The Income Tax Appellate Tribunal (ITAT) Delhi grants relief to Bellsonica Auto Component India Pvt. Ltd. in a transfer pricing dispute relating to royalty and technical fee payments to its associated enterprise.

Saima | Jun 18, 2026 |

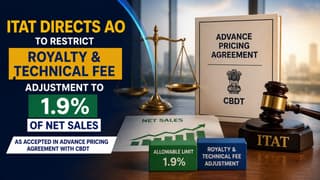

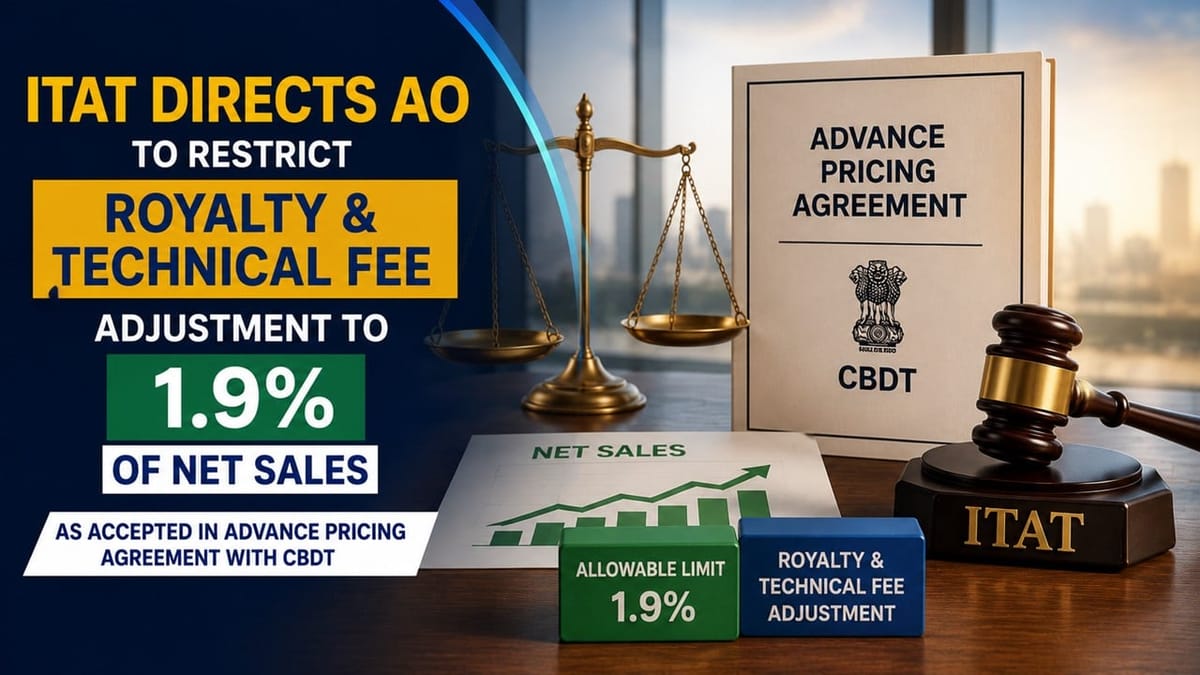

ITAT Directs AO to Restrict Royalty and Technical Fee Adjustment to 1.9% of Net Sales as Accepted in Advance Pricing Agreement with CBDT

The Income Tax Appellate Tribunal (ITAT) Delhi held that agreements entered into by the CBDT after examining all relevant aspects deserve the highest sanctity and directed the Assessing Officer to cap the royalty and technical service fee at 1.9% of net sales.

Bellsonica Auto Component India Private Limited had filed its return of income for assessment year 2014-15 declaring a loss of Rs 1.68 crore and during scrutiny proceedings, a reference was made to the Transfer Pricing Officer (TPO) under Section 92CA(1) of the Income Tax Act, 1961, for determination of the arm’s length price of international transactions entered into with associated enterprises.

Through an order passed under Section 92CA(3), the TPO proposed an adjustment of Rs 8.47 crore in respect of royalty and technical fee payments as made by the assessee to its associated enterprise. So, the AO passed the assessment order under Sections 143(3) read with 144C to make the corresponding addition. The CIT(A) upheld the adjustment, aggrieved by which the assessee filed an appeal before the Tribunal.

Before the Tribunal, the assessee contended that the TPO had incorrectly treated the arm’s-length value of royalty and technical fee payments as nil and had also wrongly included reimbursement expenses in the adjustment. The assessee submitted that it had entered into a Unilateral Advance Pricing Agreement (UAPA) with the Central Board of Direct Taxes on 29 November 2022, and a rate of 1.9% of net sales had been accepted for royalty and technical service fee payments.

The Revenue argued that the assessee had not proved with any documentary evidence that the services for which payment was made had actually been received. The Tribunal referred to the decision of Ranbaxy Laboratories Ltd. and ruled that the principles and methodology embodied in a concluded APA possess considerable persuasive value and should guide the determination of arm’s length price. Accordingly, it found the transfer pricing adjustment made by the lower authorities to be excessive.

Accordingly, the ITAT set aside the addition and directed the AO to cap the royalty and technical service fee at 1.9% of net sales, in line with the rate accepted by the CBDT under the APA and partly allowed the appeal of the assessee.

In case of any Doubt regarding Membership you can mail us at [email protected]

Join Studycafe's WhatsApp Group or Telegram Channel for Latest Updates on Government Job, Sarkari Naukri, Private Jobs, Income Tax, GST, Companies Act, Judgements and CA, CS, ICWA, and MUCH MORE!"