Karnataka AAR Allows ITC on Statutory Canteen Services for Employees And Denies Credit for Contract Workers:

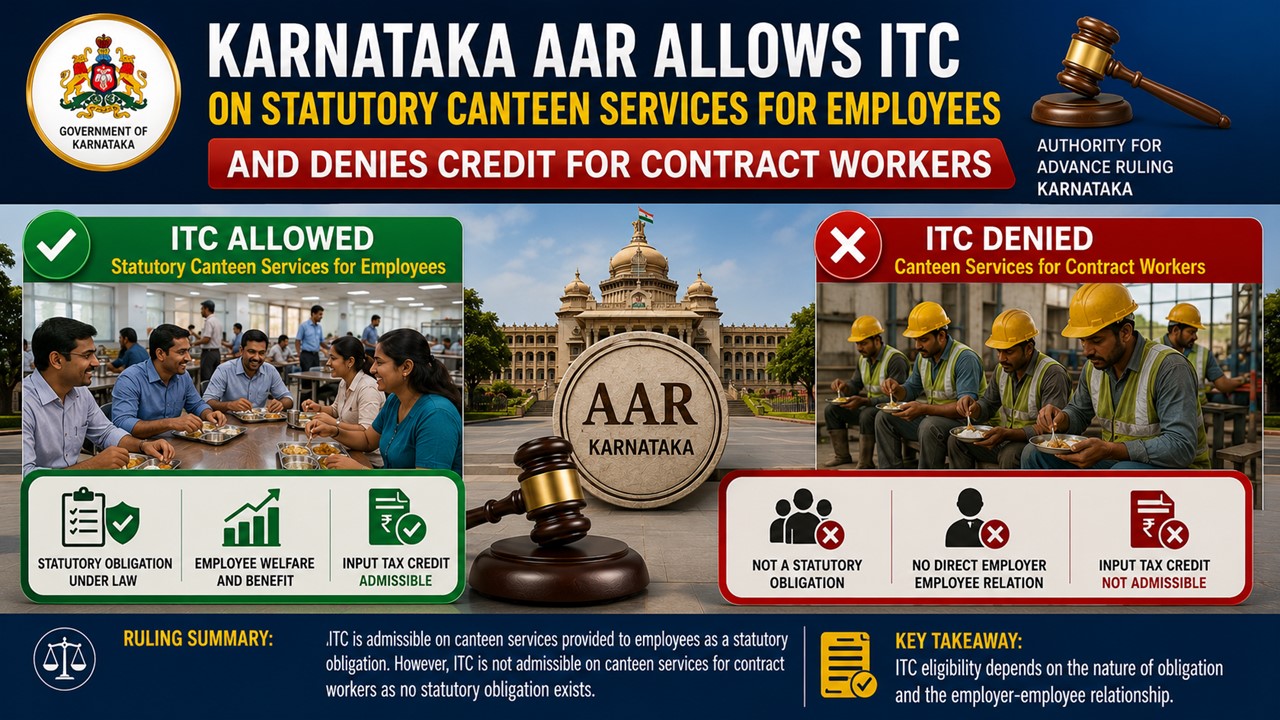

The Karnataka Authority for Advance Ruling (AAR) has held that M/s Aditya Auto Products & Engineering India Pvt. Ltd. is entitled to avail Input Tax Credit (ITC) on GST paid on canteen services provided to its regular employees.

AAR Holds That Recovery from Employees Not Eligible for ITC

Karnataka AAR Allows ITC on Statutory Canteen Services for Employees And Denies Credit for Contract Workers

M/s Aditya Auto Products & Engineering India Pvt. Ltd, engaged in the manufacture and supply of automobile parts under HSN 8708, filed an application under Section 97 of the Central Goods and Services Tax Act, 2017, seeking an advance ruling on whether Input Tax Credit (ITC) is available on GST charged by canteen service providers for supplying food facilities, which the company is statutorily required to maintain under Section 46 of the Factories Act, 1948.

The applicant operates three manufacturing units in Karnataka, which provide canteen facilities to regular employees as well as contract workers through third-party Canteen Service Providers (CSPs). The applicant asked that

"Is Input Tax Credit (ITC) admissible to the applicant on GST charged by the CSP for providing catering services, which the applicant is mandatorily required to provide under Section 46 of the Factories Act, 1948?"

The Authority observed that Section 17(5)(b) of the CGST Act blocks ITC on food and catering services. However, the proviso to the said provision permits credit where such facilities are obligatory for an employer to provide under any law. Referring to Section 46 of the Factories Act, 1948, the AAR noted that the applicant has a statutory obligation to provide and maintain canteen facilities for its employees under this act. So, GST paid on catering services supplied to regular employees qualified for ITC in terms of the proviso to Section 17(5)(b) of the CGST Act read with Serial No. 7 of Notification No. 11/2017-Central Tax (Rate) dated 28.06.2017 and Circular No. 172/04/2022-GST dated 06.07.2022.

The Authority further held that there was no statutory requirement compelling the applicant to provide canteen facilities to such workers; the restriction contained in Section 17(5)(b) continued to apply, thereby rendering ITC attributable to contract workers inadmissible.

On the issue of quantum of credit, the AAR held that the applicant could avail ITC only to the extent of the expenditure actually maintained by it. Since a part of the canteen cost was recovered from employees, credit could not be claimed on the entire value charged by the canteen service provider. Accordingly, the Karnataka AAR ruled that ITC on GST paid for canteen services is admissible in respect of regular employees under the proviso to Section 17(5)(b) of the CGST Act, 2017, but only to the extent of the cost borne by the employer. ITC relating to canteen services attributable to contract workers and the amount recovered from employees was held to be inadmissible.

For full information, refer to the whole document given below.

About Author

Saima

Content Writer

Saima is a Law graduate with a passion for research and content writing. She writes for Finance, Taxation and Legal Updates at Studycafe.in, simplifying complex legal decisions by the ITAT, High Court, AAR and GSTAT into uncomplicated and clear explanations.

Saima is a Law graduate with a passion for research and content writing. She writes for Finance, Taxation and Legal Updates at Studycafe.in, simplifying complex legal decisions by the ITAT, High Court, AAR and GSTAT into uncomplicated and clear explanations.

StudyCafe

StudyCafe Delhi, Delhi, India

Delhi, Delhi, India 275

275My Recent Articles

- ITAT Quashes Penalty as AO Failed to Validly Initiate Proceedings During AssessmentPremium

- ITAT Holds Mere Suspicion Over Surge in Jewellery Sales During Demonetisation Cannot Justify Addition Premium

- ITAT Rules Mere Omission to Report Exempt Dividend Cannot Convert Tax-Exempt Income into Taxable IncomePremium

- ITAT Allows Section 10(38) LTCG Exemption on Greencrest SharesPremium

- ITAT Condones 185 Day Delay And Grants Fresh Opportunity to Defunct PSU Premium

Up Next

Loading suggestions…

Recent Posts

All Posts

Recent Posts

All Posts