High Court quashes GST demand holding multiple financial years cannot be clubbed together.

Meetu Kumari | Jun 19, 2026 |

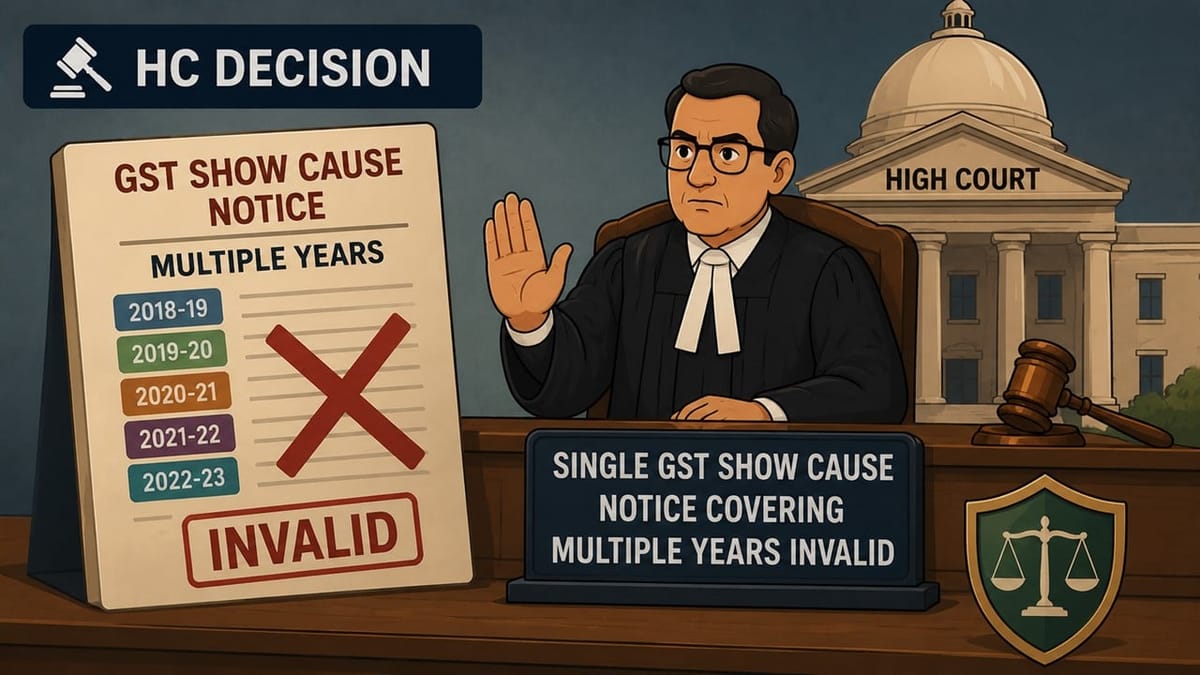

Single GST Show Cause Notice Covering 4 Financial Years and Rs.2.54 Crore Demand Invalid; Bombay High Court Quashes Entire Proceedings

The Aurangabad Bench of the Bombay High Court has quashed a GST demand of Rs.2.54 crore raised against M/s Rithwik Projects Private Limited, holding that the department lacked jurisdiction to issue a consolidated show cause notice covering multiple financial years under Section 74 of the CGST Act. The Court also set aside the consequential recovery proceedings initiated against the company’s bank account while granting liberty to the department to issue fresh notices in accordance with law.

The dispute arose from a show cause notice issued on 29 June 2022 proposing GST demand of Rs.2.54 crore, along with interest and penalty, for the period from 1 July 2017 to 31 August 2021. The petitioner, engaged in construction and infrastructure development activities, had paid royalty and other charges to the Government for allocation, permission and leasing of natural resources. Following adjudication, the Additional Commissioner confirmed the entire tax demand, imposed an equivalent penalty under Section 122(2)(b) of the CGST and MGST Acts, and initiated recovery proceedings through a third-party notice issued to Punjab National Bank.

Before the High Court, the petitioner contended that the impugned proceedings were without jurisdiction as the department had clubbed multiple tax periods and financial years in a single show cause notice. Reliance was placed on the Court’s earlier decision in Milroc Good Earth Developers v. Union of India, which had held that separate tax periods cannot be consolidated into one demand notice under the GST framework.

The Revenue opposed the petition on the ground that an alternate statutory remedy was available and further argued that the petitioner had acknowledged its liability during adjudication proceedings by seeking permission to pay the dues in instalments.

Examining the statutory scheme, the Court noted that the issue was squarely covered by the decision in Milroc, which had been consistently followed by various benches of the Bombay High Court.

“There is no scope for consolidating various financial years/tax periods. The action of issuing consolidated show cause notices for multiple assessment years is without jurisdiction.”

The Bench observed that GST assessments are linked to specific tax periods and financial years, and the statute contemplates separate proceedings for each relevant period. Consequently, a consolidated notice covering multiple years travels beyond the jurisdiction conferred by law.

The Court further rejected the Revenue’s contention that the petitioner’s request for instalment payments prevented it from challenging the proceedings.

“Since the show cause notice and the impugned order are without jurisdiction, the same are void ab initio and cannot be acted upon, irrespective of admission of liability on the part of the petitioner.”

Relying on settled principles governing jurisdictional defects, the Court held that orders passed without authority are nullities in the eyes of law and cannot be sustained merely because the assessee had participated in the proceedings or sought payment relief.

Holding that the impugned proceedings suffered from a fundamental lack of jurisdiction, the High Court quashed the show cause notice dated 29 June 2022, the adjudication order dated 21 December 2023, and the recovery notice issued to Punjab National Bank.

Thus, the writ petition was allowed, with liberty granted to the GST authorities to issue fresh notices separately for the respective financial years, if otherwise permissible under law.

To Read Full Judgment, Download PDF Given Below

In case of any Doubt regarding Membership you can mail us at [email protected]

Join Studycafe's WhatsApp Group or Telegram Channel for Latest Updates on Government Job, Sarkari Naukri, Private Jobs, Income Tax, GST, Companies Act, Judgements and CA, CS, ICWA, and MUCH MORE!"