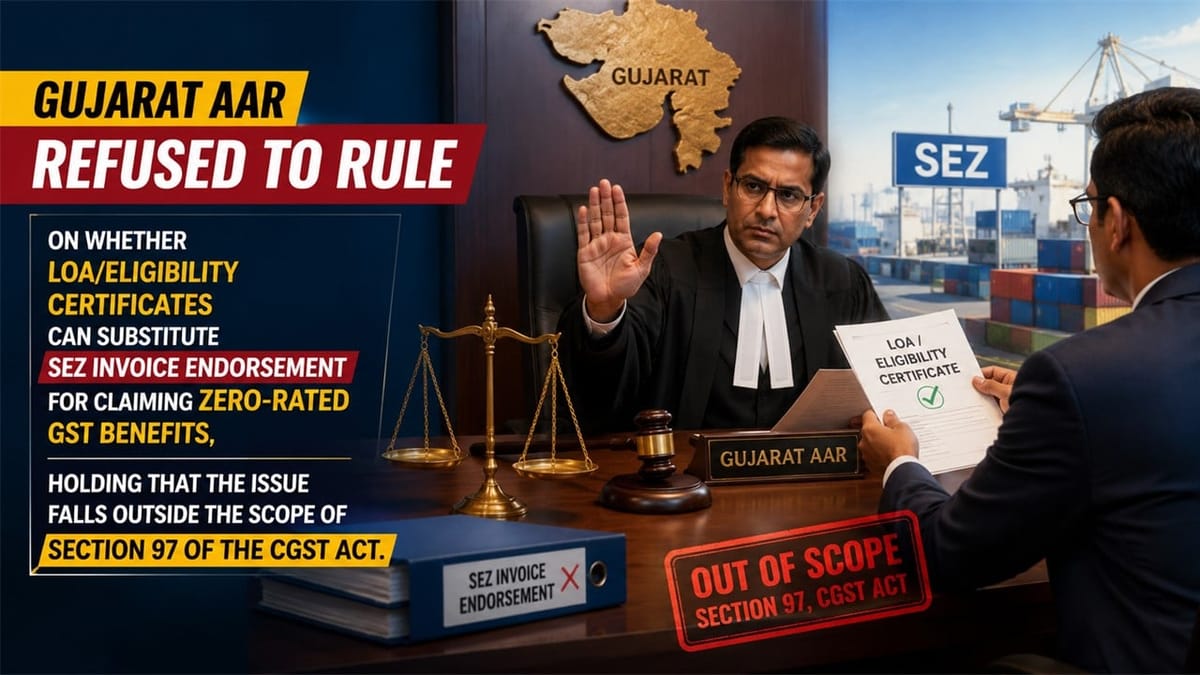

Gujarat AAR refused to rule on whether LOA/eligibility certificates can substitute SEZ invoice endorsement for claiming zero-rated GST benefits, holding that the issue falls outside the scope of Section 97 of the CGST Act.

Saloni Kumari | May 14, 2026 |

Gujarat AAR Declines Ruling on SEZ Invoice Endorsement Requirement for Zero-Rated Supplies

The company, Waystar Properties LLP (applicant), a limited liability partnership firm, has filed an application dated November 05, 2025, seeking the Gujarat Authority for Advance Ruling (AAR). The case was heard on April 08, 2026. The applicant holds GSTIN 24AADFW9786G1ZM, and its business location is situated at 15C2, Block 15, Gift City, Gandhinagar, Gujarat 382235.

The applicant claimed that it has been granted the status of a co-developer in Gujarat International Finance Tec-City Special Economic Zone (GIFT SEZ) under the Special Economic Zones Act, 2005, by the Board of Approval, Ministry of Commerce and Industry, Government of India. Consequently, it is empowered to develop, operate, and maintain certain specific infrastructure within the notified processing area of GIFT SEZ. The applicant, being a co-developer, is involved in renting out certain specified commercial properties called ‘demised premises’, whose sole situation falls within the processing area of GIFT SEZ. These properties are rented out to the lessee for running authorised operations as permitted under the SEZ framework.

Questions Asked by Applicant:

The applicant had asked the following questions before the Gujarat Authority for Advance Ruling (AAR):

“Question 1: Documentary Requirements and Legal Interpretation of ‘For Authorised Operations'”

Whether for availing zero-rated supply treatment u/s 16 of the IGST Act, 2017, read with Notification No. 09/2017-Integrated Tax (Rate) dated 28.06.2017, as amended w.e.f. 01.10.2023, for services supplied from the Domestic Tariff Area (DTA) to Special Economic Zone (SEZ) units/developers, the phrase “for authorised operations” can be established through documentary evidence, including a Letter of Approval (LOA)/Eligibility Certificate issued by SEZ authorities demonstrating that the service relates to authorised operations; or whether endorsement from the Specified Officer of SEZ on each invoice is mandatorily required irrespective of other documentary evidence available (Letter of Approval (LOA)/Eligibility Certificate) to prove that the service is supplied for “authorised operations”?

Question 2: Intra-SEZ Supplies – Zero-Rating and Endorsement Requirements.

Whether the supply of services from one SEZ unit to another SEZ unit (both located within SEZ and not in DTA) qualifies as a zero-rated supply u/s 16 of the IGST Act, 2017, and if yes, whether endorsement from the Specified Officer of SEZ is mandatory on each invoice for such intra-SEZ transactions, or whether the Letter of Approval (LOA) / Eligibility Certificate establishing that both parties are SEZ units engaged in authorised operations would be sufficient as documentary evidence?

Question 3: Practical Difficulty in Obtaining Endorsement for Intra-SEZ Supplies.

In situations where the service provider & service recipient are both SEZ developers/units and the SEZ authorities deny providing endorsement for such invoices, mention that “a procedure for endorsement is for services supplied from DTA to SEZ and details of such invoice to be mentioned through DTA Service Procurement Form (DSPF)” and that is not applicable for invoices for intra-SEZ transactions. Whether a Letter of Approval (LOA)/Eligibility Certificate as documentary evidence would be acceptable to establish that such services are supplied for authorised operations and such intra-SEZ supplies would still qualify for zero-rated treatment under GST law in the absence of invoice endorsement?”

Ruling Given by Gujarat AAR:

The Gujarat AAR has given the following ruling on the questions asked by the applicant:

According to the findings of the Gujarat AAR, the applicant company had sought clarification regarding whether invoice endorsement from the SEZ specified officer is mandatory for claiming zero-rated GST benefits under Section 16 of the IGST Act, especially for supplies between SEZ entities.

The applicant argued that supplies made for “authorised operations” should qualify as zero-rated if supported by relevant documentary evidence like the Letter of Approval (LOA), eligibility certificates, agreements, declarations from SEZ units, etc. It was further flagged that SEZ authorities reportedly do not provide invoice endorsements for intra-SEZ transactions, stating that the endorsement procedure applies only to DTA-to-SEZ supplies.

However, the Gujarat Authority for Advance Ruling (AAR) refused to answer all three questions, holding that they all fall outside the scope of every sub-section of Section 97 of the CGST Act, 2017, i.e., from Sections 97(a) to 97(g) of the CGST Act governing advance rulings. Since the questions did not involve classification, tax liability, input tax credit, registration, or supply determination, the authority refrained from giving any ruling on the merits.

In case of any Doubt regarding Membership you can mail us at [email protected]

Join Studycafe's WhatsApp Group or Telegram Channel for Latest Updates on Government Job, Sarkari Naukri, Private Jobs, Income Tax, GST, Companies Act, Judgements and CA, CS, ICWA, and MUCH MORE!"