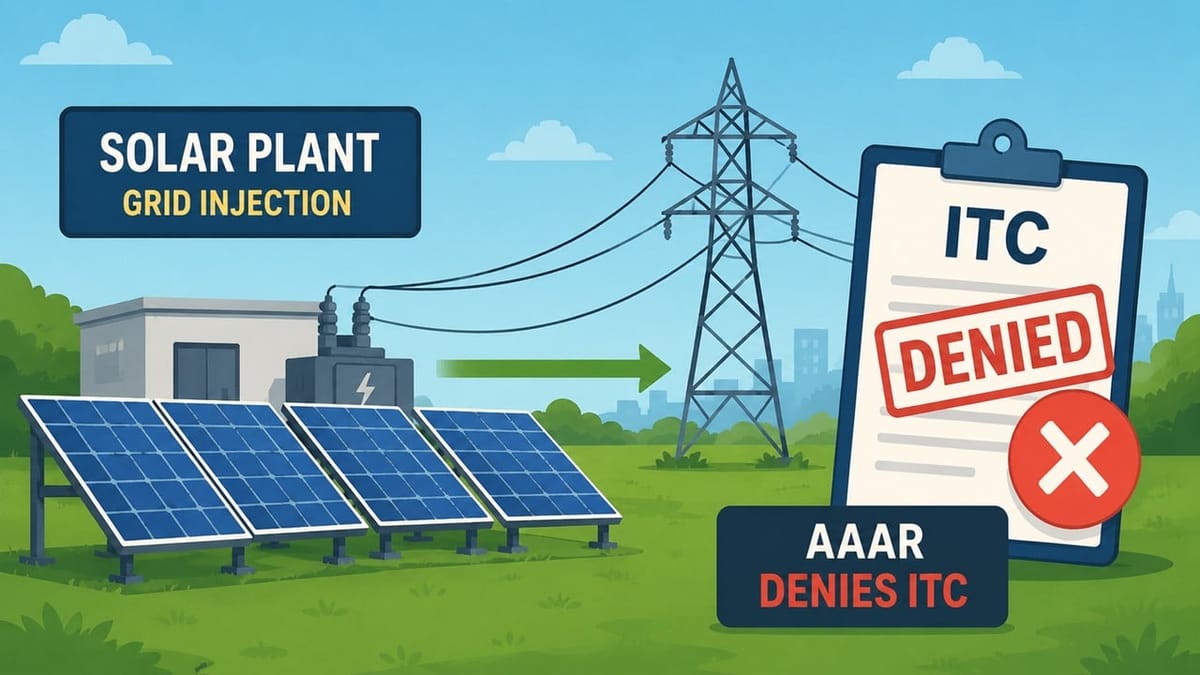

AAAR holds electricity injected into grid constitutes exempt supply, restricting related GST credits.

Meetu Kumari | Jun 19, 2026 |

Steel Manufacturer Set Up 20.5 MW Solar Plant for Captive Use; AAAR Denies GST ITC on Inputs and Capital Goods Used in Solar Project

The Appellate Authority for Advance Ruling (AAAR), Rajasthan, has upheld the denial of Input Tax Credit (ITC) to M/s SBF Ispat Pvt. Ltd. on goods and services used for setting up a 20.5 MW solar power plant intended to offset electricity consumption at its steel manufacturing unit.

The company manufactures TMT bars and MS billets and proposed to generate electricity through a solar power plant located at a separate site in Rajasthan. The power generated was to be injected into the RVPN/DISCOM grid, with equivalent energy credits being adjusted against electricity consumed at the factory. The company argued that the entire electricity generated would be used exclusively for manufacturing taxable steel products and therefore ITC on solar plant inputs, capital goods and services should be available.

Rejecting the contention, the AAAR held that once electricity is injected into the DISCOM grid, it amounts to a “supply” under the GST law. The adjustment of energy credits against future consumption constitutes consideration, making the transaction an outward supply of electricity. Since electrical energy is exempt from GST under Notification No. 2/2017-Central Tax (Rate), the inward supplies used for setting up and operating the solar power plant are attributable to an exempt supply.

The Authority further observed that electricity supplied to the grid cannot be regarded as captive consumption merely because the same entity later consumes electricity at another location under the same GST registration. According to the AAAR, the supply is made to the DISCOM, a separate entity, and therefore the subsequent drawal of electricity from the grid cannot be treated as self-consumption.

The appellant relied on several judicial precedents and advance rulings that had allowed credit on captive power projects. However, the AAAR distinguished those decisions on facts and held that they did not govern the present arrangement involving transfer of electricity to the grid and receipt of energy credits in return.

Thus, the AAAR upheld the Rajasthan AAR ruling and held that ITC is not available on inputs, capital goods or input services used for the design, engineering, erection, installation, commissioning and operation of the solar power plant, as the project is engaged in generating exempt electrical energy supplied to the grid.

To Read Full Order, Download PDF Given Below.

In case of any Doubt regarding Membership you can mail us at [email protected]

Join Studycafe's WhatsApp Group or Telegram Channel for Latest Updates on Government Job, Sarkari Naukri, Private Jobs, Income Tax, GST, Companies Act, Judgements and CA, CS, ICWA, and MUCH MORE!"